Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- FED HAS TIME TO SEE IF ‘MORE WORK’ NEEDED - BARKIN - MNI BRIEF

- JAPAN SEPT TOKYO CORE CPI 2.5% VS. AUG 2.8% - MNI BRIEF

- RBA TO LOOK AT UNDERUTILISATION IN NAIRU REVAMP - MNI

- CHINA OFFICIALS MULL DC TRIP TO PREP POSSIBLE XI-BIDEN MEET - WSJ

- CHINA LOOKS TO RELAX CROSS-BORDER DATA SECURITY -FT

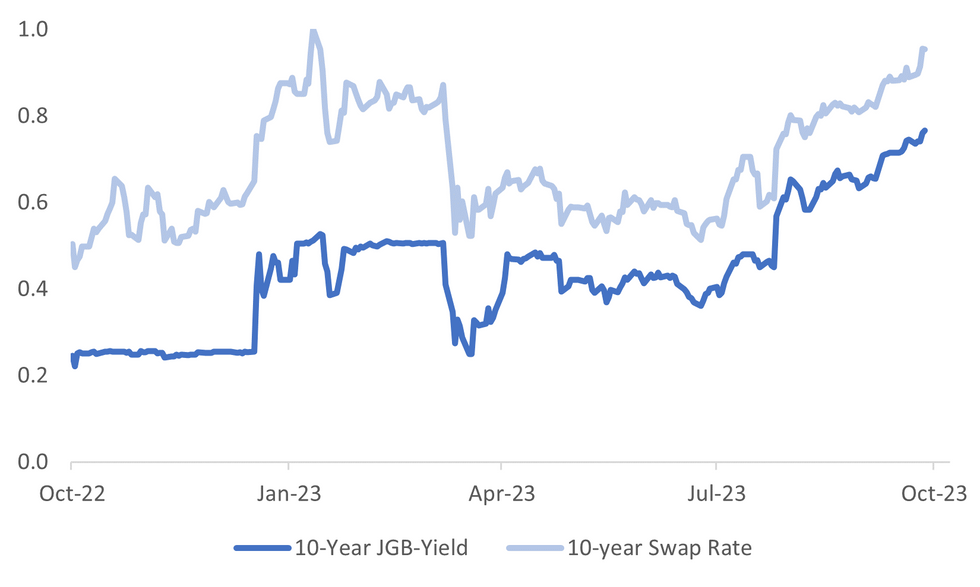

Fig. 1: Japan 10yr Government Bond Yield & 10-yr Swap Rate

Source: MNI - Market News/Bloomberg

U.K:

ENERGY: The number of customers falling into debt on their energy bills has increased by 36% since the beginning of this year, according to EDF Energy. The company plans to roll back standing charges — fixed costs added on top of bills to cover being connected to the grid — for vulnerable customers this winter to help reduce the strain. Daily charges for direct debit customers have increased by 107% for electricity and 8.2% for gas since April 2021, EDF said. (BBG)

EUROPE:

ECB: European Central Bank interest rates will probably remain steady for an extended period, according to Governing Council member Martins Kazaks. “Most likely, rates will be around where they are at the moment and also remain there for some time,” Kazaks told Latvia’s LTV on Friday. “Of course, that’s dependent on the economy — if inflation doesn’t go down, then there could be a small increase.” (BBG)

UKRAINE: NATO Secretary General Jens Stoltenberg, on an unannounced visit to Kyiv, said on Thursday that Ukrainian forces were "gradually gaining ground" in their counteroffensive against Russian forces. Speaking at a joint press conference with Ukrainian President Volodymyr Zelenskiy, Stoltenberg said "every metre that Ukrainian forces regain is a metre that Russia loses". (RTRS)

EU/CHINA: German Chancellor Olaf Scholz voiced skepticism over the EU's probe into potentially illegal subsidies for Chinese electric vehicles, saying Europe should not be protectionist and rather, should welcome global competition. "The economic model which I favor is to have global competition," Scholz said during a panel debate at the Berlin Global Dialogue on Thursday, warning against a "protectionist way." (POLITICO)

ITALY: European government bond prices dropped sharply on Thursday as investors took fright at Italy’s larger than expected budget deficit and mounting concerns that central banks will keep interest rates high for an extended period. Italian 10-year government bond yields rose as much as 0.17 percentage points to 4.96 per cent, their highest level in a decade, after Prime Minister Giorgia Meloni’s government raised its fiscal deficit targets and cut its growth forecast for this year and next. The yield later fell back to 4.88 per cent. (FT)

U.S.

FED: Federal Reserve Bank of Richmond President Tom Barkin said Thursday he supported an interest rate pause at last week's FOMC meeting and will be watching the labor market for clues of better balance and moderating wages before deciding whether there is a need for further monetary tightening. (MNI BRIEF)

OIL: The Biden administration is charting plans to sell offshore oil-drilling rights in the Gulf of Mexico over the next five years, while trimming the program to its smallest level ever. The oil leasing plan being released by the Interior Department on Friday will contain only a low number of sales, according to people familiar with the deliberations who declined to be named because the blueprint isn’t yet public. That’s far from the 11 sales the agency proposed last year, and it would be the lowest in history. (BBG)

FISCAL: The Democratic-led U.S. Senate forged ahead on Thursday with a bipartisan stopgap funding bill aimed at averting a fourth partial government shutdown in a decade, while the House prepared to vote on partisan Republican spending bills with no chance of becoming law. The divergent paths of the two chambers appeared to increase the odds that federal agencies will run out of money on Sunday, furloughing hundreds of thousands of federal workers and halting a wide range of services from economic data releases to nutrition benefits. (RTRS)

OTHER

JAPAN: The y/y rise in the Tokyo core inflation rate slowed to 2.5% in September from August's 2.8% driven by lower energy prices, indicating the nationwide September core CPI will fall from August's 3.1%, data from the Ministry of Internal Affairs and Communications showed on Friday. (MNI BRIEF)

JAPAN: Japan's industrial production was unchanged m/m in August following a 1.8% drop in July as higher production for electrical machinery and information, and communication electronics equipment offset the drop in automobile production, Ministry of Trade and Industry data showed Friday. (MNI BRIEF)

JAPAN: TOKYO--Japan's Finance Minister Shunichi Suzuki renewed his pledge to take action against sharp falls in the yen as it weakened to its lowest level in almost a year. "There is no change to our stance that we will take appropriate action against excessive moves without ruling out any options," Suzuki said at a news conference on Friday. "We have a strong sense of urgency." (DJ)

SOUTH KOREA: FTSE Russell said South Korea will continue to remain on the watch list for inclusion to its global bond index — and India for the emerging-market equivalent — extending the countries’ wait to be added to the key indexes by at least another six months. (BBG)

AUSTRALIA: The Reserve Bank of Australia will consider incorporating underutilisation data into its labour force models, such as its estimate of the non-accelerating inflation rate of unemployment (NAIRU), following the publication of an employment white paper by the Treasury this week, according to academics and former staffers. (MNI BRIEF)

CHINA

CHINA/US: China’s Vice Premier He Lifeng and Foreign Minister Wang Yi are discussing possible visits to Washington DC to prepare for a potential summit between Xi Jinping and Joe Biden, the Wall Street Journal reports, citing unidentified people briefed on the matter. (WSJ)

HOUSING: Shenzhen will relax the floor for mortgage rates on first-home purchases, the first of China’s four-biggest cities to make such a move, as officials nationwide grapple with a years-long real estate crisis that’s dragging on economic growth and rippling through financial markets. (BBG)

TECH: China has moved to water down some of its tough cross-border data controls amid complaints from foreign businesses and a teetering economy. The Cyberspace Administration of China unveiled rules on Thursday evening which look to clarify and simplify the transfer of data out of the country for ordinary business activities. Beijing’s move to walk back part of its burdensome regime comes amid efforts to reassure foreign businesses concerned about deteriorating US-China relations and the creeping influence of its own security apparatus. (FT)

ECONOMY: China’s economy showed signs of a stronger recovery in September, according to a firm analyzing the global economy using satellite data. Activity around Chinese shopping malls remained at relatively high levels in September following an increase in August, according to SpaceKnow, a US company that analyzes satellite images. A pickup in cement manufacturing, which began in June, was also sustained through this month, the data show. (BBG)

ECONOMY: President Xi Jinping says China will step up efforts to achieve the annual economic and social development targets, China Central Television reports, citing his speech at a reception Thursday in Beijing to celebrate the 74th anniversary of the Communist government. (CCT)

MARKET DATA

NZ SEP ANZ CONSUMER CONFIDENCE INDEX 86.4; PRIOR 85.0

JAPAN SEP TOKYO CPI Y/Y 2.8%; MEDIAN 2.7%; PRIOR 2.9%

JAPAN SEP TOKYO EX-FRESH FOOD CPI Y/Y 2.5%; MEDIAN 2.6%; PRIOR 2.8%

JAPAN SEP TOKYO CPI EX-FRESH FOOD, ENERGY Y/Y 3.8%; MEDIAN 3.9%; PRIOR 4.0%

JAPAN AUG JOBLESS RATE 2.7%; MEDIAN 2.6%; PRIOR 2.7%

JAPAN AUG JOB-TO-APPLICANT RATIO 1.29; MEDIAN 1.29; PRIOR 1.29

JAPAN RETAIL SALES Y/Y 7.0%; MEDIAN 6.6%; PRIOR 7.0%

JAPAN RETAIL SALES M/M 0.1%; MEDIAN 0.4%; PRIOR 2.2%

JAPAN AUG IP M/M 0.0%; MEDIAN -0.8%; PRIOR -1.8%

JAPAN AUG IP Y/Y -3.8%; MEDIAN -4.6%; PRIOR -2.3%

JAPAN AUG HOUSING STARTS Y/Y -9.4%; MEDIAN -8.7%; PRIOR -6.7%

JAPAN SEP CONSUMER CONFIDENCE INDEX 35.2; MEDIAN 36.2; PRIOR 36.2

MARKETS

US TSYS: Marginally Cheaper In Asia

TYZ3 deals at 107-26+, -0-01, a 0-05 range has been observed on volume of ~68k.

- Cash tsys sit ~2bps cheaper across the major benchmarks.

- Tsys have ticked lower, albeit in narrow ranges, through today's Asian session with participants perhaps using Thursday's richening as an opportunity to enter fresh short positions.

- There was little reaction to Feds Barkin who noted that policymakers have time to determine if they need to do more work to cool inflation and that the labour market may offer some insight.

- On the docket today we have US consumer spending, wholesale inventories and University of Michigan consumer sentiment.

JGBS: Unscheduled BOJ Bond Purchase Sees Futures Spike Higher But It Quickly Reverses

JGB futures are sitting just above session lows, -12 compared to settlement levels, despite the BOJ’s unscheduled bond purchase of Y300bn 5- to 10-year JGBS at market prices.

- In addition to the earlier releases of Tokyo CPI, industrial production and retail sales, the local docket has just printed Housing Starts and Consumer Confidence data. Housing starts print -9.4% y/y vs. -8.7% est., while confidence prints 35.2 vs. 36.2 est.

- The cash JGB curve has bear-steepened, with yields 0.6bp to 1.9bps higher. The benchmark 10-year yield is 0.4bp higher at 0.765%, above BOJ's YCC soft limit of 0.50% but below its hard limit of 1.0%. It is also below the cycle high of 0.774% set today, before the BOJ bond purchase.

- Bloomberg reports that investors need to prepare for Japan’s benchmark 10-year bond yield rising to around 2% if the central bank’s inflation goal is realized and it ends its negative-rate policy, according to a former research chief at the Bank of Japan. (See link)

- Swap rates are slightly mixed across the curve. Swap spreads are tighter across maturities.

- Monday the local calendar sees BOJ Summary of Opinions (Sept. MPM), Tankan Mfg & Non-Mfg Indices and Jibun Bank Mfg PMI.

AUSSIE BONDS: Cheaper, Mid-Range, RBA Policy Decision Next Tuesday

ACGBs (YM flat & XM -4.5) are weaker, mid-range, after a relatively light domestic data docket. As previously outlined, private sector credit for August printed slightly better than expected (+0.4% m/m vs. +0.3% est. and +0.3% prior).

- Accordingly, domestic participants have likely been on headlines and US tsys/JGBs watch in Asia-Pac trade.

- US tsys have been pressured and are around session lows, 2-3bps cheaper across the major benchmarks.

- 10-year and longer-dated JGBs have pushed to their highest levels in the current cycle. The 10-year yield reached a post-YCC tweak peak of 0.774%. In response to this development, the BOJ conducted an unscheduled bond purchase of Y300bn in 5-to-10-year notes at market yields. The announcement caused JGB futures to initially spike higher, but these gains were swiftly reversed.

- The cash ACGB curve has twist-steepened, with yields 1bp lower to 4bps higher. The AU-US 10-year yield differential is 5bps higher at -9bps.

- The swaps curve has also twist-steepened, with rates -1bp to 4bps higher.

- The bills strip is slightly richer, with pricing +1 to +2.

- RBA-dated OIS pricing is slightly firmer across meetings. The market currently attaches a 13% chance of a 25bp hike for next week.

- Next week the local calendar sees a raft of second-tier data ahead of the RBA decision on Tuesday.

NZGBS: Closed On Cheaps, ~20% Chance Of A RBNZ Hike Next Wednesday

NZGBs closed at or near session cheaps, with benchmark yields 4-6bps higher. The local data docket was relatively light, with ANZ Consumer Confidence’s push to its highest reading since January 2022 as the highlight. Accordingly, domestic participants are likely to have been guided by spillover selling from US tsys and JGBs in Asia-Pac trade.

- US tsys have been pressured and sit at session lows, 2-3bps cheaper across the major benchmarks.

- 10-year and longer-dated JGBs have pushed to their highest levels in the current cycle. The 10-year yield reached a post-YCC tweak peak of 0.774%. In response to this development, the BOJ conducted an unscheduled bond purchase of Y300bn in 5-to-10-year notes at market yields. The announcement caused JGB futures to initially spike higher, but these gains were swiftly reversed.

- Swap rates are 4-9bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing is little changed across meetings, with terminal OCR expectations at 5.77% (+27bps). The market currently attaches a 19% chance of a 25bp hike next week.

- Monday the local calendar sees the release of Building Permits for August, ahead of CoreLogic House Price Data and the RBNZ Policy Decision on Wednesday. Bloomberg consensus expects the OCR to be left unchanged at 5.50%.

FOREX: Antipodeans Firm in Asia

The Antipodeans have firmed in Asia extending Thursdays gains as firmer regional equities, the Hang Seng is up ~2%, boost sentiment.

- Kiwi is the strongest performer in the G-10 space at the margins. NZD/USD has broken the $0.60 handle in recent dealing and is now up ~0.7%. ANZ Consumer Confidence rose to its highest level since January 2022.

- AUD/USD is up ~0.5% and last prints at $0.6455/60. THe pair has ticked away from the 20-Day EMA ($0.6427), the next upside resistance level is at $0.6522 high from Sep 1. Support comes in at $0.6331 low from Sep 27.

- The Yen is little changed from opening levels and ranges have been relatively narrow. USD/JPY last prints at ¥149.35/40. The trend continues to be bullish, resistance comes in at ¥149.71, high from Oct 24 2022. Support is at ¥147.67, the 20-Day EMA.

- Elsewhere in G-10, EUR and GBP are following the broader USD move and are up ~0.1%. BBDXY is ~0.1% lower.

- The final Q2 GDP read from the UK provides the highlight in Asia today.

EQUITIES: Hong Kong Equities Surge On Multiple Support Points

Regional equities have been mixed today in holiday impacted markets. China markets are closed as the Golden Week holiday period kicks off. South Korean markets also remained closed. The stand out from a positive point of view has been the surge in Hong Kong equities. The HSI is up +2.7%. Trends elsewhere are mixed. US equity futures sit slightly higher at this stage. Eminis last near 4341, +0.08%. Earlier lows were at 4327.50.

- Hong Kong markets have been buoyed by a number of factors. Further support for China's housing market, with reports that Shenzhen will relax the mortgage rate floor for first home-buyers, is one positive.

- The FT notes that China cross-border data restrictions may be eased, which has also helped. The HSTECH index is up 3.66% at the break. The WSJ also notes that momentum is gaining for a potential Xi Jinping trip to the US.

- Elsewhere, Japan stocks are mixed, with the Topix down 0.50%, but the Nikkei 225 is a touch higher. Local bond yields continue to climb despite Tokyo core CPI printing weaker than expected.

- The ASX 200 is up 0.50%, aided by material stock gains, as firmer metal prices have boosted miners.

- In SEA, trends are mixed, with Malaysian, Philippines and Thailand shares lower. Indonesian markets have returned with a positive bias.

OIL: Consolidates After Thursday Losses, Still Up Strongly For The Past Week, Month & Quarter

WTI has largely tracked sideways near NY closing levels from Thursday in the first part of Friday trade. We did pop above $92/bbl briefly, but it wasn't sustained. The benchmark last tracked near $91.80/bbl (we closed on Thursday at $91.71/bbl). This still leaves us still nearly +2% firmer for the week, +9.76% for September and nearly 30% higher for the quarter. For Brent, we track above $95/bbl, following a similar trajectory to WTI. The benchmark has posted similarly impressive gains over the past quarter.

- Thursday's pull back has largely been described as technical in nature, given overbought readings on the RSI for example.

- Still, there is some speculation that with oils sharp rise in recent months we may start to see OPEC+ ease supply constraints. Until this/if it eventuates though, Q4 is likely to be exhibited by tight supply constraints.

- For Brent, the 20-dauy EMA sits back near $92.55/bbl. Recent highs rest at $97.69/bbl.

- Note we get official PMIs for September in China tomorrow. This will provide an update on the economic backdrop, as optimism over travel related oil demand firmed ahead of the Golden Week holiday period.

GOLD: Heading For The Biggest Weekly Loss In Eight Months

Gold has remained relatively stable during the Asia-Pac session, following a decline of -0.5% to $1865.03 on Thursday. It's worth noting that despite the USD index reversing its substantial Wednesday gains and US Treasuries experiencing a rally, there was surprisingly limited relief in bullion selling.

- Gold is headed for its biggest weekly decline in eight months, with the higher-for-longer interest rate environment taking its toll on the precious metal.

- US Treasuries finished at or near session bests, with yields 2-8bps lower. The 10-year yield climbed to a new 16-year high in a volatile morning session on heavy volume. US data was mixed. Weekly Claims printed lower than expected (204k vs. 215k est), but the GDP Price Index was lower than expected (1.7% vs. 2.0% est), Personal Consumption missed (0.8% vs. 1.7% est) and Pending Home Sales were below estimates (-7.1% vs. -1.0% est).

- Exchange-traded funds backed by the metal have accelerated sales of bullion. A particularly large outflow came from Blackrock’s iShares Gold Trust, which has shed 13 tons of gold this week, according to data compiled by Bloomberg.

- From a technical standpoint, Thursday’s low of $1857.76 saw the yellow metal push through the latest support at $1865.8 (76.4% retrace of Feb 28 – May 4 bull leg), with $1839.0 (50% retrace of the same move) up next, according to MNI’s technical team.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 29/09/2023 | 0600/0800 | ** |  | SE | Retail Sales |

| 29/09/2023 | 0600/0700 | *** |  | UK | GDP Second Estimate |

| 29/09/2023 | 0600/0700 | * | | UK | Quarterly current account balance |

| 29/09/2023 | 0600/0800 | ** |  | DE | Retail Sales |

| 29/09/2023 | 0600/0800 | ** | | DE | Import/Export Prices |

| 29/09/2023 | 0645/0845 | *** |  | FR | HICP (p) |

| 29/09/2023 | 0645/0845 | ** | | FR | PPI |

| 29/09/2023 | 0645/0845 | ** | | FR | Consumer Spending |

| 29/09/2023 | 0700/0900 | * |  | CH | KOF Economic Barometer |

| 29/09/2023 | 0740/0940 |  | EU | ECB's Lagarde speaks at IEA-ECB-EIB Conference | |

| 29/09/2023 | 0755/0955 | ** | | DE | Unemployment |

| 29/09/2023 | 0830/0930 | ** | | UK | BOE M4 |

| 29/09/2023 | 0830/0930 | ** | | UK | BOE Lending to Individuals |

| 29/09/2023 | 0900/1100 | *** | | EU | HICP (p) |

| 29/09/2023 | 0900/1100 | *** |  | IT | HICP (p) |

| 29/09/2023 | - | | UK | Publication of the Treasury bill calendar for October-December 2023. | |

| 29/09/2023 | 1230/0830 | *** |  | CA | Gross Domestic Product by Industry |

| 29/09/2023 | 1230/0830 | ** |  | US | Personal Income and Consumption |

| 29/09/2023 | 1230/0830 | ** | | US | Advance Trade, Advance Business Inventories |

| 29/09/2023 | 1345/0945 | *** | | US | MNI Chicago PMI |

| 29/09/2023 | 1400/1000 | ** | | US | U. Mich. Survey of Consumers |

| 29/09/2023 | 1500/1100 | | CA | Finance Dept monthly Fiscal Monitor (expected) | |

| 29/09/2023 | 1600/1200 | ** | | US | USDA GrainStock - NASS |

| 29/09/2023 | 1645/1245 | | US | New York Fed's John Williams |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.