Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

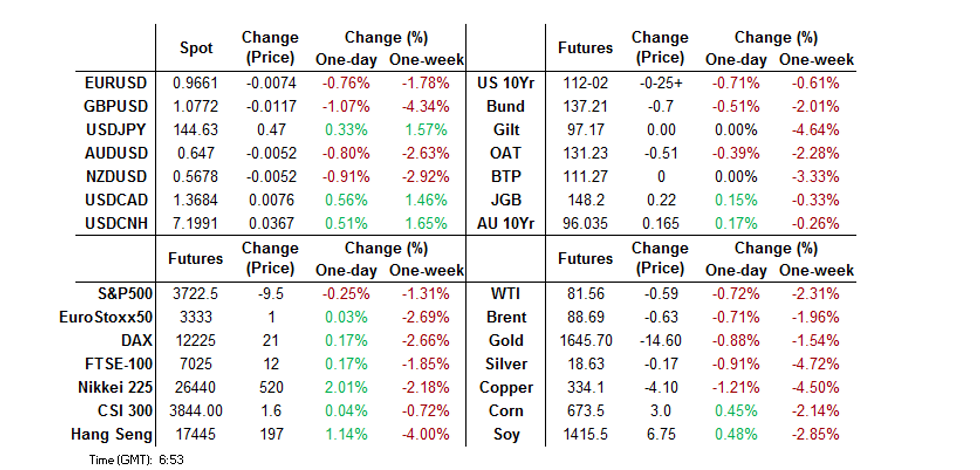

- USD strength was at the fore in G10 FX during Asia-Pac hours. Core FI markets are being pressured in recent trade on German NRW state CPI data, which topped wider expectations for the national reading.

- On the global data docket we have U.S. initial jobless claims and third reading of Q2 GDP, German consumer inflation figures and Canadian GDP. Another hefty round of central bank rhetoric is inbound, with Fed, ECB, BoE and Riksbank members due to speak.

US TSYS: Asia Fades Some Of Wednesday’s Rally

Cash Tsys run 1-4bp cheaper across the curve, with the belly leading the weakness and the wings lagging the wider move, as Asia fades some of Wednesday’s BoE-driven rally. TYZ2 last prints just off the base of its 0-09+ range, -0-15+ at 112-12, on healthy enough volume of ~100K.

- An early uptick in Chinese equities (which faded as property names struggled) helped apply some pressure lighter in the session.

- For 10s, the triple top resistance zone in yields (just above 4.00%), drawn off the YtD & ‘09/’10 highs, continues to provide the most meaningful technical area of note.

- Yesterday’s move pulled the 5-/30-Year curve away from cycle flats, but it still sits around -25bp.

- Gilt market moves in lieu of the BoE’s first round of emergency purchases will likely set the tone in London hours, with regional and national German CPI also due.

- NY hours see the final Q2 GDP print, weekly jobless claims and another round of Fedspeak, with Messrs Bullard, Mester & Daly all set to appear. Expect them to stick to the hawkish script.

JGBS: Flattening Holds, Futures Off Best Levels

Thursday’s Tokyo session has been a bit of a catch-up exercise for JGBs.

- That leaves the major cash benchmarks running little changed to 9bp richer, as the curve flattens in lieu of Wednesday’s BoE action.

- Note that 10s haven’t really moved away from the upper limit of the BoJ’s permitted trading band, with participants seemingly willing to keep the pressure on the BAnk.

- Futures have faded a touch in the afternoon, but are still +23 on the day.

- MoF data revealed that last week saw international investors lodge the largest round of net weekly sales of Japanese bonds since mid-June, building on the theme of recent times i.e. offshore participants driving the challenge of the BoJ.

- The latest 2-Year JGB auction went well. Takedown was likely aided by the recent move to multi-month cheaps in outright terms, international investor demand stemming from FX-hedged yield pickup and the BoE’s well-documented Wednesday action, which has allowed core global FI markets to stabilise, for now.

- There hasn’t been much in the way of meaningful domestic news flow, outside of continued speculation surrounding potential forms of support for households re: energy prices and schemes to generate inbound tourism for Japan.

- Looking ahead, labour market data, industrial production, retail sales and the latest round of BoJ Rinban operations headline domestically on Friday.

AUSSIE BONDS: Overnight Gains Held, No Impact From New Monthly CPI Reading

Aussie bond futures stuck within the upper end of their respective overnight ranges during Sydney hours, with XM failing to force a break through its overnight peak on a re-test, while YM fell short of challenging its own post-Sydney high.

- Participants shrugged off the domestic monthly CPI print, even with underlying inflation clearing the 6.0% Y/Y level in August (the RBA currently looks for underlying inflation to hit 6.0% in Q422), while the headline print eased a touch, back to 6.8 Y/Y vs. the 7.0% seen in July.

- Elsewhere, we also saw a 2.1% fall in the job vacancies print (which is measured in Q/Q terms), accompanied by an upward revision to the prior print.

- YM +14.0 & XM +19.0 last, back from their respective session highs, with the major cash ACGB benchmarks running 11-19bp richer on the session. 10s outperformed all day as the space played catch up to Wednesday’s BoE-driven bid in futures/wider core global FI markets.

- Bills run 2-16bp richer through the reds.

- Friday will see A$700mn of ACGB Nov-28 auctioned by the AOFM, as well as the release of the AOFM’s weekly issuance slate and private sector credit data.

NZGBS: Off Best Levels But Still Firmer At The Close

Intermediates led the catch-up rally on Thursday, as NZGBs drew support from Wednesday’s BoE-inspired price action in core global FI markets. That left the major NZGB benchmarks 11-14bp richer across the curve.

- The space moved away from best levels of the session into the weekly round of NZGB supply (which included Apr-27, May-32 & May-41 paper). The auctions ultimately passed smoothly enough, allowing fresh richening into the bell, albeit not enough for the space to force a retest of the day’s richest levels.

- The latest ANZ business survey saw an uptick for both the confidence (back to near enough flat) and conditions (which remains deep in negative territory) metrics, with the inflationary measures remaining “intense,” while there was only a “slight easing” in inflation expectations.

- ANZ consumer confidence and building permits data round off this week’s domestic data releases on Friday.

- Next week’s RBNZ monetary policy decision provides the major upcoming domestic risk event, with a touch above 50bp of tightening still priced and a terminal rate of just over 4.80% priced in, which is ultimately little changed on the day.

FOREX: Risk-Off Flows Restart After Wednesday's Pause

Early Asia-Pac trade saw a reversal of Wednesday's risk rebound amid suspected profit taking by regional players. With the BoE's bond-buying intervention already in the books, concerns over the UK government's fiscal plans and the prospect of further aggressive Fed tightening resurfaced. The re-established negative risk tone remained firm through the session, with wires carrying little to alter that trend.

- The greenback outperformed all its G10 peers, with upticks in U.S. Tsy yields facilitating this dynamic. E-minis operated in the red, generating demand for safe haven currencies, with JPY and CHF strengthening alongside USD as a result.

- USD/JPY added ~30 pips, even as one-month option skews dropped. Slight widening in U.S./Japan 10-year yield spread helped push the rate higher.

- Cable gave away nearly 100 pips as the sterling came under renewed pressure linked to Chancellor Kwarteng's sweeping tax reduction plans.

- USD/CNH advanced, then caught a breather as the PBOC pushed its fixing error back out to -729 pips, but promptly resumed gains. The rate's upswing was capped at the CNH7.2 mark.

- Yuan weakness created unfavourable backdrop for the Antipodeans, with the kiwi pacing losses in G10 FX space. The uptick in AUD/NZD was out of sync with the move lower in AU/NZ 2-year swap spread.

- On the global data docket we have U.S. initial jobless claims and third reading of Q2 GDP, German consumer inflation figures and Canadian GDP. Another hefty round of central bank rhetoric is inbound, with Fed, ECB, BoE and Riksbank members due to speak.

ASIA FX: Dips In Most USD/Asia Pairs Supported

In line with the majors, most USD/Asia pairs have moved above lows seen in the NY session. USD/CNH climbed, but couldn't get beyond 7.2000. THB has outperformed, with USD/THB back to 38.10/15. The focus tomorrow is on China PMI prints for September and the RBI interest rate decision, where a 50bps hike is expected.

- USD/CNH dips have been supported. The CNY fixing went back to a wide surprise, while the actual outcome was slightly below yesterday's (7.1102, versus 7.1107). The market looked to take the pair back through 7.2000, but we couldn't breach this level and we are now around 7.1900.

- USD/KRW couldn't sustain early lows sub 1430. Some resistance is evident ahead of 1440. Equities are higher (+1.25%), but we are away from best levels.

- USD/TWD remains below recent highs of 31.90. Onshore equities are also higher, but not as firm as Kospi gains. The CBC Governor appeared to walk back earlier comments in the week that the central bank would put in place FX controls in the event of severe outflows.

- Spot USD/IDR has dropped in sync with most USD/Asia crosses, catching up with overnight greenback sales. The rate last sits -21 figs at 15,242, albeit up from session lows, with familiar technical contours broadly intact.

- Spot USD/PHP is edging away from record highs printed Wednesday at 59.005. The pair last deals -0.05 at 58.938. Foreign investors were net sellers of $10.02mn in Philippine stocks Wednesday, with the PSEi sinking deeper into bear market territory. The index has recovered today, adding ~1.3% thus far.

- USD/THB is lower, dipping back to 38.13, around 0.65% below yesterday's closing levels. Some catch up from overnight USD weakness is in play. The BoT didn't appear too concerned about FX weakness, following last night's modest 25bps hike.

CHINA: PMIs On Tap Tomorrow

A reminder that the China September PMIs print tomorrow. The consensus looks for a further recovery in the manufacturing PMI to 49.7 from 49.4 in August. The range of estimates is 49.0 to 50.5. For services, the market expects an easing in conditions to 52.4 from 52.6. Not surprisingly, the range of estimates is wider for this print: 49.5 to 53.0. The Caixin manufacturing PMI is expected to be unchanged at 49.5.

- August real activity data surprised on the upside, particularly in terms of retail sales, so the services PMI could come under great focus tomorrow.

- For the services sector, recall that the large city of Chengdu was locked down for a good proportion of September, so this may have weighed on services activity in the month.

- The Standard Chartered SME survey has also already printed for September, and it eased back to 50.90 in terms of the headline index. This is the second monthly decline for the index, although we remain above May lows of 48.50.

MNI RBI Preview - September 2022: Risks Tilted Towards 50bps Hike

EXECUTIVE SUMMARY

- We see the balance of risks tilted towards a 50bps hike tomorrow from the RBI, given the current inflation/growth backdrop. The latest inflation print was firmer than expected at 7% y/y. Since peaking in April (7.80%), consumer price pressures have moderated, albeit remaining fairly sticky around the 7% level. We remain comfortably above the upper inflation target limit for the RBI of 6%.

- On the growth front, the Q2 GDP report, whilst delivering a headline miss, had solid underlying details. Partial growth indicators have been mixed in recent months, but aren’t suggesting a sharp slowdown in growth. External financial market developments have also turned more hawkish since the last policy meeting.

- This backdrop argues for a 50bps move, with the key objective of bringing inflation risks under control, likely to outweigh growth concerns. If the real policy rate was closer to flat (currently -160bps), the case for a smaller move would arguably be stronger.

- Click to view the full preview:

EQUITIES: Relief Rally In APAC

Major regional indices are all in the green, as markets have risen in sympathy with the US gains overnight. Gains have ranged from 0.30% to more than 2%. US futures have fluctuated today, but have edged back towards positive territory this afternoon. Eminis were last around 3735, up from the 3718 low earlier in the session.

- China stocks continue to exhibit a low beta to broader global moves. At this stage, the Shanghai Composite index is up 0.27%, although the property sub-index is lagging, down a further 1.1% today. We highlighted woes for developer CIFI Holdings yesterday.

- The HSI has fared better, up +1.25%, albeit away from earlier highs. HSI Tech gains are around the same (+1.2%).

- The Kospi (+1.30%) and TWSE (+0.65%) are firmer as well, support from the official sector helping. South Korea stated late yesterday it was reactivating the stock stabilization fund and may ban short sales. In Taiwan, the Labor Pension Fund pledged to buy up to $70bn TWD of local equities before year end.

- The ASX200 has outperformed, up around 2%, with financial and resource names leading the rebound.

OIL: Supply Outlook Coming Back Into Focus

Brent crude is just below $89/bbl currently, modestly off NY highs, unwinding only 0.4% of the +3.5% rally yesterday. We haven't been able to sustain earlier gains beyond $89.50/bb. WTI is close to $82/bbl, displaying a similar trajectory.

- Crude is still moving with broader risk appetite to some degree. Today's rebound in the USD has no doubt weighed on sentiment.

- Still, the supply backdrop is likely to remain the main driver of sentiment as we push into next week. The energy conflict in the EU is unlikely to improve in the near term, which should continue to see some spill over to oil prices.

- Next week's OPEC+ meeting (October 5th) could deliver fresh production cuts as well. A number of sell-side analysts are suggesting as much.

- Overnight, we also had a surprise drawdown in both US crude and gasoline inventories, which suggests the demand backdrop is not as soft as feared.

- Tomorrow China PMIs print, which will also be eyed to gauge China's recovery/commodity demand outlook.

GOLD: Consolidates After Rebounding To Weekly High

Gold is down from overnight highs, last tracking close to $1654. This is around 0.35% down from NY closing levels. This comes after yesterday’s near 2% gain.

- There appears to be some support for the precious metal ahead of $1650. Note there were a number of highs just below this point at the start of the week as well. Below that we could also see buying interest emerge in the low $1640 region.

- On the topside, overnight highs came in just under $1663. Beyond that is numerous highs closer to $1680 from earlier in September.

- Gold continues to follow broader USD gyrations for the most part. The move lower today has coincided with the DYX back above 113, while a slight recover in UST yields has also likely weighed at the margin.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 29/09/2022 | 0700/0900 |  | EU | ECB Panetta Intro at ECOFIN Hearing | |

| 29/09/2022 | 0700/0900 | *** |  | ES | HICP (p) |

| 29/09/2022 | 0800/1000 | *** |  | DE | Bavaria CPI |

| 29/09/2022 | 0800/1000 | | EU | ECB de Guindos Speech at BIS/Bank of Lithuania | |

| 29/09/2022 | 0800/1000 |  | IT | PPI | |

| 29/09/2022 | 0815/1015 | | EU | ECB Elderson Speech at Nederlandsche Bank & OMFIF | |

| 29/09/2022 | 0830/0930 | ** |  | UK | BOE Lending to Individuals |

| 29/09/2022 | 0830/0930 | ** | | UK | BOE M4 |

| 29/09/2022 | 0900/1100 | ** | | EU | Economic Sentiment Indicator |

| 29/09/2022 | 0900/1100 | * | | EU | Consumer Confidence, Industrial Sentiment |

| 29/09/2022 | 0900/1100 | * | | EU | Business Climate Indicator |

| 29/09/2022 | 0900/1100 | *** | | DE | Saxony CPI |

| 29/09/2022 | 0930/1130 | | EU | ECB de Guindos Opens ECB Research Workshop | |

| 29/09/2022 | 1130/1230 | | UK | BOE Ramsden Panels Lithuania CB/BIS Conference | |

| 29/09/2022 | 1200/1400 | *** | | DE | HICP (p) |

| 29/09/2022 | 1230/0830 | *** |  | CA | Gross Domestic Product by Industry |

| 29/09/2022 | 1230/0830 | * | | CA | Payroll employment |

| 29/09/2022 | 1230/0830 | ** |  | US | Jobless Claims |

| 29/09/2022 | 1230/0830 | *** | | US | GDP (3rd) |

| 29/09/2022 | 1330/0930 | | US | St. Louis Fed's James Bullard | |

| 29/09/2022 | 1400/1000 | ** | | US | WASDE Weekly Import/Export |

| 29/09/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 29/09/2022 | 1500/1600 | | UK | BOE Tenreyro Panellist at Centre for Economic Policy Research | |

| 29/09/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 29/09/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 29/09/2022 | 1700/1300 | | US | Cleveland Fed's Loretta Mester | |

| 29/09/2022 | 1700/1900 | | EU | ECB Lane Panels ECB/Cleveland Fed Conference | |

| 29/09/2022 | 1800/1400 | *** |  | MX | Mexico Interest Rate |

| 29/09/2022 | 2045/1645 | | US | San Francisco Fed's Mary Daly |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.