Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Equity weakness and safe demand in the FX arena were evident overnight, with spill over from Monday trade and continued worry re: the COVID situation in China supporting that theme.

- The Japanese Finance Minister seemingly sounded a little more worried re: the recent run of JPY weakness.

- On the radar today we have German ZEW Survey and remarks from Fed's Barkin, ECB's Villeroy & BoE's Bailey.

US TSYS: Richer Overnight

Continued worry surrounding the COVID situation in China (another city went into a 3-day lockdown on the discovery of 1 case, while fears surrounding a Shanghai lockdown remained evident, with 3 COVID cases detected outside of quarantine) allowed Tsys to rally overnight, with weakness in e-minis and Chinese stocks noted.

- TYU2 showed through its Monday & Friday highs, although there was a lack of notable upside extension beyond that, with gains pared back into London hours. The contract last deals +0-05 at 118-17, 0-07 off of the peak of its 0-14+ range, operating on solid volume of ~115K. Cash Tsys run 1.5-3.5bp richer across the curve, with bull steepening in play.

- Asia-Pac flow was dominated by a couple of bloc buys in TY futures (+1.5K & +2.3K).

- Tuesday’s NY docket will provide the latest NFIB small business optimism reading, along with Fedspeak from Barkin (’24 voter) & 10-Year Tsy supply. A quick reminder that Wednesday will bring the CPI reading for June, with the Biden administration already warning of “highly elevated” readings, noting the prints will not reflect the recent lowering of gas prices

JGBS: Curve Twist Steepens, Futures Bid

JGB futures have held on to their morning bid, last printing +26, with the early uptick holding. Wider cash JGBs run 2.5bp richer to 1.5bp cheaper across the curve. 7s lead the rally in paper out to 20s, outperforming on the back of the bid in futures, while the curve has pivoted around 30s.

- A reminder that weakness in domestic equities and the wider defensive flows observed since Monday’s Tokyo close seemed to be the major supportive factors for the space throughout the session, although the super-long end softened as we moved through the day.

- The most notable round of domestic headline flow came from Finance Minister Suzuki, who seemingly showed greater outward worry re: the recent run of JPY weakness, at least when compared to previous communique on the matter. Suzuki is currently meeting with his U.S> counterpart, Yellen.

- A firm round of 5-Year supply would have helped the wider bid, as it saw the low price top wider dealer expectations (which stood at 99.81, per the BBG dealer pol), while the tail vanished as the cover ratio moved away from the multi-year low that was observed at the prior 5-Year auction, topping the 6-auction average (3.37x) in the process. The recent cheapening vs. swaps and allure of new paper likely facilitated demand.

- BoJ Rinban operations headline the domestic docket on Wednesday.

AUSSIE BONDS: Surveys Reiterate Consumer Woes & Tight Labour Market, ACGBs Bid

The defensive tone observed in wider markets (spill over from Monday trade & continued worry re: China COVID matters) coupled with soft domestic business and consumer survey prints (with the picture painted by consumers still far more dire than that given by businesses, at least in headline terms) has supported the ACGB space during Tuesday trade, leaving YM and XM 11.5 and 10.5 ticks above their respective settlement levels, a touch shy of best levels of the session. Cash ACGBs see the major benchmarks running 8.5-11.5bp richer across the curve, with 5s leading the bid. EFPs have actually broken the recent trend and sit a little narrower on the day, although the velocity and scale of the recent widening is notable. Bills run 5-19bp richer through the reds, bull flattening. Note that broader volume remains on the lighter side.

- Outside of the headline readings, we note that the NAB business survey revealed that “the supply side remains a challenge, with survey measures of both input and labour costs growth reaching new records in June at 3.6% and 4.8% respectively in quarterly terms.” This will have caught the RBA’s attention given its focus on softer survey and liaison programme findings when it comes to wage growth.

- A$800mn of ACGB Nov-32 supply headlines local matters tomorrow.

- In the semi space, SAFA’s May ’36 tap is set to price today after being launched earlier.

FOREX: Risk-Off Impulse Lingers On But Moderates, EUR/USD Flirts With Parity

Participants were reluctant to take more risk ahead of this week's company earnings reports & U.S. CPI data. Overnight headline flow did not provide much in the way of fresh insights, failing to assuage familiar fears related to China's COVID-19 situation and other well-documented headwinds to global growth. That said, initial risk-off impetus moderated as the session progressed.

- The yen still sits atop the G10 pile, with other traditional safe havens (USD, CHF) also showing strength. USD/JPY slipped into the Tokyo open and extended losses to Y137.03, before trimming initial losses.

- The dollar index (BBDXY) ripped through yesterday's best levels on its way to fresh cyclical highs, even as U.S. Tsys richened across the curve. All three main U.S. e-mini contracts sank.

- Spot USD/CNH added ~215 pips on a flight to safety, with the move likely facilitated by a slightly weaker than expected PBOC fix. The mid-point of permitted USD/CNY trading band was set 18 pips above expectations.

- Greenback strength drove EUR/USD to its lowest point since 2002, with the pair bottoming out at $1.0006. The rate sits within touching distance from parity, owing to the Eurozone's exposure to the fallout from Russia's war on Ukraine.

- The kiwi dollar showed resilience despite its commodity-tied peers coming under pressure. Reminder that the RBNZ will announce its rate decision on Wednesday, it is expected to hike the OCR by 50bp.

- On the radar today we have German ZEW Survey and remarks from Fed's Barkin, ECB's Villeroy & BoE's Bailey.

FOREX OPTIONS: Expiries for Jul12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0175-85(E521mln), $1.0260-70(E1.2bln)

- USD/JPY: Y135.55-60($1.0bln), Y137.60-65($1.2bln)

- NZD/USD: $0.6250(N$1.2bln)

- USD/CNY: Cny6.7000($1.3bln)

RBNZ: MNI RBNZ Preview - July 2022: Harsh Braking

EXECUTIVE SUMMARY

- New Zealand's GDP unexpectedly contracted in Q1 as COVID-19 swept across the nation for the first time, while a suite of leading indicators highlighted intensifying headwinds to the growth outlook.

- Still, data on inflation expectations and pricing intentions, as well as evidence that the labour market remains extremely tight, suggest that the RBNZ still has much work to do before fulfilling its mandate.

- There is broad consensus that the Reserve Bank will hike the OCR by another 50bp on Wednesday, continuing its fight against runaway inflation despite worrying ramifications for growth.

- There will be no updated forecasts or press conference, which gives the Committee time to keep implementing its well-defined "stitch in time" strategy for now, before revisiting its fundamental assumptions in August.

- Click here to see the full preview:MNI RBNZ Preview July 2022.pdf

BOK: MNI BoK Preview - July 2022: A 'Big Step' Rate Hike Of 50bps Expected

EXECUTIVE SUMMARY

- A 50bps hike by the BoK seems likely at this Wednesday’s policy meeting. This would take the policy rate to 2.25% from 1.75% currently, which would be the highest level since mid 2014. Such a call is not a uniform consensus among economists surveyed with Bloomberg, with 15 out of 19 expecting a 50bps hike. The remainder expect a more modest move of 25bps.

- This would be the BoK’s first such 50bps hike, although underlying inflation pressure justify such a move. The June data once again exceeded expectations. The headline printed at 6.0% YoY, while core prices accelerated to 4.4% YoY. The headline is the strongest rate of increase since 1998, while core is running at the firmest pace since early 2009.

- The weaker won trend also adds to the case for a larger rate hike, albeit at the margin. Higher USD/KRW levels are adding to imported price pressures from rising commodity prices.

- Click to view full preview: BoK Preview - July 2022.pdf

ASIA FX: Weighed By Lower EUR & Equity Weakness

USD/Asia pairs are higher today across the board, as lower EUR levels and weaker equity market sentiment continues to weigh. We are seeing fresh cyclical highs/record highs in a number of pairs.

- CNH: USD/CNH is above 6.7500, +1% above lows from late last week. Equity weakness, driven by fresh covid concerns, continues to outweigh better data momentum. The CNY fix was also weaker than expected. USD/CNH is playing catch up to broader USD strength, as EUR flirts with a break below parity against the USD.

- KRW: USD/KRW spot has reached fresh cyclical highs above 1315, around +0.85% above yesterday's closing levels. The Kospi is down by 1.4%, while offshore investors have stepped up the pace of selling of local equities.

- INR: Rupee continues to weaken, with USD/INR rising above 79.60, a further +0.25% on yesterday's closing level. The RBI's announcement of trade being settled in rupee hasn't had a huge impact on sentiment. The move is largely seen as facilitating Indian buying of Russian oil.

- IDR: Spot USD/IDR has added 21 figs so far and last deals at IDR14,994, a modest +0.15% rise on yesterday's levels. IDR is outperforming the broader trend for Asian FX. Indonesia's 5-Year CDS premium, one of the indicators of rupiah vulnerability watched by Bank Indonesia, has soared to levels last seen in June 2020.

- MYR: USD/MYR is at fresh cyclical highs, last trading at 4.4373. We have seen some catch up today with broader USD strength following yesterday's public holiday. FinMin Zafrul was positive about the nation's potential to meet its 2022 economic growth target. He suggested that GDP may rise +5.3%-6.3% Y/Y this year amid continued strengthening in domestic demand. g the recent upsurge in COVID-19 cases and urged high-risk individuals to get booster jabs.

- THB: Baht is revisiting cyclical lows. USD/THB is up 0.5% today, last at 36.36. Topside technical focus falls on Oct 2, 2015 high of THB36.665. Conversely, a dip through yesterday's low of THB35.882 would bring Jun 29 low of THB34.960 into play.

- PHP: The Philippines' monthly trade deficit unexpectedly widened to $5.679bn in May from $5.349bn recorded in April. The latest reading marks the largest shortfall on record, underscoring the gravity of the "twin deficit" challenge faced by the new administration from day one. Spot USD/PHP now trades +0.370 at PHP56.363, which brings the all-time high printed in 2004 at PHP56.500 into view.

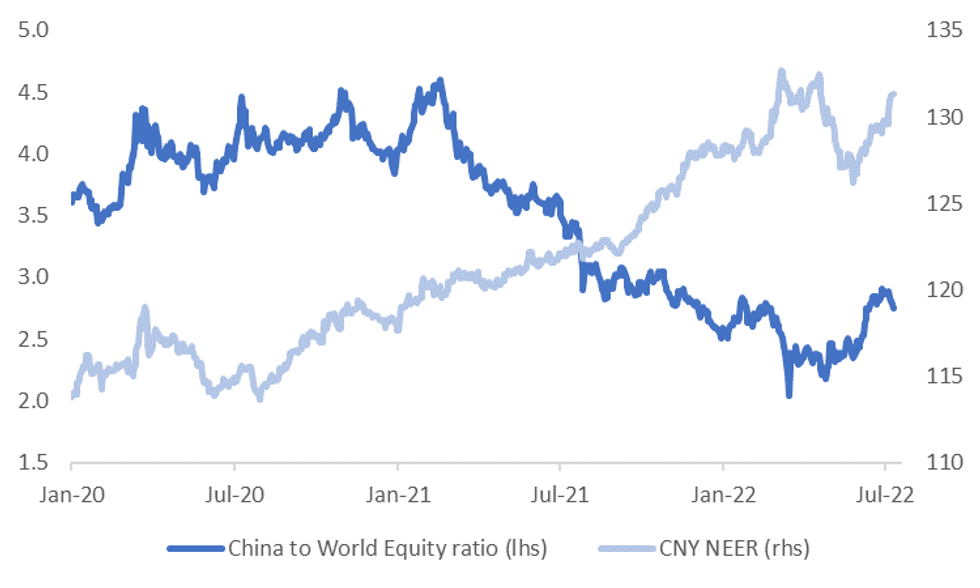

CNH: China Outperformance Theme Seeing Some Reversal

China equities are down again today (off -1.5 to -2%), continuing to unwind some of the recent outperformance trend, see the first chart below. Covid concerns are weighing with a fresh city put in lock down, while Shanghai has found a few more cases outside of quarantine. The market is looking through the overnight bumper credit figures, with the dynamic covid zero strategy continuing to raise questions over the growth rebound.

- CNH has still been outperforming, but it is starting to feel greater pressure from higher USD levels. Interestingly, the CNY TWI in NEER terms is not too far away from recent YTD highs, see the other line on the first chart below.

- USD/CNH has now risen above 6.7450, which is nearly 1% above the lows from the end of last week. We are back at highs from mid June. Just below the 6.7600 is the next level that could be eyed, and then above 6.7800 beyond that.

Fig 1: China Equities Unwinding Some Recent Outperformance, FX Next?

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

- Higher USD/CNH levels are spilling over to the rest of the USD/Asia FX complex. Spot USD/KRW is trading at fresh cyclical highs, above 1314, while USD/INR is closing in on 79.60, another record high. THB and PHP have also dropped further on the day.

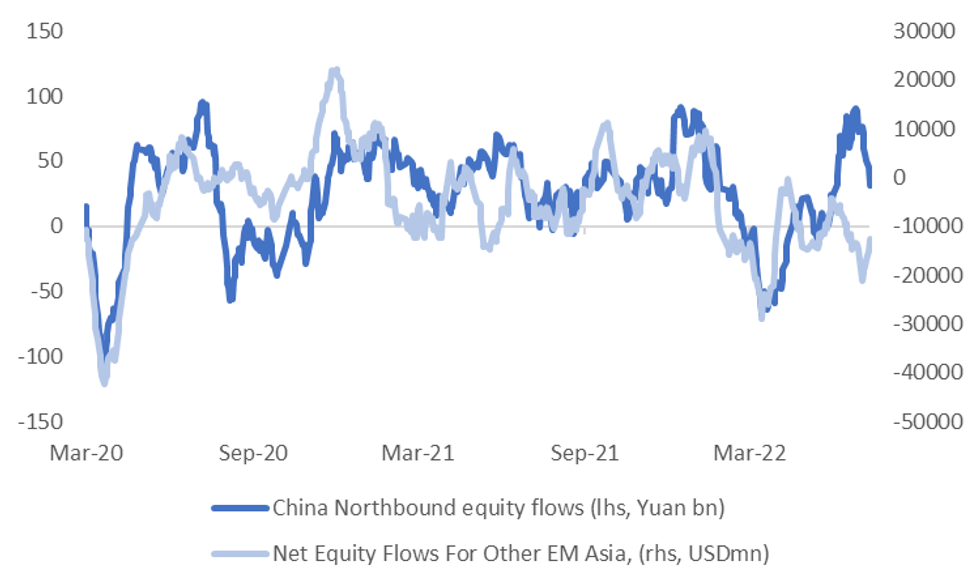

- Not surprisingly, inflows into China equities are also losing momentum, see the second chart below.

- Inflow momentum for the rest of EM Asia was on a slightly better trend, but this may not be sustained. If this eventuates, it creates another negative feedback loop for regional FX. Net outflows from South Korea today (-$171mn) are on track for the largest since the start of the month.

Fig 2: China Equity Flows & Rest Of EM Asia Equity Flows (Rolling Monthly Sum)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

EQUITIES: Generally Lower In Asia

Monday’s defensive tone spilled over into Asia-Pac hours, with the latest localised COVID-related lockdown in a Chinese city & the detection of a handful of cases outside of quarantine in Shanghai applying further pressure to wider sentiment.

- Headline flow was limited, with cross-market related moves front and centre. The weaker start for the likes of the Nikkei 225 and the KOSPI dragged e-minis through Monday’s lows, with the weakness in e-minis then extending further as Chinese equities moved lower.

- In terms of outright performance, the Nikkei 225 is 1.5% lower on the day at typing, with the CSI 300 printing 1.0% worse off. E-mini futures are 0.5 to 0.7% below settlement levels, with the NASDAQ 100 contract leading the weakness.

- The ASX 200 bucked the broader trend, sitting 0.3% higher on the day ahead of the close, benefitting from buoyant consumer staples and healthcare sectors, which outweighed the downtick in the heavyweight materials sector.

GOLD: Still Losing Ground

Gold saw a brief dip sub $1730 (low was a $1723 handle), but we are now back above this level, last tracking at $1732. This is down slightly from NY closing levels. The broader trend for the precious metal still looks skewed to the downside given ongoing USD strength.

- Gold's fortunes look tied to broader USD sentiment in the near term. The earlier dip came as EUR/USD almost fell through parity against the USD.

- Overnight moves in gold also tracked USD swings. The precious metals lost 0.5% yesterday and we are now at lows going back to late September last year. This low had a $1722 handle, which was close to levels we saw earlier today (~$1723). Beyond that is sub $1700 recorded in August last year.

- Lower back end US yields didn't help gold much overnight, although real 10yr yields are only marginally off recent highs, which is arguably a more important driver.

- Weaker equities also haven't generated much safe have support during today’s session.

OIL: Drifting Lower As Broader Risk Appetite Softens

Brent crude is down slightly from NY closing levels, last tracking sub $106/bbl, but has respected recent ranges since the start of this week. It's been a similar pattern for WTI, sitting close to $102.50/bbl currently. Cross asset signals have been negative, with equities lower and the USD gaining further ground.

- Broader energy commodity trends continue to outperform the metals complex, with supply pressures clearly holding up energy prices relative to metals.

- Today in Sydney, IEA Executive Director Fatih Birol stated that we may not have seen the worst of the energy crisis. He also stated this winter in the EU will be very difficult.

- The US is also trying to garner fresh support for its proposal to cap Russian oil export prices at $40-$60. This comes as US Treasury Secretary Yellen kicks off a 10 day trip to Asia, starting in Japan. Japan officials have already reportedly stated the cap could be too low, although haven’t rejected the proposal. US officials have stated failure to implement a cap could result in oil prices rising to $140/bbl. Clearly, there still needs to be lots of detail worked out with this plan.

- Elsewhere, US National Security Advisor Sullivan stated the US does believe OPEC has more oil capacity. This comes ahead of Biden's trip to Saudi Arabia this week.

- China Covid developments remain negative at the margin, onshore equities continue to weaken, while the city of Wugang was placed into a 3 day lockdown after 1 covid case was discovered. Close to 30 million people in China are currently in lockdown.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 12/07/2022 | 0800/0900 |  | UK | BOE Cunliffe on Crypto Markets | |

| 12/07/2022 | 0900/1100 | *** |  | DE | ZEW Current Conditions Index |

| 12/07/2022 | 0900/1100 | *** | | DE | ZEW Current Expectations Index |

| 12/07/2022 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 12/07/2022 | 0900/1000 | | UK | BOE Bailey Speaks at OMFIF | |

| 12/07/2022 | 1000/0600 | ** |  | US | NFIB Small Business Optimism Index |

| 12/07/2022 | - |  | EU | ECB de Guindos at ECOFIN Meeting | |

| 12/07/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 12/07/2022 | 1400/1000 | ** | | US | IBD/TIPP Optimism Index |

| 12/07/2022 | 1530/1130 | ** | | US | US Treasury Auction Result for 52 Week Bill |

| 12/07/2022 | 1600/1200 | *** | | US | USDA Crop Estimates - WASDE |

| 12/07/2022 | 1630/1230 | | US | Richmond Fed's Tom Barkin | |

| 12/07/2022 | 1700/1300 | ** | | US | US Note 10 Year Treasury Auction Result |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.