Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

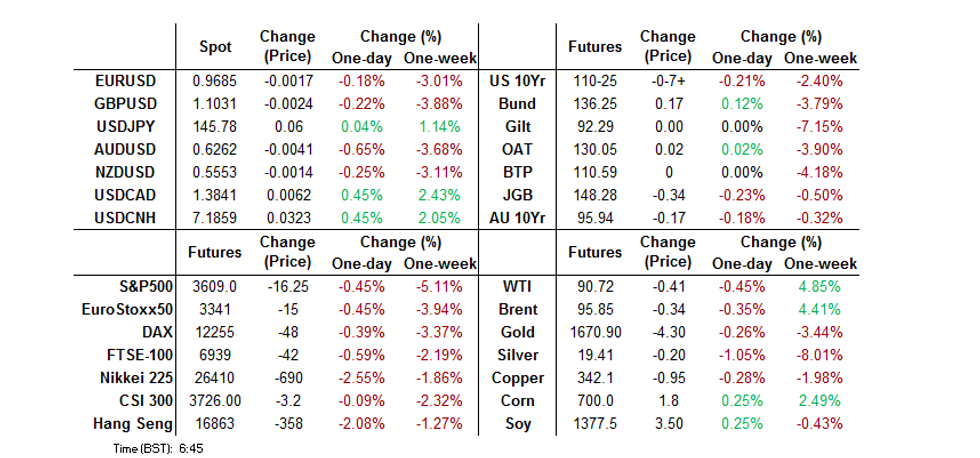

- Tsys were pressured overnight, with 10-Year yields back around 4.00%, operating just below the triple top drawn off '09, '10 & YtD highs, while the USD firmed in Asia.

- E-minis were pressured against this backdrop, although we didn't get much in the way of meaningful headline flow.

- Major data releases going forward are limited to the UK labour market report. Elsewhere, speeches are due from Fed's Mester, ECB's Lane & Villeroy, BoE's Bailey & Cunliffe.

MNI Insight: Gloomier Global Growth Outlook Positive For USD

EXECUTIVE SUMMARY

- Global growth and trade projections are being revised down, especially for 2023. The IMF is expected to do the same when it publishes the World Economic Outlook on October 11. Concerns remain centred around tightening global monetary policy, the European energy crisis and a weaker China.

- The softer global backdrop tends to favour the USD on flight to quality assets. Global trade trends are also highly correlated with EM FX.

- Leading indicators such as the PMIs, Baltic Freight Index and metal prices all suggest a slowdown in trade and therefore also in production. This is likely to hurt non-China Asia significantly more than the OECD and China itself.

- For the full piece please click here: Global growth Oct 22a.pdf

US TSYS: Block Sales Help To Keep Pressure On

TYZ2 hovers just above the base of its 0-13+ range into London hours, last -0-09+ at 110-23, on solid volume of ~120K, operating just above technical support at the contract’s cycle low (110-19). Cash Tsys run 3.5-11.5bp cheaper across the curve, with 10s leading the way lower as that benchmark hovers just below 4.00%, with the round number protecting the triple top resistance area drawn off the ’09, ’10 & YtD highs.

- Spill over from Monday’s cheapening was aided by several rounds of block sales in TY & FV futures, alongside a USD bid, with Tsys extending on yesterday’s weakness as cash trade opened after the elongated Columbus Day weekend.

- There wasn’t much in the way of meaningful headline flow to drive the move, with the space shrugging off the latest round of risk-negative COVID headlines out of China, after the state-backed People’s Daily reiterated the need for the country’s ZCS, while a fresh mass testing scheme was unveiled in the city of Shanghai.

- Looking ahead, Tuesday’s NY docket will see the release of the NFIB small business optimism index, Fedspeak from Mester and 3-Year Tsy supply.

JGBS: Curve Steepens On Wider Weakness In Core Global FI Markets

JGB futures operate just above worst levels into the bell, -33 vs. Friday’s settlement, after Tokyo returned from an elongated weekend and reacted to the weakness witnessed in wider core global FI markets.

- Cash JGBs are flat to 7bp cheaper across the curve, with the super-long end leading the way lower owing to the relative lack of BoJ control in that area of the curve.

- 7s underperform surrounding paper owing to the weakness in futures, while 10s are little changed as they operate just shy of the BoJ’s yield cap.

- An FT interview with PM Kishida showed the leader’s support for the BoJ’s ultra-loose policy settings, even as the JPY tumbles, while Kishida indicated that he intends to allow Governor Kuroda to serve his full term atop the BoJ (which expires in April ’23).

- A steady to lower round of offer/cover ratios in the BoJ Rinban operations covering 1- to 25-Year JGBs, coupled with the FT story, seemed to facilitate a very modest bid during the early rounds of Tokyo afternoon dealing before fresh weakness set in.

- Elsewhere, Japanese policymakers reiterated well-trodden verses surrounding the FX market, alongside suggestions that the U.S. has shown “a certain extent” of understanding re: Tokyo’s FX intervention in September.

- Looking ahead, 30-Year JGB supply headlines the domestic docket on Wednesday, with lower tier economic data also due.

AUSSIE BONDS: Dragged Lower By Broader Weakness And Semi-Issuance Pricing

The wider weakness observed in core global FI futures allowed the major Aussie bond futures to extend through their respective overnight bases during Tuesday’s Sydney session, with hedging around the pricing of TCV’s new Sep-36 benchmark bond also applying some pressure late in the day.

- That leaves YM -9.0 and XM -15.0 into the bell, operating just above worst levels, as U.S. Tsys nudge away from session cheaps.

- Wider cash ACGB trade has seen the major benchmarks cheapen by 9-16bp, with the curve bear steepening as super-long paper leads the way lower.

- Bills sit flat to 10bp cheaper on the day, with RBA dated OIS now pricing a terminal rate of just under 4.0%, ~7bp or so higher on the day.

- Local data saw a firming of NAB business conditions, a moderation in business confidence (to around long-run average levels), a modest downtick in Westpac consumer confidence (albeit with very split directions in the reading, intra-month) and a sight slowing of CBA household spending in Y/Y terms (with a negative M/M print seen).

- An address from RBA Assistant Governor (Economic) Ellis on “The Neutral Rate: The Pole-star Casts Faint Light,” headlines the domestic docket on Wednesday. Elsewhere, A$800mn of ACGB Nov-32 supply is due.

NZGBS: NZGBs Cheaper On The Global Drumbeat

The broader weakness observed in core global FI markets since Monday’s local close dragged NZGBs lower in early Tuesday trade, before fresh pressure for global core FI markets resulted in additional cheapening, with the major benchmarks running 12-13bp cheaper across the curve at the close, bear steepening.

- In the RBNZ's annual report Governor Adrian Orr reiterated the idea that "there is more work to do. Increasing the OCR is the most effective way we can reduce inflation and support maximum sustainable employment over the coming years, consistent with our monetary policy Remit. That is one of our key roles as a central bank and the best thing we can do for the long term economic wellbeing of all New Zealanders."

- RBNZ dated OIS indicated terminal rate pricing of just over 4.90%, advancing ~10bp on the day, with the move higher in global yields pushing that metric upwards as we moved through the session.

- Lower tier local data failed to impact the space in a meaningful manner, although firmer card spending data in September would have aided the cheapening in the background.

- Looking ahead, REINZ house sales and net migration data is due Tuesday.

FOREX: Risk Aversion Evident, Iron Ore Dip Weighs On AUD, JPY Intervention Talk Returns

Participants rushed to safety as U.S. e-mini futures erased their initial uptick, while U.S. Tsy yield curve bear steepened as cash trading re-opened. The BBDXY index gained for the fifth consecutive day as its 1-month implied volatility was closing on its cyclical highs. There was little in the way of fresh risk-off headline flow, but familiar concerns continued to linger, affecting Japanese, South Korean and Taiwanese players as they returned from holidays.

- Spot USD/JPY traded within touching distance from a cyclical high (Y145.90) last printed on Sep 22, when Japanese officials intervened to prop up the yen. Renewed jawboning may have lent additional support to the yen, as officials vowed readiness to act decisively if needed. Japan's FX czar Kanda said he could order an intervention while en route to the G20 summit in Washington D.C.

- Risk aversion and intervention talk kept a lid on USD/JPY, allowing it to look past widening U.S./Japan yield spreads, with JGB yields anchored by confidence in the BoJ's commitment to its ultra-loose policy. PM Kishida reiterated his support for the central bank's current policy stance.

- A drop in Iron ore prices sapped strength from the Aussie dollar, which paced losses in G10 FX space for the second consecutive day. AUD/USD refreshed cycle lows, while AUD/NZD fell below the NZ$1.1300 figure.

- Spot USD/CNH advanced but the CNH7.2 mark proved resilient, with domestic COVID-19 case counts likely weighing on the redback.

- Major data releases going forward are limited to the UK labour market report. Speeches are due from Fed's Mester, ECB's Lane & Villeroy, BoE's Bailey & Cunliffe.

MNI BoK Preview - October 2022: Back To A Big Step 50bps Hike

EXECUTIVE SUMMARY

- Since the last policy meeting the biggest shift has been in terms of renewed hawkishness around the Fed outlook. BoK Governor Rhee has stated recently, external factors will be a key factor in determining Wednesday’s outcome and that the Fed outlook has been more hawkish compared to their expectations at the August policy meeting.

- Higher utility prices in Q4, in terms of electricity and gas prices, suggest it may be too early to declare victory from an inflation standpoint. The BoK also stated following the recent inflation data that it expects inflation to stay in a 5-6% range for a considerable period of time. Moreover, core pressures are not showing signs of rolling over.

- Concerns around the external growth backdrop is one factor that may drive a slower rate hike pace. Domestic conditions are holding up better (cyclical low in the unemployment rate at 2.5% etc) or at least aren’t a high enough concern yet to outweigh inflation. On this basis, while the growth outlook can’t be discounted, it’s unlikely to prevent a 50bps move at tomorrow’s meeting.

- Click to view the full preview:BoK Preview - October 2022.pdf

ASIA FX: USD Remains In Control

The USD is firmer across the board in the Asian FX space. Some markets returning from holidays has driven catch up plays. Weaker equity sentiment, a firmer USD against higher beta majors and uptick in US yields has weighed throughout the session. The main focus tomorrow is the BoK decision, where a 50bps hike is likely to be delivered.

- USD/CNH was fairly range bound until the onshore spot open. The fixing error was -300pips, larger than yesterday but still well down on late September levels. Onshore USD/CNY spot surged in early trade and USD/CNH followed suit. Higher domestic covid case numbers are likely weighing. USD/CNH touched a high of 7.1955. Focus will be on intervention risks if we breach 7.2000.

- Spot USD/KRW is +1.5% to 1435, as onshore markets play catch up after yesterday's holiday. Onshore equities are weaker (Kospi -2.40%), while earlier data (first 10 days of trade for October) continued to suggest an export slowdown).

- USD/TWD onshore is back close to 31.90 (last 31.87), which is right on recent cyclical highs for the pair. Taiwan equities are off by over 3.5%, led by weakness in tech names (TSMC down by nearly 7%).

- Spot USD/IDR extended gains after ripping through resistance from Oct 4 high, as equity outflows continued on Monday, the commodity complex softened, while Indonesia's 5-Year CDS premium moved closer to cyclical wides.

- USD/MYR lodged its best levels since the 1998 Asian financial crisis as onshore markets re-opened after a public holiday. Palm oil futures snapped a seven-day winning streak, while high-frequency data showed a decline in shipments from Malaysia in the first 10 days of the month. Participants digested the dissolution of parliament, which terminates parliamentary debate on Budget 2023.

- Onshore PHP was the strongest performer in emerging Asia as firm resistance from the PHP59 record high limited gains in USD/PHP, days after the BSP admitted being "very active" in the FX market. The peso was steady even as the Philippines' trade deficit widened to a record, exceeding expectations.

- Spot USD/THB advanced after net equity outflows from Thailand accelerated, while the NESDC warned against domestic consequences of the global economic slowdown which may turn into a recession next year.

EQUITIES: Tech Sensitive Markets Lead Declines

Asia Pac equities remain under pressure for the most part. Some smaller markets are outperforming, while Australian equities are close to flat. However, the bigger centers are seeing larger losses, part of this reflects catch up from closed markets yesterday.

- US futures are down close to -0.50%. Focus will be on whether we test below 3600 again for the SPX. Note lows at the start of the month were close to 3570. Overnight comments from Fed Vice Chair Brainard that the Fed needs to be cautious in terms of the outlook, have provided no lasting positive sentiment.

- China markets are also weaker, but mainland bourses are defying broader sell-off pressures. The Shanghai Composite down -0.35% so far in the session. The property sub-index is unwinding all of yesterday's gains, down 1.73%.

- Hong Kong shares are lower as well, the HSI down 1.5%, with tech again driving weakness.

- The Nikkei 225 is off by over 2.6%, the Taiex 4.10%, and Kospi 2.45%. Tech names like TSMC and Smasung have seen sharp losses, no doubt reflecting some catch up from yesterday's holiday.

- Chip/PC demand concerns from US markets late last week continue to weigh on the sector.

OIL: Demand Concerns Cap Rebound

Oil is slightly below NY closing levels at present. Brent was last around $96/bbl, around -0.2% for the session so far, while WTI is back under $91/bbl, off by slightly more. This follows losses of more than 1.6% through yesterday's session.

- For Brent dips towards $95.50/bbl were supported yesterday, so this level could be watched on the downside. Beyond that, note the 50-day MA comes in just under $94/bbl.

- Oil could consolidate further after last week's very strong rally (+11.3% for Brent), with the OPEC+ supply meeting now out of the way.

- Concerns this week likely rest on the demand outlook, amid global recession fears. Also, the trend move higher in Covid case numbers in China can also impact sentiment.

- Note we don't get the API inventory report tonight in the US, as this has been delayed by a day due to the Columbus day holiday at the start of this week.

- Tomorrow will deliver OPEC's monthly oil report, along with the EIA short term energy outlook, and the weekly API inventory data.

GOLD: Could See More Downside On Higher USD Levels

The backdrop for gold still looks to be a bearish one. The precious metal has dropped over 2.5% in the past 2 sessions, as the USD and yields continue to recovery. We are relatively steady so far today in trading. Gold was last just above $1666, only slightly down on NY closing levels.

- Given the DXY is back above 113.00, a simple visual relationship suggests that gold should be testing sub $1650.

- Added to this is the generally hawkish core yield backdrop. The 10yr US real yield is back to 1.62%, only slightly down on cyclical highs.

- The weaker equity market back drop is likely helping at the margin, although the dollar and real yield move tend to be more important drivers over a multi-day/week horizon.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 11/10/2022 | 0600/0700 | *** |  | UK | Labour Market Survey |

| 11/10/2022 | 0800/1000 | * |  | IT | Industrial Production |

| 11/10/2022 | 0900/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 11/10/2022 | 1000/0600 | ** |  | US | NFIB Small Business Optimism Index |

| 11/10/2022 | - |  | EU | ECB Panetta IMF/World Bank Annual Meetings | |

| 11/10/2022 | 1245/1445 | | EU | ECB Lane Keynote Speech | |

| 11/10/2022 | 1400/1000 | ** | | US | IBD/TIPP Optimism Index |

| 11/10/2022 | 1530/1130 | | US | Philadelphia Fed's Patrick Harker | |

| 11/10/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 11/10/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 11/10/2022 | 1600/1200 | | US | Cleveland Fed's Loretta Mester | |

| 11/10/2022 | 1700/1300 | *** | | US | US Note 03 Year Treasury Auction Result |

| 11/10/2022 | 1800/1900 | | UK | BOE Cunliffe Panels IIF Annual Meeting | |

| 11/10/2022 | 1800/2000 | | EU | ECB Lane NY Fed Fireside Chat | |

| 11/10/2022 | 1835/1935 | | UK | BOE Bailey in Conversation w. Tim Adams at IIF Meeting |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.