Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

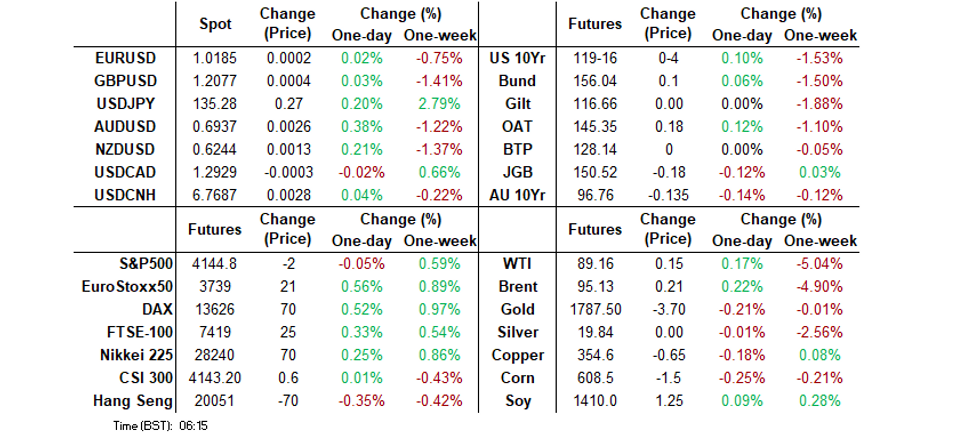

- JPY continued to struggled in post-NFP dealing, finding itself at the bottom of the G10 FX table during Tokyo dealing.

- U.S. Tsys unwound early Asia cheapening to sit marginally richer on the day into London hours.

- The global economic docket is particularly thin today, with U.S. NFIB small business optimism and unit labour cost data headlining.

US TSYS: Richer At The Margins In Asia

TYU2 operates just shy of best levels as we head towards London hours, last +0-03+ at 119-15+, -0-03 off the peak of its overnight high, dealing in a 0-10 range on limited volume of ~68K. Cash Tsys print little changed to 1bp richer across the curve.

- Post-NFP spill over and weekend Fedspeak applied pressure to the space in early Asia-Pac dealing, but bears failed to force a break below Friday’s lows in the major futures contracts (only TU experienced an actual test of its Friday trough). That was before geopolitics and a nudge lower in New Zealand inflation expectation provided some modest support for the space.

- In terms of details, the weekend saw Fed Governor Bowman indicate that similar sized rate hikes to the 75bp steps deployed recently should be on the table until inflation meaningfully decreases. Elsewhere, San Francisco Fed President Daly (’24 voter) reiterated her view that the Fed is “far from done yet” when it comes to its fight to bring down inflation, stressing the data dependence of the central bank (perhaps seeming a little more open to a larger than 50bp hike in the process).

- Elsewhere, the weekend saw Chinese trade data for July reveal a wider than expected surplus aided by much firmer than expected exports. Meanwhile, continued tension surrounding Taiwan also generated plenty of headlines, with China announcing its intentions to conduct “regular” drills near the island.

- Looking ahead, NY hours will see the release of the NFIB small business optimism index and unit labour cost data.

JGBS: Futures Lead Weakness In Belly, Steepening Gives Way To Twist Flattening

JGB futures pulled lower at the open, as Tokyo reacted to Friday’s post-NFP cheapening in U.S. Tsys, allowing the contract to take out its overnight session base. Since then, a recovery for U.S. Tsys from worst levels has facilitated a similar move in JGBs.

- That leaves the benchmark futures contract -17 at typing, a little shy of its Tokyo peak after failing to get anywhere near recouping the losses observed since Friday’s settlement. Meanwhile, the early bear steepening impulse witnessed on the JGB curve has given way to twist flattening, with the major benchmarks running 1.5bp cheaper to 0.5bp richer. 7s present the weakest point on the curve, owing to the aforementioned move lower in futures, while 30s are the firmest point on the curve, with the pivot seen at the 20-Year point.

- Lower tier local data and news flow hasn’t impacted the space, with wider cross-asset flows at the fore. Note that the Nikkei has flagged the likelihood of an announcement re: a government cabinet reshuffle on Wednesday.

- Flash machine tool orders data and 30-Year JGB supply headline the domestic docket on Tuesday.

AUSSIE BONDS: Off Of Extremes Into The Bell

Aussie bonds operate off of cheapest levels as we move towards the Sydney close, with U.S. Tsys trading in a similar manner. That leaves YM -14.5 & XM -13.5, with much of the overnight/early Sydney bear flattening in YM/XM unwound after YM failed to breach its overnight lows. Wider cash ACGB trade sees the major benchmarks print 10-14bp cheaper across the curve, with the belly leading the weakness.

- EFPs are a little narrower on the day, with the 3-/10-Year box flattening.

- Bills run 9-17bp cheaper through the reds.

- The space saw a modest, short-lived bid on the back of a moderation in NZ 2- & 5-Year inflation expectations from across the Tasman, before backing off from best levels alongside U.S. Tsys.

- The latest round of (infrequent) ACGB Apr-37 supply saw the weighted average yield print 0.51bp through prevailing mids (per Yieldbroker), while the cover ratio came in comfortably below the 2.50x benchmark. The auction was probably a bit softer than we expected on the whole, with the lack of clear micro relative value, flatness of the 5-/15- & 10-/15-Year yield curves and Monday timing of supply (the most illiquid time of the global trading week) the major negatives that we would point to.

- Moving forwards, the latest Westpac consumer and NAB business confidence surveys headline domestically on Tuesday. Elsewhere, the AOFM is set to come to market with A$100mn of index linked paper.

FOREX: Yen Stays On Back Foot, Kiwi Trims Gains As NZ Inflation Expectations Cool

Regional reaction to the most recent U.S. nonfarm payroll report released after Asia hours last Friday inspired some fresh demand for USD/JPY but the pair struggled to make much headway beyond the prior trading day's high. It topped out at Y135.58 and trimmed gains into the Tokyo fix as U.S. Tsy yields slipped into negative territory. The yen continues to underperform its G10 peers at the margin, mostly due to the absence of other notable catalysts.

- USD/JPY risk reversal crept higher, printing new multi-week highs across the curve, indicating stronger bullish sentiment among options traders.

- The BBDXY index retraced its initial uptick but managed to consolidate its post-NFP gains. The expectation-busting jobs report fanned hawkish Fed expectations.

- Antipodean currencies garnered some mild strength, albeit the kiwi dollar pared advance upon the release of the RBNZ's Q3 Survey of Expectations, which showed the first decline in 2-year out inflation expectations since mid-2020.

- The global economic docket is particularly thin today.

ASIA FX: Higher US Rates Weigh

Asian FX is weaker across the board today, albeit to varying degrees. Recent outperformers like THB and PHP have weakened as higher Fed expectations weigh. INR is also weaker, along with KRW. USD/CNH has edged up but is finding some selling interest above 6.7700.

- CNH: USD/CNH has edged higher through the session. We are seeing selling interest above 6.7700 but the pair hasn't corrected much to the downside. The CNY fix was in line with market expectations, while onshore equities are mixed. The weekend's record high trade surplus for July hasn't impact sentiment a great deal today, although is a strong buffer to capital outflow pressures from a medium term standpoint.

- KRW: USD/KRW 1 month has traded a tight range, with offers above 1305, but unable to get below 1302. Onshore equities are weaker but are away from worst levels. Spot USD/KRW is up around +0.50% from last week's close, around 1305 presently.

- TWD: USD/TWD is back above 30.00, in line with broader USD strength. Onshore equites are lower, but like Korea, are away from weakest levels. China also continued military drills near Taiwan, after early reports suggested drills had concluded. Note coming up later is July trade figures for Taiwan.

- INR: The rupee is weaker in early trade today, with USD/INR up +0.30% to 79.50. Eyes will be on whether we can test above 79.80, which reportedly drew strong intervention flows last week.

- IDR: Spot rupiah is weaker, with USD/IDR +34 figs to 14927, but the 1 month NDF is away from worst levels post the payrolls print on Friday. The pair is back to 14946. 5yr CDS is higher (last 116bps) but still well below mid-July highs of 165bps.

- THB: Spot USD/THB has been creeping higher today and last changes hands +0.22 at THB35.79 (around +0.60% for the session). This is line with higher US yields from late last week. 23 of the 26 economists surveyed by Bloomberg expect the Bank of Thailand to lift the key policy rate by 25bp this week, while the three dissenters have forecast a 50bp rate rise.

- PHP: Hawkish Fed repricing in response to the U.S. jobs report released Friday has lent support to USD/PHP as local markets re-opened. The peso is the worst performer in emerging Asia, with some linking its underperformance to a decline in the Philippines' stack of foreign reserves. USD/PHP was last at 55.59, nearly +0.70% for the session.

EQUITIES: Little Changed, With Conflicting Forces Observed

The major regional equity indices trade either side of unchanged in the first Asia-Pac session of the week, with deeper COVID restrictions in the Chinese province of Hainan, the post-NFP uptick in FOMC tightening premium, continued Chinese drills surrounding Taiwan and a shortening of Hong Kong’s quarantine period for international travellers at the fore on the headline front. The matters largely offset, although the net bearish skew to the major headline flow applied light pressure to the majority of the regional equity benchmarks. The Nikkei 225 was the outperformer amongst the major regional indices, last sitting 0.2% higher, benefitting from the post-NFP move lower in the yen. Elsewhere, the major regional indices run 0.2-0.8% below their respective Friday closes, while e-minis are 0.1% below Friday’s settlement levels.

GOLD: Can't Sustain Gains Above 50-Day MA

Gold is a little lower from Friday closing levels in NY. The precious metal last traded at $1773, off by a further 0.15%. After failing to close back above the 50-day MA on Friday (which comes in at $1787.40), the near term focus may shift to a more consolidative tone in gold.

- This is also in line with renewed Fed hawkishness last week and the bumper Friday payrolls report. With US real yields are on the march higher again, which is likely to present a near term headwind to gold. The real 10yr is back to +37bps, from a recent low of +9bps at the start of the month.

- The correlation between gold and US real yields remains a reasonable one. Note US nominal yields are down a touch today, with both the 2yr and 10yr down by 1.5 to 2bps. This hasn’t aided gold sentiment though.

- Other cross asset drivers haven’t had a huge influence on trends today either. Equities are mixed in Asia Pac markets, but generally away from worse levels. The same goes for US equity futures. The USD has tried to rally against the majors today, but hasn't made much in the way of fresh inroads.

- Elsewhere, the Czech central bank stated over the weekend it wants to increase the shares of its FX reserves that are held in gold. Note total FX reserves for the central bank are $157bn.

OIL: Modest Upside, Tentative Signs Of Improving China Demand

Oil prices have steadily recovered after early weakness at the open. Brent is back at $95/bbl, while WTI is a touch over $89/bbl. These are very small gains, but build on modest positive momentum from Friday's session.

- Yesterday's China import data showed some recovery in oil demand, around 4.2% higher compared to June levels in terms of import volumes. We are still down 4% on a year-to-date basis though.

- The demand outlook also improved at the margin as Hong Kong cut the hotel quarantine period from 7 days to 3 days for intervention travellers (effective this Friday). China also eased rules around international flights where covid cases are detected, although restrictions still remain in place.

- These benefits to demand could also be offset by a fresh lockdown in Sanya, a holiday destination, while Hainan will conduct mass testing as case numbers continue to climb.

- Spec positions continued to move lower, with net longs in Nymex now back to fresh lows from April 2020.

- Goldman Sachs cut its near term forecast for oil. The Bank lowered its Q3 forecast to $110/bbl from $140/bbl, and the Q4 forecast to $125/bbl, from $130/bbl. The 2023 outlook was unchanged at $125/bbl and the Bank maintained a constructive view over the medium term.

- The market focus will also be on a number of official reports this week. The US EIA prints its short-term outlook on Tuesday. Monthly snapshots are also out from OPEC and the International Energy Agency on Thursday.

- Note for Brent the 200 day MA comes in $98.60/bbl. Brent is down further 13.6% since the start of August, after a 4.2% drop in July.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 08/08/2022 | 0545/0745 | ** |  | CH | unemployment |

| 08/08/2022 | 1500/1100 | ** |  | US | NY Fed survey of consumer expectations |

| 08/08/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 08/08/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 09/08/2022 | 2301/0001 | * |  | UK | BRC-KPMG Shop Sales Monitor |

| 09/08/2022 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 09/08/2022 | 1000/0600 | ** | | US | NFIB Small Business Optimism Index |

| 09/08/2022 | 1230/0830 | ** | | US | Preliminary Non-Farm Productivity |

| 09/08/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 09/08/2022 | 1400/1000 | ** | | US | IBD/TIPP Optimism Index |

| 09/08/2022 | 1530/1130 | ** | | US | US Treasury Auction Result for 52 Week Bill |

| 09/08/2022 | 1700/1300 | *** | | US | US Note 03 Year Treasury Auction Result |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.