Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

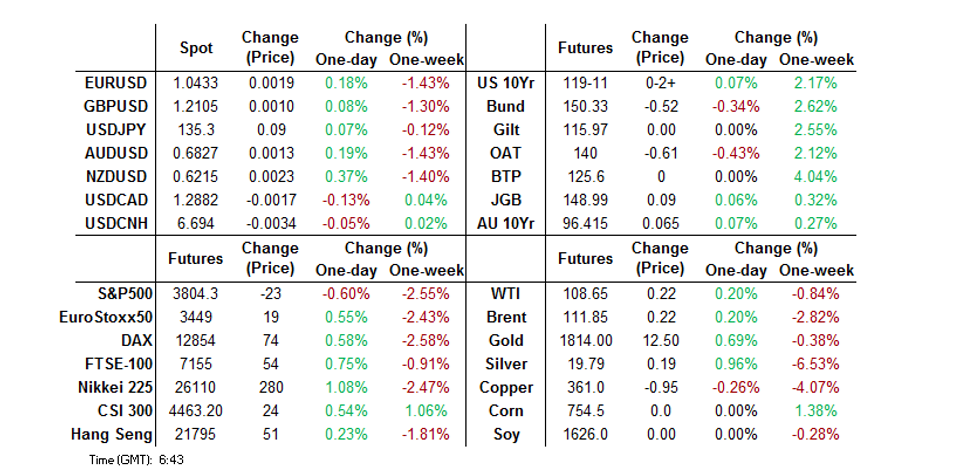

- Tsy futures moved away from best levels as Chinese equities reversed early losses during Asia hours, with cash Tsys closed owing to the Independence Day holiday.

- The broader USD has nudged lower (As measured by the DXY) in contained G10 FX trade.

- German trade data is on tap, as is Eurozone Sentix Investor Confidence & PPI. ECB members Nagel and de Guindos headlines Monday's central bank speaker slate.

US TSYS: Off Best Levels In Holiday-Thinned Trade

TYU2 prints +0-03 at 119-11+ into European hours, 0-01+ off the base of its 0-10+ overnight range, on limited volume of ~45K lots, while cash Tsys are closed for the Independence Day holiday. Early Asia trade was shaped by recessionary worry as Asia-Pac participants reacted to Friday’s softer than expected ISM m’fing reading. Note that the latest Russian advances in Ukraine and rising COVID cases in China’s Anhui province did little when it came to generating wider price action. That was before an uptick in Chinese equities (erasing early losses) allowed e-minis to find a bit of a base (S&P 500 e-minis last -0.5%), facilitating a pullback from best levels in Tsy futures. TYU2 respected Friday’s range after a pullback from Friday’s richest levels was observed ahead of the weekend.

- Note that the EDZ2/H3 & EDZ2/Z3 spreads operate a touch above their respective negative extremes last printing around -15bp and -75bp, respectively.

- There isn’t much in the way of notable economic data releases slated during the remainder of the day, meaning that various rounds of ECB speak will headline during a curtailed Tsy futures trading session.

JGBS: Swap Payside Flow Helps Futures Unwind Overnight Gains

JGB futures have followed the wider core global fixed income space away from overnight highs, with the contract up a mere 7 ticks as we work towards the Tokyo close (40 off the overnight session peak), with domestic equities moving higher and participants perhaps trimming short-term long positions after the rally from cycle cheaps.

- Cash JGBs sit 0.5bp richer to 1.0bp cheaper across the curve, with the curve steeoening as 30+-Year paper cheapens. Note that swaps lagged the early catch up rally observed in the cash JGB space, while the swap spread widening persisted as we moved through Tokyo trade as swap payside flows came to the fore, potentially aiding the cheapening/steepening themes.

- A quick reminder that our policy team have flagged their understanding that the Bank of Japan may be leaning towards taking its overnight rate out of negative territory rather than raising the upper limit of its yield control range in response to rising inflation and to ease speculative pressure as other major central banks tighten policy.

- There was little in the way of meaningful domestic headlines to impact the space, with continued news flow surrounding the Sakhalin 2 situation and impending upper house elections providing no real impetus for markets.

- Looking ahead, 10-Year JGB supply and wage data headline domestic matters tomorrow.

AUSSIE BONDS: Drifting Further From Best Levels

ACGB futures have backed away from overnight highs throughout the Sydney session (after retests for both YM & XM), with a pullback in U.S. Tsy futures (albeit on holiday-thinned trade) facilitating the move lower in the Aussie bond space. Cash ACGBs run 5.5bp to 7.5bp richer across the curve with the belly leading the bid. YM and XM are +7.0 and +7.5 apiece, while Bills run 2 to 11 ticks richer through the reds, bull flattening, but well shy of best levels observed since Friday’s settlement.

- Stronger than expected housing finance data and a firmer ANZ job ads print earlier in the session failed to elicit much reaction from the Aussie bond space, keeping in mind last week’s moves in ACGBs, with proximity to Tuesday’s RBA decision likely foremost in participants’ minds.

- Tuesday will see the S&P Global Services and Composite PMIs cross first, with the RBA’s decision due later in the day (with most looking for a 50bp rate hike).

RBA: MNI RBA Preview - July 2022: Everything Points To 50

EXECUTIVE SUMMARY

- The analytical community is unanimously behind the idea that the RBA will deliver further tightening at its July meeting, with 25 of the 26 surveyed by BBG looking for a 50bp hike and just one looking a 75bp step. The STIR space currently prices in ~43bp of tightening come the end of the Bank’s July meeting, which equates to just under a 75% chance of a 50bp hike.

- Domestic data flow & recent comments from Governor Lowe indicate that a 50bp hike will be implemented.

- Market pricing surrounding RBA tightening continues to look aggressive.

- Expect the Board to reiterate its guidance that it “expects to take further steps in the process of normalising monetary conditions in Australia over the months ahead.” Q2 CPI data (due 27 July) is set to provide the next major yardstick when it comes to assessing the velocity of any future RBA tightening,

- Click to view full preview.

FOREX: USD Off Smalls, A$ Underperforms

The USD is lower on the day, but moves have been well contained, in what has been a quiet start to the week. AUD underperformance has been evident, but is not dramatic.

- AUD weakness has reflected commodity falls, with focus on the sharp drop in iron ore today. Active Singapore futures are down 4.5% to sub $110/tonne. The metal has lost over 11% from recent highs. The dip in AUD/USD sub 0.6900 was short lived though.

- China headlines around another property default and rising covid case numbers from the weekend have not helped broader recessionary fears in terms of the global outlook. However, other China assets have shrugged off this, with equities rebounding from earlier weakness today, while USD/CNH is back to the low 6.6900 region.

- AUD/NZD is lower, back to a 1.0970/75. This comes despite better than expected Australian domestic data, although the weaker commodity picture outlined above is weighing. AU-NZ spreads have generally move in favor of the AUD today. NZD/USD is holding above just 0.6200 for now, versus an earlier high of 0.6217.

- Elsewhere, USD/JPY continues to be supported sub 135.00. We got just below 134.80, as US equity futures fell, but now sit back close to 135.150. US futures are off worse levels.

- EUR/USD is up smalls on the day, but within recent ranges, last at 1.0425. NOK has been an outperformer, up over 0.4% against the USD. USD/NOK sits with a 9.95 handle, but we did get close to 9.9000 in earlier trade.

- In terms of upcoming event risks, note US markets are closed for the US Independence Day holiday, so no US Cash Tsys trading. In the EU, German trade data is on tap, Switzerland CPI, and EU Sentix Investor Confidence are also due, along with the EU PPI. ECB members Nagel and Guidos also speak.

FX OPTIONS: Expiries for Jul04 NY cut 1000ET (Source DTCC)

- USD/JPY: Y135.00-05($769mln)

ASIA FX: Quiet Start To The Week

USD/Asia pairs have been mixed to start the week. USD/CNH is off earlier highs to the low 6.6900 region. KRW and TWD have been rangebound, despite weaker local equities. SGD NEER has lost some ground over the past week, while dips in USD/INR and USD/IDR were supported.

- CNH: USD/CNH pressed higher in early trade, but found selling interest above 6.7050. Weekend developments around another property sector default and rising onshore covid cases weighed, but China equities recovered from an early dip and are back in positive territory. China will also start a swap connect program with Hong Kong in 6 months. This is expected to increase the appeal of investing in CGBs, particularly from a hedging standpoint. USD/CNH is back at the low 6.6900 region, below the 50-day, which comes in at 6.7013.

- KRW: USD/KRW has been range bound. Equities have failed to gain any topside. The Kospi is off by another 1.10%. Spot USD/KRW has been stuck in a 1296-1300 range. Note important June CPI figures print tomorrow.

- INR: USD/INR spot opened sub 79.00, but this dip was supported. We are back to 79.04 now. Onshore equities are a little weaker. Sell-side analysts remain bearish on the rupee given the twin deficits and further run down in FX reserves.

- IDR: Spot USD/IDR opened below 14940 but quickly found support. The pair is back above 14960, close to highs from last Friday. Onshore equities were off by more than 3% at on stage, but we are now back to -2.5%. Portfolio outflows from both equities and bonds is weighing on the IDR, with little respite for the currency despite lower core G3 yields.

- PHP: USD/PHP spot spiked to 55.20 in early trade, but we are back closer to 55.03 now. Chief Economic Planner Arsenio Balisacan stated that growth of 7-8% would be hard to meet this year. A little above 6% was more likely. Note June CPI figures print tomorrow, with the market expecting a 6% YoY handle from 5.4% previously.

- SGD: The SGD NEER lost 0.25% last week, according to Goldman Sachs estimates. It has lost a little further ground today, with spot USD/SGD edging higher to 1.3975. Coming up later is the electronics sector PMI (last 50.5), and the broader PMI (50.4 expected versus 50.4 previously) both for June.

EQUITIES: Mixed In Asia; KOSPI Hits 20-Month Low

Asia-Pac equity indices are mixed at typing, bucking a positive lead from Wall St.

- The KOSPI has continued its tumble, dealing 1.0% weaker at typing after reversing opening gains, putting it on track for a fourth consecutive day of losses while hitting levels last witnessed in Nov ‘20 earlier in the session. Broader sentiment in the KOSPI continues to be weak amidst the backdrop of recent regulatory efforts to stabilise the stock market, with losses observed in 14 of the index’s 19 sub-industries.

- The Hang Seng Index trades 0.6% lower, dragged lower by underperformance in the financials (-2.0%) and property (-1.3%) sub-indices. Hong Kong Exchanges & Clearing Co (-3.8%) leads the way lower after announcing the launch of a “Swap Connect” between China and Hong Kong, with a BBG analysis suggesting that the initiative may not raise the HKEX’s clearing fees by much.

- The CSI300 deals 0.2% firmer at typing after reversing opening losses, aided by a sustained rally in the healthcare sub-index (+3.7%), as well as by richly valued consumer staples equities paring the bulk of their losses.

- The ASX200 deals 1.2% firmer at writing, with gains observed across virtually every sector. Tech-based large caps such as Block Inc and Xero Ltd lead the bid, adding to moderate gains observed in consumer staples and financials, with the “Big 4” banks sitting ~1.3% to 1.8% better off apiece at writing, making up for lacklustre performance in the materials sub-index.

- U.S. e-mini equity index futures sit 0.6% to 0.8% worse off apiece heading into European hours, a little off their respective session lows, operating comfortably around the upper half of Friday’s range at typing.

GOLD: Little Changed In Asia; Minor Reprieve On Recession Worry

Gold sits $2/oz worse off at typing to print $1,809/oz, a little below best levels highs after briefly showing above Friday’s high earlier in the session.

- To recap, gold recovered from five-month lows (at $1,784.6/oz) on Friday to close ~$4/oz firmer, breaking a four-day streak of losses. The recovery in gold on Friday was facilitated by a miss in the U.S. ISM m’fing survey and May construction spending, exacerbating heightened recession worry from some quarters, with the Atlanta Fed’s GDPNow tracker for Q2 ‘20 declining to -2.1% in the wake of the data print (from -1.0% prior).

- Elsewhere, BBG source reports over the weekend have pointed to the EU preparing bloc-wide sanctions on Russian gold imports, with Australia declaring their embargo on Russian gold on Sunday. The moves may ultimately change little, taking reference to previously-flagged reports of earlier western sanctions since Mar ‘22 already having restricted flows within the space.

- From a technical perspective, the move lower on Friday has seen gold briefly break support and the bear trigger at $1,787.0/oz (May 16 low), a clearer break of which could expose key support at $1,780.4 (Jan 28 low).

OIL: Little Changed In Asia; Recession Worry Lingers

WTI and Brent sit ~$0.10 weaker apiece at typing, paring earlier losses, and operating around the upper end of their respective ranges on Friday. Both benchmarks have risen from session lows as earlier worry re: a recession in the U.S. and an ongoing COVID outbreak in China’s east has moderated for now, mixing with lingering worry re: tight global crude supplies.

- Brent’s prompt spread (~$3.75 at typing) continues to sit at elevated levels despite recent downticks in crude benchmarks, pointing to expectations for near-term tightness in crude markets.

- Japanese PM Kishida offered details re: the G7’s proposed price caps on Russian crude - that they may be fixed at approx. half of its current purchase price. While consensus re: the wider impact of price caps has yet to be reached, some are increasingly pointing to the potential for a surge in oil prices due to issues surrounding the imposition of the measure.

- A previously-flagged worker strike in Norway’s O&G sector is estimated to reduce crude exports by ~130K bpd (~6.8% of national output), with little progress reported in ongoing wage talks.

- Elsewhere, Libyan crude production has declined, now averaging ~365K to ~409K bpd, down from >600K bpd in June, and less than half of the ‘21 average of ~1.1mn bpd. Several critical facilities (such as the 300K bpd El Sharara oilfield) remain under force majeure amidst political unrest.

- On the other hand, Ecuadorian crude output is expected to rise this week to ~90% of levels witnessed before recent political unrest, possibly representing ~200K bpd in recovered oil production.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 04/07/2022 | 0600/0800 | ** |  | DE | Trade Balance |

| 04/07/2022 | 0630/0830 | *** |  | CH | CPI |

| 04/07/2022 | 0700/0300 | * |  | TR | Turkey CPI |

| 04/07/2022 | 0900/1100 | ** |  | EU | PPI |

| 04/07/2022 | 1430/1030 | ** |  | CA | BOC Business Outlook Survey |

| 04/07/2022 | 1430/1630 | | EU | ECB Elderson on Climate Change at ECB Seminar | |

| 04/07/2022 | 1500/1700 | | EU | ECB de Guindos Speech at Frankfurt Euro Finance Summit |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.