Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

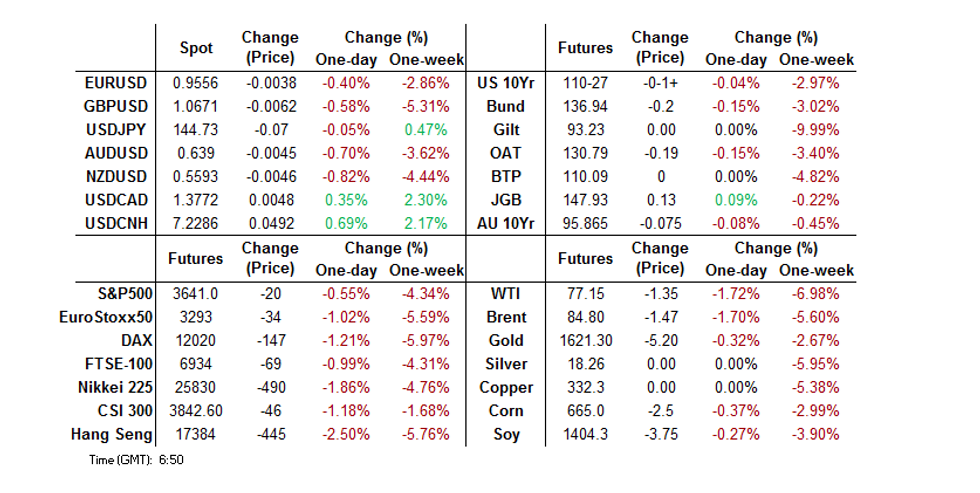

- Recent themes extending with 10-YEar U.S. Tsy yields probing 4.00% for the first time since '10, S&P 500 e-minis registering fresh cycle lows and another new all-time high for the BBDXY on the back of broader USD strength, punctuated by a fresh all-time peak in USD/CNH.

- On the data front, U.S. pending home sales & flash wholesale inventories take focus from here. The central bank calendar remains busy, a long list of speeches includes comments from ECB Pres Lagarde & Fed Chair Powell.

- Gilt market moves will continue to be eyed in light of yesterday’s IMF and ratings agency rhetoric re: UK fiscal matters.

US TSYS: 10s Probe 4%

Cash Tsys sit 1.0-3.5bp cheaper into London hours, with 7s leading the weakness. TYZ2 sits 0-06+ off the base of its 0-15+ range, with volume nearing 130K.

- 10-Year yields briefly showed above 4.00% for the first time since ’10 overnight, before pulling back as bears failed to force a sustained and meaningful move through the round number.

- We have flagged the 4.00% mark and double top zone drawn off the ‘09/’10 highs (just above the round number) as a key technical area in recent days.

- San Francisco Fed President Daly reiterated the central Fed message re: its resolute approach to taming inflation.

- Elsewhere, White House economic advisor Deese played down the idea of a Plaza-type accord in the FX markets, allowing the broad USD to firm. Meanwhile, Axios suggested that Tsy Secretary Yellen may depart the Biden admin after the mid-terms. These matters may have factored into the cheapening in Tsys.

- We saw a block seller of TY futures (-~3K) which helped the cheapening. There were also block sales of FVX2 106.50 puts (-2.5K) & FVX2 106.75 puts (-2.5K), with the former seemingly partial profit taking and the latter perhaps part of a spread against the remainder of the existing exposure.

- Gilt market moves will continue to be eyed (in light of yesterday’s IMF and ratings agency rhetoric re: UK fiscal matters), with second tier data, 7-Year Tsy supply and Fedspeak from Powell, Bowman, Bullard, Bostic, Evans & Barkin due in NY hours.

JGBS: The Steepening Extends

Curve steepening has extended through the Tokyo day, with 20+-Year JGB yields running 3.0-8.0bp higher, aided by the previously outlined show higher in U.S. Tsy yields and the BoJ’s choice to refrain from deploying another round of off-schedule Rinban purchases.

- Paper out to 10s is little changed, anchored by the BoJ’s YCC mechanism, which promotes a steeper curve in a bearish bond environment.

- JGB futures are a touch lower vs. levels seen at the end of the overnight session, last +4 vs. yesterday’s settlement, hugging a tight range. Participants are seemingly unwilling to test the BoJ’s resolve via a retest of June’s bearish extremes in the contract given the (ultimately successful) BoJ defences deployed at that time.

- 2-Year JGB supply and the weekly international security flow data headline tomorrow’s domestic docket.

AUSSIE BONDS: Steepening Theme Spills Into ACGBS

Wider moves in core global FI markets were at the fore when it came to ACGBs, leaving YM and XM off worst levels after a foray below their respective overnight troughs, -1.5 & -7.5, respectively. The wider ACGB curve has twist steepened, with benchmarks running 1.5bp richer to 8.5bp cheaper, pulling the 3-/10-Year curve further away from cycle flats.

- The 3-/10-Year EFP box has twist steepened, putting an end to the recent consistent flattening pressure.

- Bills sit +5 to -2 through the reds, also twist steepening. RBA dated OIS prices in 43bp of tightening for next week’s decision, little changed on the day, while terminal rate pricing is 5-10bp softer, sitting just below 4.30%.

- There was no tangible reaction to the slightly firmer than expected domestic retail sales data for August (+0.6% M/M vs. BBG Median +0.4%).

- Elsewhere, the final Australian underlying deficit for FY21/22 came in at -A$32.0bn, roughly in line with the positive adjustments flagged by the Treasurer in recent weeks, with fiscal headwinds touted once again.

- Job vacancies data headlines the domestic docket on Thursday.

NZGBS: Cheaper On Wider Impetus

A move higher in global FI yields applied pressure to NZGBS as we moved through Wednesday trade, leaving the major benchmarks running 3.0-5.5bp cheaper on the session, with some light bear steepening in play.

- 2- & 5-Year swap spreads pushed wider, while 10- & 15-Year swap spreads narrowed a touch.

- Another round of solid domestic filled jobs data was observed.

- RBNZ OIS pricing is little changed vs. what was seen at the start of the session i.e. 53bp of tightening priced for next week’s meeting, with a terminal rate of ~4.85% priced at present.

- The weekly round of NZGB issuance (’27, ’32 & ’41 paper is due to be auctioned) and the monthly ANZ business survey headline domestic matters on Thursday.

FOREX: Risk-Off Takes Hold, Comments From White House's Deese Support Greenback

Risk sentiment was suppressed by Tuesday's round of hawkish Fedspeak and a report noting that Apple is abandoning plans to boost iPhone production, which weighed on the equity space. White House National Economic Council chief Deese played down potential for a new Plaza-like accord, which lent further support to the greenback.

- Gauges of U.S. dollar strength were trending higher. The BBDXY index surged to a new record high of 1,359 and the DXY index topped out at a fresh cyclical high of 114.69. Firmer U.S. Tsy yields facilitated demand for the greenback.

- White House's Deese told attendees of an event hosted by the Economic Club of Washington, DC that a currency pact to counter USD strength was unlikely. His comments seemingly underpinned renewed USD strength, even as there wasn't much prior hope/discussion of such a deal.

- Bloomberg trader sources flagged that leveraged funds were dumping the sterling in response to Deese's remarks. Cable sold off sharply, shedding ~75 pips to erase the entirety of yesterday's gains.

- The yen was the only G10 currency to trade roughly on par with the greenback, benefitting from its safe-haven status and the perception of heightened intervention risk. The Swiss franc was also resilient amid demand for safety.

- The kiwi dollar led high-beta FX bloc lower, with NZD/USD hitting its worst levels since Mar 2020 and AUD/NZD touching its highest point in nine years. A spillover from offshore yuan weakening past CNH7.2 versus the dollar may have added pressure to the Antipodeans.

- On the data front, U.S. pending home sales & flash wholesale inventories take focus from here. The central bank calendar remains busy, a long list of speeches includes comments from ECB Pres Lagarde & Fed Chair Powell.

FX OPTIONS: Expiries for Sep28 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9850-60(E743mln)

- USD/JPY: Y141.80-00($769mln), Y145.00($514mln)

- NZD/USD: $0.5980(N$784mln)

- USD/CNY: Cny7.1000($1.1bln), Cny7.1500($700mln)

ASIA FX: USD/CNH Breaks Higher

Yesterday's pause in the USD uptrend has given way to fresh weakness today. Except for USD/PHP, all pairs are higher. Much of the focus rested with USD/CNH, which broke to fresh cyclical highs above 7.2000. Still to come is the BoT decision, where it is a close call between a 25bps or 50bps hike. Tomorrow the data calendar is light for the region.

- USD/CNH hit as high as 7.2386, post the 7.2000 break. USD/CNY is above 7.2200 as well, fresh highs back to early 2008. The fixing outcome wasn't as strong as recent sessions, while the introduction of the countercyclical factor didn't shift market estimates too much.

- USD/KRW is now close to 1440, with spot 1.2% weaker in the session. Onshore equities have slumped (-3%), with tech under pressure following reports Apple will ditch plans to ramp up iphone production due to softer demand. This afternoon BoK also announced it will conduct direct purchases of bonds to curb interest rate volatility.

- USD/INR is just shy of 81.90, another record high. India's inclusion in the J.P. Morgan EM debt index will be delayed until 2023. Coming up on Friday is the RBI decision, where a 50bps hike is expected.

- IDR is the second weakest performer within the region today, after the won. Spot USD/IDR is up close to 15250. Yesterday's intervention flows have been digested by the market.

- Spot USD/PHP sits at 58.986, within touching distance from record highs (59.001), but little changed for the session. BSP Gov Medalla sought to discourage buying dollars way before use as he warned that it would add pressure to the beleaguered peso. He stopped short of announcing any measures to that effect, noting that the central bank will not raise any barriers to dollar purchases for domestic companies.

- Spot USD/THB has climbed in line with regional trend, as the BBG/J.P. Morgan Asia Dollar Index prints 20-year lows. The rate changes hands +0.15 at 38.077. The Bank of Thailand will announce its monetary policy decision within a few hours (see our preview here). Most economists expect the Committee to raise the key policy rate by 25bp, but broadening price pressures and weak exchange rate support the case for a more aggressive move.

EQUITIES: Apple Demand Concerns Hits Regional Tech Sentiment

Asia Pac equities are down across the board, particularly in the tech related space. Only Indonesia's JCI has managed to hold gains today within the region. Sentiment was hurt early on a BBG headline, noting that that Apple has “ditched” an iPhone production increase on the back of faltering demand.

- This sent US futures lower across the 3 major contracts. At one stage Nasdaq futures were off by 1.3%. We are away from worst levels but still in the red. The next level of technical support for the S&P 500 contract comes in at the round number of 3,600.

- The spill over to tech plays in Asia has been evident. The Nikkei 225 is off around 2%, while HSI is down over 2.3%, dragged by a 2.76% fall in the etch sub index.

- The Kospi has fared slightly worse, down by close to 3%, the TWSE around 2.15%.

- Mainland China bourses are down, but have outperformed on a relative basis. The Shanghai Composite is off by 0.75%. A China Developer, CIFI Holdings, was down sharply though on fresh debt concerns. The company is the China's 13th largest building.

- Australian stocks are down by 0.7%, with energy related names helping drive outperformance.

OIL: Falters On Cross Asset Headwinds

Brent crude dipped as far as $84.50/bbl in early trade, but we have stabilized somewhat, now back above $85/bbl. We are still off by 1.3% for the session so far. WTI is around $77.50/bbl, down by the same amount since the open. Fresh risk aversion in the equity space, along with cyclical highs in USD FX indices, has weighed.

- We haven't unwound all of oils gains from Tuesday's session. Support came from reports that Russia will propose a 1mln barrel output cut at the next OPEC+ meeting according to Reuters. There was also spill over from higher EU gas prices, which came after leaks were reported at Nordstream pipelines.

- In the US, API reported a +4mln barrel increase in crude inventories, although gasoline stocks fell by just over 1mln. Note we get the EIA weekly report this evening. Around 11% of US Crude production (190k barrels) is off line as Hurricane Ian bares down on the Gulf of Mexico region.

- Finally, some China oil refiners sounded more optimistic on the Q4 outlook for the China economy at the final day of the Asia Pacific Petroleum Conference in Singapore (see this Bloomberg link for more details).

GOLD: Risk Aversion Providing Some Support

Gold is lower for the session, but only by a modest -0.20%. We currently sit around $1625.50, which is still above recent cyclical lows closer to $1621 (from earlier in the week). This comes despite fresh highs in USD FX indices, with the dollar's relentless rise underpinned by the White House pushing back on the need for any fresh Plaza-type FX accord agreement.

- Support for gold appears to have come from the risk aversion channel. Equity markets are off strongly in Asia Pac, particularly in the tech space, while US futures are down as well, albeit away from worst levels.

- Consistent with this theme, the precious metal is also outperforming other commodities so far today (copper, oil and iron ore).

- US yields are also higher, but the 10yr couldn't an earlier break through 4.00%. The real US 10yr yield climbed further overnight to 1.64%. This may cap any upswings in gold, with overnight highs above $1640 a potential resistance point.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 28/09/2022 | 0600/0800 | * |  | DE | GFK Consumer Climate |

| 28/09/2022 | 0600/0800 | ** |  | SE | Retail Sales |

| 28/09/2022 | 0600/1400 | ** |  | CN | MNI China Liquidity Suvey |

| 28/09/2022 | 0645/0845 | ** |  | FR | Consumer Sentiment |

| 28/09/2022 | 0700/0900 | ** | | SE | Economic Tendency Indicator |

| 28/09/2022 | 0715/0915 |  | EU | ECB Lagarde at Frankfurt Forum Discussion | |

| 28/09/2022 | 0800/1000 | ** |  | IT | ISTAT Business Confidence |

| 28/09/2022 | 0800/1000 | ** | | IT | ISTAT Consumer Confidence |

| 28/09/2022 | 0815/0915 |  | UK | BOE Cunliffe Keynote at AFME Conference | |

| 28/09/2022 | 0900/1100 | * | | IT | Industrial Orders |

| 28/09/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 28/09/2022 | 1230/0830 | ** | | US | Advance Trade, Advance Business Inventories |

| 28/09/2022 | 1235/0835 | | US | Atlanta Fed's Raphael Bostic | |

| 28/09/2022 | 1400/1000 | ** | | US | NAR pending home sales |

| 28/09/2022 | 1410/1010 | | US | St. Louis Fed's James Bullard | |

| 28/09/2022 | 1415/1015 | | US | Fed Chair Jerome Powell | |

| 28/09/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 28/09/2022 | 1500/1700 | | EU | ECB Elderson Intro at Greens/EFA Event | |

| 28/09/2022 | 1500/1100 | | US | Fed Governor Michelle Bowman | |

| 28/09/2022 | 1530/1130 | ** | | US | US Treasury Auction Result for 2 Year Floating Rate Note |

| 28/09/2022 | 1530/1130 | | US | Richmond Fed's Tom Barkin | |

| 28/09/2022 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 28/09/2022 | 1700/1300 | ** | | US | US Treasury Auction Result for 7 Year Note |

| 28/09/2022 | 1800/1400 | | US | Chicago Fed's Charles Evans | |

| 28/09/2022 | 1800/1900 | | UK | BOE Dhingra Chairs Panel at LSE |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.