Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- JEFFERSON: STABLE PRICES SET STAGE FOR EXPANSIONS THAT BOOST INCLUSIVE GROWTH (RTRS)

- BRACE FOR MORE CHANGE, SAYS LIZ TRUSS THE DISRUPTOR (THE TIMES)

- RBNZ HIKES 50BP, CONTINUES TO TIGHTEN "AT PACE" (MNI)

- ECB MUST AT A 'MINIMUM' STOP STIMULUS, LAGARDE SAYS (RTRS)

- ECB’S PANETTA WON’T BE NEXT ITALIAN FINANCE MINISTER (BBG)

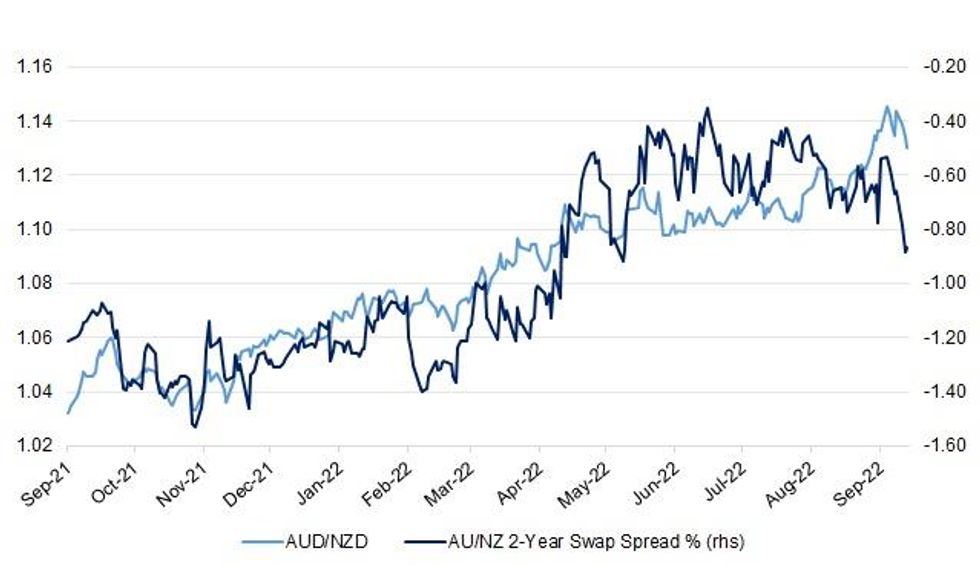

Fig. 1: AUD/NZD Vs. AU/NZ 2-Year Swap Spread

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

UK

FISCAL/ECONOMY/POLITICS: Liz Truss will warn today of more disruption ahead as the price of economic growth, after another day of cabinet infighting threatened to derail her first party conference as leader. (The Times)

FISCAL: After 24 hours of confusion, the Treasury has confirmed that it has brought forward the publication date of long-awaited financial plans. (BBC)

FISCAL: Prime Minister Liz Truss has not ruled out increasing the retirement age to help balance the nation's books. (BBC)

FISCAL/POLITICS: Crunch votes to implement last week’s mini-Budget will not take place until next spring, The Telegraph understands, putting off potential rebellions until 2023. (Telegraph)

FISCAL/POLITICS: Liz Truss is coming under pressure from Tory MPs to ensure benefits rise in line with prices, with minister Penny Mordaunt arguing it "makes sense". (BBC)

POLITICS: Liz Truss will on Wednesday attempt to rally Conservative MPs behind her faltering leadership, at a party conference that has descended into acrimony, cabinet infighting and confusion. (FT)

ENERGY: British Prime Minister Liz Truss said on Tuesday the government was looking at long term energy contracts with other countries but had not yet signed any deals. (RTRS)

EUROPE

ECB: The European Central Bank must at a "minimum" stop stimulating the economy through its monetary policy, the ECB's President Christine Lagarde said on Tuesday, in a likely reference to raising interest rates back to "neutral" territory. This is defined as a level of interest rate that neither stimulates nor curbs economic growth, all else being equal. (RTRS)

FISCAL: Two top European Union officials on Tuesday called for joint borrowing to help the 27-nation bloc navigate the energy crunch together, after Germany faced criticism for going its own way with huge subsidies its peers could never afford. (RTRS)

GERMANY: Germany is in advanced talks to provide billions of euros in additional guarantees to Sefe, formerly Gazprom Germania, to ensure the company can honour a major contract to supply gas to German importer VNG, two people familiar with the matter said. (RTRS)

FRANCE: France on Tuesday started the process to fully nationalise debt-laden nuclear power group EDF, seeking to secure greater control of its energy supplies as Europe scrambles to replace Russian gas. (RTRS)

ITALY: Fabio Panetta, a member of the European Central Bank’s Executive Board, won’t be the next Italian finance minister despite speculation linking him with the position, according to a person familiar with the matter. (BBG)

IRELAND: Ireland's central bank pushed up its 2023 inflation projections and revised down its forecast for economic growth for the third quarter in row, but expects the drag on disposable incomes to ease in the second half of next year. (RTRS)

IRELAND: Ireland collected 26% more tax in the first nine months of the year than the same period in 2021 following another huge surge in corporate receipts and large increases in VAT and income tax, finance ministry data showed on Tuesday. (RTRS)

FINANCE: Europe stands ready to use “every lever” to keep the financial system stable as Russia’s invasion of Ukraine undermines the region’s energy supplies, a senior European Union official said on Tuesday. (BBG)

ENERGY: The European Union can learn from Spain and Portugal's mechanism to cap the price of gas used in power generation, although the scheme is not suitable to immediately roll out across Europe, the EU's head of energy policy said on Tuesday. (RTRS)

ENERGY: European Union member countries, afflicted by soaring prices for natural gas, should coordinate more to make the bloc a single energy buyer, German Economy Minister Robert Habeck said, and the United States should show more solidarity with European countries that supported America during periods of high oil prices. (RTRS)

U.S.

FED: Stable prices that lead to long economic expansions set the stage for economic gains for the least well off, Federal Reserve Governor Philip Jefferson said on Tuesday. (RTRS)

FED: San Francisco Federal Reserve Bank President Mary Daly on Tuesday said the U.S. central bank has the tools and the knowledge to bring down high inflation, and will use them to do so. (RTRS)

FISCAL: Treasury Secretary Janet Yellen denied Tuesday an unconfirmed report that President Joe Biden would replace her after the November midterm elections, saying she plans to stay on as head of the agency. (CNBC)

POLITICS: U.S. President Joe Biden's public approval rating edged lower this week and was close to the lowest level of his presidency, with just five weeks to go before the Nov. 8 midterm elections, a Reuters/Ipsos opinion poll completed on Tuesday found. (RTRS)

EQUITIES: Elon Musk has reversed course and is again proposing to buy Twitter for $54.20 a share, according to a regulatory filing on Tuesday. Twitter shares surged 22% to $51.83 when they reopened. (CNBC)

OTHER

GLOBAL TRADE: Implementing tech export controls on China is challenging due to “civil-military fusion”, deputy economics minister C. C. Chen says at briefing. Taiwan will adopt measures to prevent its tech from being used by PLA. (BBG)

U.S./CHINA: The Financial Times reported that US is proposing to impose export controls in an effort to slow Chinese from obtaining semiconductors and chipmaking equipment for supercomputers and other military-related purposes. (FT)

U.S./CHINA/TAIWAN: If China imposed a maritime blockade of Taiwan, the U.S. and its allies would have the capability to break it, says Adm. Samuel Paparo, commander of the U.S. Pacific Fleet. (Nikkei)

CHINA/TAIWAN: Taiwan warned it would view any incursion of China’s planes or drones into the island’s airspace as a first strike, Defense Minister Chiu Kuo-cheng told lawmakers, in response to questions. (BBG)

GEOPOLITICS: The Solomon Islands refused to sign the US government’s Pacific partnership deal until “indirect” references to the Chinese government were removed, with Foreign Minister Jeremiah Manele saying his country did not want to “choose sides.” (BBG)

RBNZ: The Reserve Bank of New Zealand raised interest rates by 50bp to 3.5% and signalled it would continue to tighten policy "at pace" as it revealed a 75bp hike had been discussed. (MNI)

NEW ZEALAND: New Zealand’s annual budget deficit widened much less than forecast as the economy performed better than expected and the government was able to curtail pandemic-related spending. (BBG)

NEW ZEALAND: The price of homes sold by Auckland's largest real estate agency dropped by $47,000 from August to September but by $180,000 since last November. (NZ Herald)

SOUTH KOREA: South Korea’s central bank said annual consumer inflation is expected to stay high at the 5-6% levels, with upside risks, for a considerable period of time. (RTRS)

NORTH KOREA: South Korea and the U.S. military fired a volley of missiles into the sea in response to North Korea's launch of a ballistic missile over Japan, Seoul said on Wednesday, as Pyongyang's longest-range test yet drew international condemnation. (RTRS)

MEXICO: Mexico’s central bank named Stanford-University educated Alejandrina Salcedo Cisneros to be its new chief economist, board member Jonathan Heath said Tuesday. (BBG)

BRAZIL: President Jair Bolsonaro and his leftist challenger Luiz Inacia Lula da Silva are rushing to secure endorsements from key political players from across Brazil as they gear up for the second stretch of the presidential campaign ahead of a Oct. 30 runoff. (BBG)

RUSSIA: Washington's decision to send more military aid to Ukraine poses a threat to Moscow's interests and increases the risk of a military clash between Russia and the West, said Anatoly Antonov, Russia's ambassador to the United States. (RTRS)

RUSSIA: European Union sanctions against Russia are working well, a top European Commissioner said on Tuesday, dismissing as Russian propaganda criticism that EU measures were ineffective and had little impact. (RTRS)

RUSSIA: Russian Finance Ministry plans to borrow directly on financial market through repo mechanism, Vedomosti reports, citing budget documents and Russian Treasury. (RTRS)

SOUTH AFRICA: Eskom has escalated blackouts to Stage 4 from 6pm after generation units at Kendal and Lethabo power stations tripped. (EWN)

METALS: Chile's total copper production fell 10.2% in August to reach 415,500 tonnes, government body Cochilco said on Tuesday. (RTRS)

ENERGY: The operators of two Baltic Sea gas pipelines that linked Russia and Germany until they both sprang major leaks last week said they were unable to inspect the damaged sections because of restrictions imposed by Danish and Swedish authorities. (RTRS)

ENERGY: The European Commission is considering versions of a gas price cap including a possible temporary "flexible" limit on the Dutch Title Transfer Facility price, the EU's head of energy policy said on Tuesday. (RTRS)

ENERGY: European Union finance ministers said on Tuesday they have backed "targeted changes" to how markets operate to ease the strain on energy companies struggling with high prices. (RTRS)

OIL: Saudi Arabia is seeking to raise oil prices at a crucial meeting in Vienna in a move set to anger the US and help Russia. Riyadh, Moscow and other producers are poised to announce deep cuts at a meeting of the Opec+ cartel on Wednesday, according to people with knowledge of the discussions. The size of the cut is still to be agreed but Saudi Arabia and Russia are pushing for reductions of 1mn-2mn barrels a day or more, although these could be phased in over several months. The move would probably trigger US countermeasures, analysts said. (FT)

OIL: The Organization of the Petroleum Exporting Countries and its Russia-led allies are preparing for a potentially contentious meeting on Wednesday, when they gather in-person for the first time in years to discuss a production cut of up to 1.5 million barrels a day that not all players support, OPEC officials said. (WSJ)

OIL: The United States is pushing OPEC+ nations not to proceed with potential deep oil output cuts, a source familiar with the matter told Reuters, as President Joe Biden seeks to prevent U.S. gasoline prices from rising. (RTRS)

OIL: The European Union is advancing work on a price cap for Russian oil under an approach that keeps the U.S.-led effort on track, but holds off on final approval. (WSJ)

OIL: The largest U.S. oil trade groups said on Tuesday that they have "significant concerns" that the Biden administration is considering limiting fuel exports to lower consumer prices and urged top officials to take the option off the table, according to a letter seen by Reuters. (RTRS)

OIL: The US isn’t considering an additional release from the Strategic Petroleum Reserve despite expectations that OPEC+ nations could cut production. Oil rallied for a second day. And US aluminum producer Alcoa Corp. told the London Metal Exchange that Russian metal shouldn’t be traded on the benchmark industrial metals bourse, according to people familiar with the matter. (BBG)

OVERNIGHT DATA

JAPAN SEP, F JIBUN BANK SERVICES PMI 52.2; FLASH 51.9

JAPAN SEP, F JIBUN BANK COMPOSITE PMI 51.0; FLASH 50.9

September brought along a more positive month for Japan's service sector as activity levels returned to growth. The announcement that restrictions on foreign tourism will be lifted from October should also help support greater economic activity levels across Japan over the coming months. (S&P Global)

AUSTRALIA SEP, F S&P GLOBAL SERVICES PMI 50.6; FLASH 50.4

AUSTRALIA SEP, F S&P GLOBAL COMPOSITE PMI 50.9; FLASH 50.8

Despite recent RBA interest rate decisions and current global inflationary pressures, latest survey data displayed evidence that the Australian private sector economy may be able to avoid the recessions that are likely to be seen elsewhere. Following five months of slowing growth, Australian service companies registered a stronger improvement in business activity. New business also recorded accelerated growth with panel members mentioning that a sustained improvement in COVID-19 related challenges helped strengthen underlying demand. (S&P Global)

NEW ZEALAND SEP CORELOGIC HOUSE PRICES +2.8% Y/Y; AUG +5.8%

SOUTH KOREA SEP CPI +5.6% Y/Y; MEDIAN +5.7%; AUG +5.7%

SOUTH KOREA SEP CPI +0.3% M/M; MEDIAN +0.4%; AUG -0.1%

SOUTH KOREA SEP CORE CPI +4.5% Y/Y; MEDIAN +4.4%; AUG +4.4%

MARKETS

SNAPSHOT: RBNZ Pushes On, No Pivot Evident

Below gives key levels of markets in the second half of the Asia-Pac session:

- Nikkei 225 up 107.68 points at 27099.89

- ASX 200 up 116.41 points at 6815.7

- Chinese markets are closed.

- JGB 10-Yr future down 3 ticks at 149, yield up 2.7bp at 0.249%

- Aussie 10-Yr future up 7 ticks at 96.32, yield down 7.6bp at 3.654%

- U.S. 10-Yr future -0-03+ at 113-12+, yield down 0.77bp at 3.625%

- WTI crude down $0.31 at $86.21, Gold down $5.19 at $1720.99

- USD/JPY down 7 pips at Y144.06

- JEFFERSON: STABLE PRICES SET STAGE FOR EXPANSIONS THAT BOOST INCLUSIVE GROWTH (RTRS)

- BRACE FOR MORE CHANGE, SAYS LIZ TRUSS THE DISRUPTOR (THE TIMES)

- RBNZ HIKES 50BP, CONTINUES TO TIGHTEN "AT PACE" (MNI)

- ECB MUST AT A 'MINIMUM' STOP STIMULUS, LAGARDE SAYS (RTRS)

- ECB’S PANETTA WON’T BE NEXT ITALIAN FINANCE MINISTER (BBG)

US TSYS: Antipodean Influence Offset By Issuance

TYZ2 has stuck to a narrow 0-07+ range in Asia-Pac hours, last printing around the mid-point of that range, -0-03 at113-13.

- This leaves the major cash Tsy benchmarks at essentially unchanged levels across the curve.

- The cross-market impact of richer NZGBs & ACGBs post-RBNZ (where the expected 50bp hike was delivered and the Bank just about managed to stay away from a decisively hawkish shift) was cancelled out by the marketing of a US$ multi-tranche round of issuance from the Philippines (consisting of 5-, 10- & 25-Year paper).

- ADP employment data, the ISM services survey and Fedspeak from Kashkari & Bostic headline Wednesday’s NY docket.

- Elsewhere, the latest OPEC+ decision will cross on Wednesday, with various source reports prepping market participants for a sizable output cut (in headline quota terms, at a minimum), which supported crude oil over the first couple of sessions of the week (putting a bid into U.S. breakevens).

JGBS: Sideways Trade Continues

JGB futures oscillated either side of unchanged levels during Tokyo trade, dealing -3 into the bell, sticking to a tight range, while cash JGBs sit 1bp richer to 1bp cheaper across the curve. There hasn’t been much in the way of a meaningful domestic catalysts, leading to a lack of conviction in JGB trade.

- Offer/cover ratios nudged higher in the latest round of BoJ Rinban operations, perhaps as participants use the move away from recent cheaps in those maturities as a selling opportunity:

- 1- to 3-Year: 3.59x (prev. 2.74x)

- 3- to 5-Year: 2.50x (prev. 1.60x)

- Comments from PM Kishida underscored the BoJ’s independence when it comes to setting monetary policy, while he refrained from commenting on the outlook for the JPY.

- Weekly international security flow data and the latest liquidity enhancement auction for off-the-run 5- to 15.5-Year JGBs will be seen on Thursday.

AUSSIE BONDS: 10s Lead Auction/RBNZ-Inspired Bid, Off Best Levels Into The Bell

A solid enough round of ACGB supply and the trans-Tasman spill over from the latest RBNZ decision (universally expected and fully priced 50bp OCR hike delivered and a lack of a decisively hawkish shift, just about) supported ACGBs, allowing the space to add to the gains that came on the back of the overnight session uptick in futures.

- XM managed to show through its overnight peak, although YM didn’t, with both contracts pulling back from best levels alongside a similar move in U.S. Tsys. That leaves YM +3.0 & XM +8.0, with the major cash ACGB benchmarks running 2-8bp richer, as 10s lead the bid.

- Bills sit -4 to +4 through the reds, with a lack of net movement in RBA terminal rate pricing, with OIS still pricing a peak rate of ~3.60%.

- Looking ahead, monthly trade balance data headlines the domestic docket on Thursday.

AUSSIE BONDS: AOFM sells A$800mn of the 1.25% 21 May 2032 Bond, issue #TB158:

The Australian Office of Financial Management (AOFM) sells A$800mn of the 1.25% 21 May 2032 Bond, issue #TB158:

- Average Yield: 3.6829% (prev. 3.6790%)

- High Yield: 3.6850% (prev. 3.6825%)

- Bid/Cover: 2.8188x (prev. 2.4825x)

- Amount allotted at highest accepted yield as percentage of amount bid at that yield: 91.9% (prev. 4.1%)

- Bidders 42 (prev. 40), successful 19 (prev. 21), allocated in full 12 (prev. 14)

NZGBS: NZGBs Richer Despite RBNZ Debating 75bp Hike

NZGBs finished 16-18bp richer on Wednesday, bull steepening at the margin.

- Yesterday’s dovish RBA surprise provided the catalyst for the bid in early Wednesday trade.

- Later in the day we saw NZGBs initially cheapen as the RBNZ delivered the universally expected and fully priced 50bp rate hike (as it became apparent that 50 & 75bp hikes were discussed, indeed, the 50bp decision was made “on balance”), although the lack of a decisive hawkish shift (there was a high bar for such a move) allowed a bid to come back in.

- The RBNZ reiterated the need for tightening to be conducted at pace, while the proximity to yesterday’s dovish RBA surprise likely had some readthrough when it came to initial price action.

- There hasn’t been meaningful, lasting movement in the market pricing of RBNZ tightening expectations, with the terminal rate now seen at 4.55%, after some contained gyrations post-MPR.

- There isn’t much of note on Thursday’s local docket.

EQUITIES: Bid Extends In Asia; Hang Seng Plays Catch Up

Most Asia-Pac equity indices are in the green at writing, tracking a positive lead from Wall St. on lingering speculation of a slowdown in Fed tightening amidst softer economic data.

- The Hang Seng (+5.3%) outperformed, playing catch up to regional equities on its first day back from a holiday. The HSTECH (+7.4%) contributed the most to gains, adding to strength in China-based stocks (Hang Seng China Enterprises Index: +5.7%).

- The ASX200 deals 1.7% firmer, building on Tuesday’s ~3.8% higher close, rising to fresh two-week highs amidst the repricing of expectations around the RBA’s terminal rate. Rate-sensitive tech leads the bid, with the ASX All Tech Index sitting 3.7% better off at typing.

- The Nikkei 225 is 0.4% better off at writing, on track to close higher for a third straight session, extending a move off of 15-week lows observed on Monday. Large caps such as Softbank (+2.0%) and Fast Retailing (+1.1%) lead the way higher, offsetting weakness in consumer staples.

- E-minis sit 0.4-0.5% weaker at writing, paring a little of their recent gains after a two-day rally (+5.5-5.9% apiece) saw the contracts record fresh two-week highs on Tuesday.

OIL: Holding Recent Gains As OPEC+ Output Cuts Eyed; U.S Inventory Data Due

WTI and Brent are ~$0.30 softer apiece, operating within ~$1 of their respective multi-week highs made on Tuesday, with participants on watch for the size of potential output cuts arising from the OPEC+ meeting later on Wednesday.

- To elaborate on the latter, OPEC+ will meet in Vienna amidst elevated uncertainty over the size of a possible cut in collective output targets, as various source reports in recent days have pointed to quota reductions ranging from 0.5-2mn bpd.

- Some will also be on the lookout for extra, unilateral output cuts from Saudi Arabia, a measure the kingdom has taken before in the past.

- Note that RTRS source reports previously highlighted that OPEC+ missed output targets by just under 3mn bpd for Jul, while Argus sources placed quota shortfalls at ~3.4mn for Aug.

- U.S. API data on Tuesday saw reports point to a large, surprise drawdown in crude inventories, with a decline in gasoline and distillate stocks and a build in Cushing hub stockpiles reported as well.

- Looking ahead, weekly U.S. EIA data is due, with BBG median estimates calling for a build in crude inventories.

GOLD: Consolidating Below Three-Week Highs

Gold deals ~$6/oz softer to print ~$1,720/oz, backing away from three-week highs made on Tuesday (at ~$1,729.5/oz), but holding on to the bulk of that session’s gains at typing.

- To recap, the precious metal closed ~$26/oz firmer on Tuesday, drawing support from the miss in JOLTS job opening figures (pointing to softening labour demand), with the DXY hitting fresh two-week lows after.

- The improvement in sentiment likely reflects optimism from some quarters re: a slowdown in Fed tightening amidst soft U.S. economic data prints.

- Consensus re: a slower pace of Fed hiking remains far from certain however, with Nov FOMC dated OIS now pricing in ~70bp of tightening at that meeting, operating at its highest level in a week.

- Looking ahead, participants will be on the lookout for more employment data due later this week, capped by NFPs on Friday.

- From a technical perspective, gold has established a short-term bull cycle, having broken above its 20-Day EMA and trendline resistance. Initial resistance is seen at ~$1,735.1 (Sep 12 high and key resistance), while support is seen at $1,659.7 (Oct 3 low).

FOREX: RBNZ's Hawkish Determination Boosts Kiwi But Risk Aversion Limits Gains

New Zealand dollar appreciated as the RBNZ raised its key policy rate by the expected 50bp and reaffirmed its hawkish credentials via another strong-worded statement. The tone of today's interim monetary policy review disappointed those who had expected the RBNZ to signal imminent slowdown in the pace of its rate hikes, after the RBA delivered a smaller-than-expected 25bp rate hike the day before.

- The RBNZ echoed most of it rhetoric from the August statement when it comes to the main policy objectives, while for the first time making an explicit mention of a debate on raising interest rates by 75bp. Comments on FX dynamics intimated greater sense of concern with the weakening exchange rate and its impact on imported inflation.

- Renewed risk aversion prompted NZD/USD to gradually erase its post-RBNZ gains but the kiwi dollar outperformed on other crosses. AUD/NZD probed the water below NZ$1.1300 before settling just above that level amid a limited round trip in AU/NZ 2-year swap spread.

- Cautious mood supported safe-haven currencies at the expense of most G10 high-betas as e-mini futures faltered after a two-day rally in U.S. equity benchmarks.

- Sterling resumed losses after cable recovered to its pre-mini budget levels, as jitters resurfaced ahead of PM Truss' address to the Tory party conference today.

- Financial markets in mainland China and India were closed for local public holidays.

- U.S. ADP employment change, trade balance, as well as a suite of Services PMI readings from across the globe will take focus after Asia hours. Fed's Bostic & Kashkari are set to speak.

FX OPTIONS: Expiries for Oct5 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9800(E2.0bln), $0.9930-36(E1.2bln)

- USD/JPY: Y143.85-05($798mln)

- EUR/JPY: Y142.20(E809mln)

- AUD/USD: $0.6650(A$629mln)

- USD/CAD: C$1.3800($585mln)

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 05/10/2022 | 0600/0800 | ** |  | DE | Trade Balance |

| 05/10/2022 | 0645/0845 | * |  | FR | Industrial Production |

| 05/10/2022 | 0715/0915 | ** |  | ES | IHS Markit Services PMI (f) |

| 05/10/2022 | 0745/0945 | ** |  | IT | IHS Markit Services PMI (f) |

| 05/10/2022 | 0750/0950 | ** | | FR | IHS Markit Services PMI (f) |

| 05/10/2022 | 0755/0955 | ** | | DE | IHS Markit Services PMI (f) |

| 05/10/2022 | 0800/1000 | ** |  | EU | IHS Markit Services PMI (f) |

| 05/10/2022 | 0830/0930 | ** |  | UK | IHS Markit/CIPS Services PMI (Final) |

| 05/10/2022 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 05/10/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 05/10/2022 | 1215/0815 | *** | | US | ADP Employment Report |

| 05/10/2022 | 1230/0830 | * |  | CA | Building Permits |

| 05/10/2022 | 1230/0830 | ** | | US | Trade Balance |

| 05/10/2022 | 1345/0945 | *** | | US | IHS Markit Services Index (final) |

| 05/10/2022 | 1400/1000 | *** | | US | ISM Non-Manufacturing Index |

| 05/10/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 05/10/2022 | 2000/1600 | | US | Atlanta Fed's Raphael Bostic |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.