Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- FOMC: TIGHTER FINANCIAL CONDITIONS MAY LESSON NEED FOR MORE TIGHTENING - MNI

- SCHNABEL: DISINFLATION PROCESS LIKELY TO SLOW - BBG

- ISRAEL/HAMAS AGREE HOSTAGE DEAL - BBG

- HUNT AIMS TO BOOST BUSINESS INVESTMENT - BBG

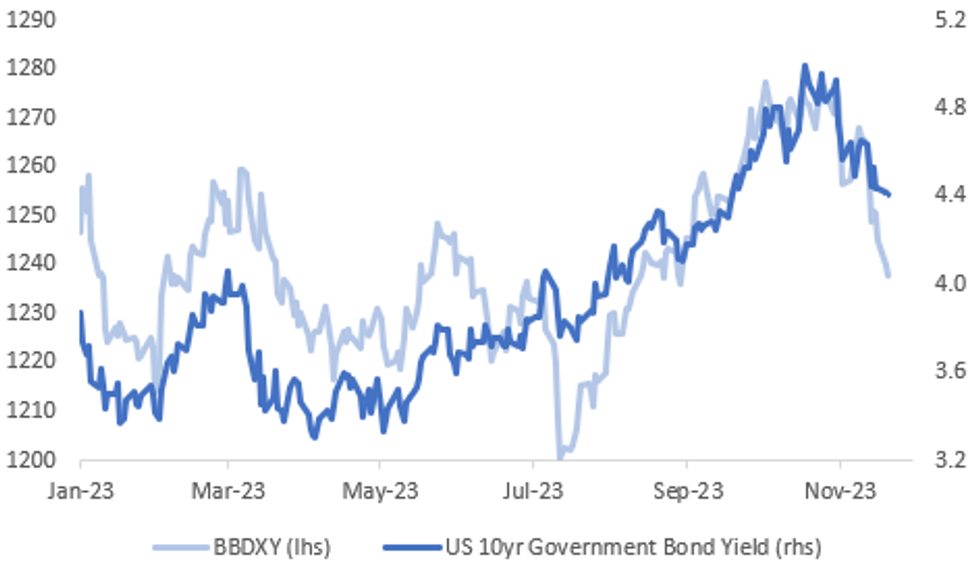

Fig. 1: BBDXY vs US 10YR Govt Bond Yield

Source: MNI - Market News/Bloomberg

U.K.

GOVT INVESTMENT (BBG): UK Chancellor of the Exchequer Jeremy Hunt aims to boost business investment by £20 billion ($25 billion) a year by unleashing a package of measures on Wednesday including making permanent a 100% tax relief on investment spending by British businesses.

EUROPE

ECB (BBG): The disinflation process recently seen in the euro area is likely to slow, according to European Central Bank Executive Board member Isabel Schnabel. “We expect overall inflation to see a temporary uptick,” she told students Tuesday at University of Wuerzburg, Germany. “We’ll need two years to get inflation from 2.9% to 2%.” (BBG)

HOLLAND (BBG): Dutch far-right populist Geert Wilders jumped to first place in the latest survey ahead of elections on Wednesday, setting the stage for him to enter government.

ETS (BBG): Ships sailing to European ports face a combined carbon emissions bill of $3.6 billion next year, the start of a levy that’s almost certainly going to rise as the continent steps up efforts to combat climate change.

U.S.

FOMC (MNI): Federal Reserve officials believed tighter financial conditions could lessen the need for additional monetary tightening as they decided to hold interest rates steady for the second straight meeting earlier this month, according to minutes of the central bank's November meeting.

NVIDIA (BBG): Nvidia Corp. investors gave a cool reaction to its latest quarterly report, which blew past average analysts’ estimates but failed to satisfy the loftier expectations of shareholders who have bet heavily on an artificial intelligence boom.

MIDDLE EAST (BBG): The US military fired at Iran-backed militants from an AC-130 gunship after they launched a close-range ballistic missile against American forces stationed at al-Asad Airbase in western Iraq, according to the Pentagon.

OTHER

JAPAN (MNI): Japan’s government lowered its main economic assessment from the previous month in November, the first downward revision since January 2023 and also decreased its assessment on capital investment for the first time in 23 months, the Cabinet Office said on Wednesday.

CANADA (MNI): Canada’s update budget Tuesday continues to book spending growth making it difficult for the central bank to cut interest rates, former senior government advisor Robert Asselin told MNI.

CANADA (MNI): Canadian Finance Minister Chrystia Freeland modestly boosted deficits over the next five years though near-term program spending runs much faster than the central bank says lines up with price stability.

ISRAEL/HAMAS (BBG): Israel’s cabinet has approved a deal with Hamas that will free at least 50 hostages in return for a four-day pause in fighting, the prime minister’s office said.

CRYPTO (BBG): Binance Holdings Ltd. and its Chief Executive Officer Changpeng Zhao pleaded guilty to anti-money laundering and US sanctions violations under a sweeping settlement with the US that allows the cryptocurrency exchange to continue operating.

OIL (BBG): Oil steadied, with signs of another stockpile build in the US coming ahead of an OPEC+ meeting on supply over the weekend.

CHINA

GROWTH (RTRS): Reuters spoke to the seven advisers who will be providing advice at December’s annual Central Economic Work Conference. Apparently, five will suggest at 5% growth target, with one at 4.5% and another 5-5.5%. But they believe that more fiscal stimulus will be needed to achieve these targets, as this year was supported by positive pandemic-related base effects. The target may be agreed in December but is unlikely to be announced until March.

YUAN (YICAI): The market should brace for further yuan appreciation, with more short squeezes expected especially over the typical November to January settlement period, Yicai.com reported citing analysts. The yuan is likely to fluctuate within the range of 7.15 to 7.17 against the U.S. dollar in the next few days, said Zhou Hao, chief economist at Guotai Junan Securities. Short squeezes driven by the improvement in China-U.S. relations and expectation of the end of rate hike is driving the recent yuan rebound, though the sustainability is unclear. The yuan has appreciated by nearly 2,000 points in two weeks.

REAL ESTATE (SEC DAILY): Sunac China has become the first large-scale real-estate company to complete domestic and overseas debt restructuring, and secure CNY3.48 billion in cooperative financing from the government-backed asset manager Huarong, the Securities Daily reported. The company has resolved CNY90 billion in debt, and reduced it by USD4.5 billion. It will have no debt repayment pressure in the overseas public market within two-three years, while the company still needs to stabilise operating cash flow and use unrestricted funds to ensure the delivery of housing projects to avoid further deterioration of brand credit, said Yan Yuejin, director at the E-house China Research and Development Institution.

CAR EXPORT (YICAI): China exported 4.24 million automobiles from January to October this year, up 58% y/y with the average export price rising to USD20,000 from USD18,000 in 2022, according to Cui Dongshu, secretary-general at the Passenger Car Association. Cui expects car exports to remain strong in Q4 reflecting the competitiveness of China's automobile industry. Chinese manufacturers have also benefited from increased demand from Russia following the Russia-Ukraine crisis. Cui also noted that the car export market has recovered stronger than the domestic market this year.

CHINA MARKETS

PBOC Drains Net CNY35 Bln Weds; Rates Unchanged

The People's Bank of China (PBOC) conducted CNY460 billion via 7-day reverse repo on Wednesday, with the rate unchanged at 1.80%. The operation has led to a net drain of CNY35 billion after offsetting the maturity of CNY495 billion reverse repos today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.9900% at 10:39 am local time from the close of 2.0213% on Tuesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 55 on Tuesday, compared with the close of 48 on Monday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

PBOC Yuan Parity Lower At 7.1254 Wednesday vs 7.1406 Tuesday

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1254 on Wednesday, compared with 7.1406 set on Tuesday. The fixing was estimated at 7.1432 by Bloomberg survey today.

MARKET DATA

AUSTRALIA OCT WESTPAC -0.03% M/M; PRIOR 0.06%

MARKETS

US TSYS: Marginally Pressured In Asia, Narrow Ranges Observed

TYZ3 deals at 108-28+, -0-01+, a 0-06+ range has been observed on volume of ~91k.

- Cash tsys sit 1-2bps cheaper across the major benchmarks, light bear steepening is apparent.

- Tsys have ticked lower through the Asian session in a narrow range in Asia. Losses marginally extended as details of an Israel/Hamas hostage deal crossed however the move has not yet follow through.

- The proximity to tomorrow's US holiday is perhaps keeping participants on the sidelines today. Cross asset flows are muted; BBDXY is unchanged, WTI is a touch below opening levels and e-minis are flat.

- There is a thin docket in Europe today, further out we have Initial Jobless Claims and the UofMich Consumer Sentiment Survey.

JGBs: Bear-Steepening Of JGB Curve Extends After BOJ Rinban Operations, Holiday Tomorrow

In the Tokyo afternoon session, JGB futures are weaker at 146.04, -26 compared to settlement levels, after reaching a new session low of 145.95 in early afternoon dealings. With the domestic data calendar light today, the catalyst for afternoon weakness appeared to be the results of this morning’s BOJ Rinban operations. The operations showed positive spreads and higher cover ratios (1-3-year: 2.57x, 3-5-year: 3.00x, 5-10-year: 1.86x and 25-year+: 2.39x).

- Reuters poll: 85% of economists say BOJ will end negative interest rates in 2024, up from 63% in the October poll.

- Weakness in cash US tsys, 2-3bps cheaper across benchmarks, in today’s Asia-Pac session also weighed on JGBs. That said, US tsy dealings have been relatively subdued as the market approaches the Thanksgiving holiday.

- The cash JGB curve has bear-steepened. The benchmark 10-year yield is 2.2bp higher at 0.725% versus the cycle high of 0.97% set in late October and the BOJ's 1% YCC reference rate. The 20-year yield is 4.8bps higher at 1.454%, fully reversing yesterday's post-20Y auction rally.

- The swaps curve has bear-steepened too, with rates 0.4bp to 5.9bps higher. Swap spreads are wider.

- A reminder that the local market is closed tomorrow for the Labour Thanksgiving holiday. National CPI is due for release on Friday.

ACGBs: Subdued Trading, RBA Gov Bullock Speech Later Today

ACGBs (YM +2.0 & XM flat) are slightly richer after dealing with relatively narrow ranges in the Sydney session. Given the light domestic calendar and the fact that US tsys are in a pre-Thanksgiving mode, the overall trading activity has been subdued.

- Cash US tsys are 1-3bps cheaper in the Asia-Pac session after yesterday’s modest gains. The release of the FOMC minutes yesterday provided no new information, with the report reaffirming the higher-for-longer stance. There was little market reaction. The US calendar later today sees Initial Jobless Claims and the UofMich Consumer Sentiment Survey.

- The latest round of ACGB Dec-34 supply showed mixed demand metrics. It printed 1.0bp through prevailing mids but the cover ratio moved lower and the number of overall and successful bidders dropped substantially.

- Cash ACGBs are flat to 2bps richer, with the AU-US 10-year yield differential 3bps lower at +3bps.

- Swap rates are flat to 2bps lower, with the 3s10s curve steeper.

- The bills strip is little changed, with pricing -1 to +1.

- RBA-dated OIS pricing is +/- 1bp softer across meetings.

- RBA Governor Bullock will deliver a speech at the ABE dinner at 1935 AEDT today.

- Tomorrow, the local calendar sees Judo Bank PMIs (preliminary) for November.

NZGBS: Slightly Cheaper, Subdued Dealings, Thanksgiving Holiday On Radar

NZGBs concluded the session on a slightly less favourable note, trading 2-3bps cheaper across benchmarks. The overall session remained relatively subdued, marked by an empty local calendar and US tsys adopting a pre-Thanksgiving holiday mode.

- In today's Asia-Pacific session, cash US tsys are 1-2bps cheaper, retracing modest gains from the previous day. The FOMC minutes released yesterday did not provide any groundbreaking information, reiterating the higher-for-longer stance. This resulted in minimal market reaction. Looking ahead, the US calendar for later today includes Initial Jobless Claims and the UofMich Consumer Sentiment Survey.

- Swap rates closed 1-2bps higher, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed little changed across meetings. Terminal OCR expectations remained at 5.54%.

- Tomorrow, the local calendar is once again empty, ahead of Q3 Retail Sales Ex-Inflation on Friday.

- Tomorrow, the NZ Treasury plans to sell NZ$225mn of the 3.0% Apr-29 bond, NZ$225mn of the 3.5% Apr-33 bond and NZ$50mn of the 2.75% Apr-37 bond.

OIL: Crude Little Changed As Wait For US Stock Data

Oil prices are off their early session highs following confirmation of an Israeli/Hamas temporary ceasefire deal. Crude has been trading in a narrow range ahead of the US holiday but is moderately lower today. WTI is down 0.1% to $77.70/bbl after approaching $78 earlier. Brent is -0.1% at $82.35, off the intraday low of $82.12. The USD index is flat.

- OPEC+ meets this weekend and while an extension of the Saudi and Russian voluntary cuts into 2024 is expected, there is some speculation whether the rest of the bloc will reduce output further because of current softer prices and increased non-OPEC supply. Citibank has estimated a 20% probability this occurs and Goldman Sachs 35%, according to Bloomberg.

- The focus for crude today is likely to be the official EIA US inventory data. Bloomberg reported that there was a 9.05mn barrel crude stock build, according to people familiar with the API data, but gasoline inventories fell 1.8mn and distillate -3.5mn. EIA reported refinery rates will also be of interest.

- Later US jobless claims, October preliminary durable goods orders and final November Michigan consumer sentiment are released.

GOLD: Steady After Strong Gains On Tuesday

Gold is little changed in the Asia-Pac session, after closing +1.0% at $1998.29 on Tuesday, pulling back off highs of $2007.61 with some intraday strengthening in the USD index.

- This was the first time bullion had cleared $2,000/oz in spot trade since late October.

- The precious metal is up around 3% since the beginning of last week, buoyed by falling Treasury yields and a sharp drop in the dollar.

- Technically, well-defined parameters remain in play and bulls remain in control at present, according to MNI’s technical team.

- A stronger resumption of gains would open $2,022.20/oz (the May 15 high). The bull trigger at $2,009.4/oz (the Oct 27 high) provides initial resistance ahead of there.

EQUITIES: APEC Markets Mixed & Range Trading Ahead Of US Thanksgiving

Equity markets have been mixed during the APAC session following US weakness on Tuesday. The MSCI APEX 50 is down 0.3% with China/HK falling but Japan rallying. The Nasdaq e-mini is down 0.1% but S&P is flat ahead of the US holiday on Thursday.

- While HK’s Hang Seng is down only 0.1%, China’s CSI is 0.5% lower but the property component is slightly higher.

- Japan’s Nikkei is 0.3% higher, Korea’s KOSPI up only 0.1% but Taiwan’s TAIEX is down 0.7%, due to semiconductor manufacturer TSMC falling 1.7%. Tech stocks have been weaker after the Nasdaq’s Nvidia fell in after-hours trading despite better profits.

- Australia/NZ are little changed with the ASX down 0.1%. The NZX 50 is up slightly.

- ASEAN is mixed with Indonesia’s Jakarta Comp falling 0.6%, SE Thai -0.8%, Malay KLCI -0.6% but Singapore’s Straits Times is up 0.4% and Philippines PSEi +0.2%.

- India’s Nifty 50 is marginally higher.

FOREX: Narrow Ranges Across G-10 In Asia

There has been narrow ranges across G-10 FX in muted pre-US holiday trade in Asia today. The cross asset space remains muted; US Tsy Yields are marginally higher and e-minis are unchanged. Details of an Israel/Hamas hostage deal crossed however there was little reaction in FX.

- USD/JPY is ~0.1% lower and sits a touch above the ¥148 handle. Technically there is a short term bearish trend for USD/JPY. Support comes in at ¥147.15, Nov 21 low, and ¥146.00, trendline support drawn from Mar 24 low. Resistance is at ¥149.16, 50-Day EMA.

- Kiwi is a touch softer, however a narrow $0.6040/60 range has been observed in Asia.

- AUD/USD is little changed from opening levels. Westpac Leading Index for October printed at -0.03%. Technically the latest rally has resulted in a clear break of former resistance at $0.6522, the Aug 30 and Sep 1 high. Resistance now comes in at $0.6616, High Oct 8. Support is at $0.6453, Low Nov 17.

- There is a thin docket in Europe on Wednesday with no data releases of note, the highlight is the UK Autumn Statement from Chancellor Hunt.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 22/11/2023 | 1100/1100 | ** |  | UK | CBI Industrial Trends |

| 22/11/2023 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 22/11/2023 | 1230/1230 | | UK | UK Autumn Statement | |

| 22/11/2023 | 1330/0830 | ** | | US | Durable Goods New Orders |

| 22/11/2023 | 1330/0830 | *** | | US | Jobless Claims |

| 22/11/2023 | 1410/1510 |  | EU | ECB's Elderson keynote speech on stability in the Green Transition | |

| 22/11/2023 | 1500/1600 | ** | | EU | Consumer Confidence Indicator (p) |

| 22/11/2023 | 1500/1000 | ** | | US | U. Mich. Survey of Consumers |

| 22/11/2023 | 1530/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 22/11/2023 | 1530/1530 | | UK | DMO publish agenda for quarterly meetings | |

| 22/11/2023 | 1630/1130 |  | CA | BOC Governor Tiff Macklem speech/press conference | |

| 22/11/2023 | 1700/1200 | ** | | US | Natural Gas Stocks |

| 23/11/2023 | 2200/0900 | *** |  | AU | Judo Bank Flash Australia PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.