Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- FED’s WALLER WANTS TWO MORE INTEREST RATE HIKES THIS YEAR - MNI

- FED’s BULLARD, INFLUENTIAL VOICE ON RATES, TO LEAVE FOR ACADEMIA - BBG

- CHINA CENTRAL BANK PLEDGES TO USE POLICY TOOLS TO SPUR RECOVERY - BBG

- BoJ To TWEAK YIELD CONTROL THIS MONTH, EX-OFFICIAL HAYAKAWA SAYS - BBG

- BOJ LIKELY TO RAISE FY2023 INFLATION FORECAST ABOVE 2% - YOMIURI

- BULLOCK TO REPLACE LOWE AS NEXT RBA GOVERNOR - MNI BRIEF

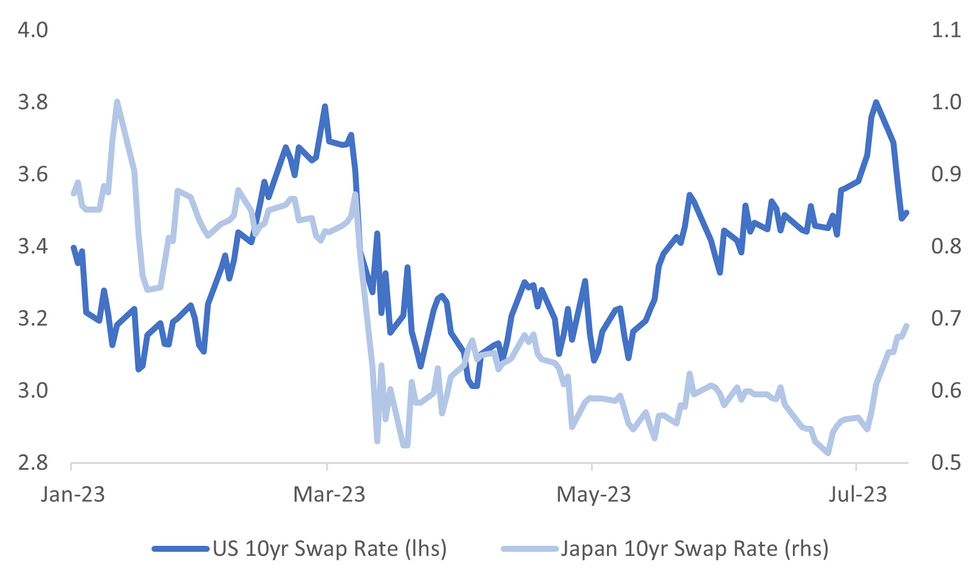

Fig. 1: Japan & US 10yr Swap Rates - Recent Trends Diverging

Source: MNI - Market News/Bloomberg

U.K.

WAGES: British Prime Minister Rishi Sunak sought on Thursday to end months of crippling public sector strikes by offering teachers, doctors and other workers pay increases of 6% and above, but warned it would cost billions that could mean cuts elsewhere. Sunak faces an election in the next 18 months against a backdrop of the highest inflation of any major economy, a near-stagnant economy and a legacy of scandals and missteps from his Conservative Party's 13 years in power. Opinion polls put the Conservatives far behind the opposition Labour Party. (RTRS)

US

FED: (MNI) WASHINGTON - The Federal Reserve should raise interest rates twice more this year to bring U.S. inflation back down to the central bank’s 2% goal, Fed Governor Chris Waller said Thursday. “I see two more 25-basis-point hikes in the target range over the four remaining meetings this year as necessary to keep inflation moving toward our target,” Waller said in prepared remarks to the Money Marketeers of New York University. “Furthermore, I believe we will need to keep policy restrictive for some time in order to have inflation settle down around our 2% target. (MNI)

FED: Federal Reserve Bank of St. Louis President James Bullard, an influential voice who called for aggressive interest-rate hikes to fight the recent inflation surge, resigned after 15 years in the position to become dean of a university business school. Bullard, 62, stepped down from his post as head of the bank effective Thursday. He will fully depart Aug. 14 to become the inaugural dean of the Mitchell E. Daniels, Jr. School of Business at Purdue University, the St. Louis Fed said in a statement Thursday. (BBG)

OTHER

JAPAN: The Bank of Japan will probably adjust its yield curve control program at its policy meeting this month given that inflation is stronger than expected, according to a former executive director at the bank. “I expect they will make some kind of adjustment to YCC this month,” former director Hideo Hayakawa said in an interview Thursday. “If they don’t, it doesn’t make sense.” (BBG)

JAPAN: The Bank of Japan is on course to raise its inflation forecast for this fiscal year ending March to more than 2% from current 1.8% when it reviews the outlook later this month, the Yomiuri newspaper reports without attribution. The central bank sees businesses increasing prices more than it expected. (Yomiuri)

JAPAN: Japan’s Finance Minister Shunichi Suzuki tells reporters that he will host a Group of Seven meeting with Bank of Japan Governor Kazuo Ueda on July 16. Will discuss Ukraine, international taxation, multilateral development banks during meeting; not expecting to issue an outcome statement. (BBG)

AUSTRALIA: (MNI) Sydney - Michele Bullock, deputy governor at the Reserve Bank of Australia, will become Australia’s next governor, replacing Philip Lowe when his term ends September. Federal Treasurer Jim Chalmers and Prime Minister Anthony Albanese revealed the decision Friday morning in Canberra. Bullock beat out two other top contenders to take the job – Department of Finance Secretary Jenny Wilkinson and Treasury Secretary Steven Kennedy. She has spent over 37 years at the RBA and was named the Reserve’s first female deputy in 2022. She will lead the RBA’s implementation of the recent review recommendations (MNI)

AUSTRALIA: Treasurer Jim Chalmers has made history by appointing the first female governor of the RBA. Bullock continues a tradition since the 1990s of the deputy succeeding the governor, after intense speculation about who would replace Lowe and whether an outsider would be appointed to shake up the bank. The elevation of the straight-talking Bullock sends a positive signal to the financial markets and the public that the Albanese government backs the RBA’s once-in-a-generation inflation fight. (AFR)

CHINA/AUSTRALIA: China's top diplomat Wang Yi said China and Australia's relations have "stabilised, improved and developed" under the joint efforts of both countries, a Chinese foreign ministry statement Friday said. Wang also said he hoped Australia will provide a fair, just and non-discriminatory business environment for Chinese enterprises to invest and operate in the country. (RTRS)

SINGAPORE: Singapore's economy narrowly escaped a recession in the second quarter as global demand weakened and China's slowdown dragged on trade flows, leading some economists to cut their growth forecasts for the year. The Southeast Asian economy grew a seasonally adjusted 0.3% quarter-on-quarter, following a 0.4% contraction in the first three months, preliminary government data showed on Friday. Four economists with quarterly estimates had forecast growth of 0.3% in a Reuters poll. (RTRS)

CHINA

POLICY: The People’s Bank of China urged patience and confidence in the economy’s recovery as it pledged to use its policy tools to support growth. China will implement targeted and forceful monetary policy and strengthen counter-cyclical adjustments, Deputy Governor Liu Guoqiang told reporters in Beijing on Friday. That was largely a repeat of the PBOC’s recent monetary stance. (BBG)

ECONOMY: Chinese President Xi Jinping finally appears to be extending an olive branch to private businesses battered in recent years by regulatory crackdowns and the world’s most restrictive Covid-19 policies. Officials have made a series of high-profile actions designed to telegraph the Chinese government’s backing for private firms, as the nation’s post-pandemic recovery risks being caught in a confidence trap. The Chinese leader has vowed to treat foreign investors better and called for greater opening up in recent weeks. (BBG)

YUAN: The People’s Bank of China will move against any one-way bet on the yuan while remaining accommodative to shore up the economy, while consumer price will likely edge up by the end of the year, Vice Governor Liu Guoqiang told reporters Friday. The Bank will respond to “correct pro-cyclical moves” in the fx market when necessary and “prevent big volatility”, Liu said when was questioned on CNY's recent depreciation. He noted the PBOC had plenty of policy tools at its disposal. (MNI BRIEF)

OFFICE VACANCIES: Office vacancy rate in Beijing reached 18% in the second quarter, the highest in 13 years, Caixin Global reported, citing data from real estate service provider Savills. The second-quarter vacancy rate of office buildings in the Chinese is up 1.5 percentage points from the previous quarter and is the highest since the first quarter of 2010. (BBG)

MARKETS: At least 30 companies listed in China’s A-share market have received regulatory warnings for large revisions made to their earnings forecasts this year, Economic Information Daily reports Friday. (BBG)

TOURISM: China posts 2.3 trillion yuan in revenue from domestic tourism in the first half of 2023, a rise of 96% year over year, according to a Xinhua report. 2.38 billion domestic tourism trips were made in 1H, up 64% over same period of last year, report cites data from the Ministry of Culture and Tourism. (BBG)

PROPERTY: The People’s Bank of China signaled more targeted support may be on the cards for the property market as it sought to assure investors that the risks banks face from the sector are controllable. Real estate policies will be “tailored” to cities, Zou Lan, head of the monetary policy department, said Friday at the PBOC’s briefing on first-half economic statistics. He added that the policies that were rolled out when the market was overheated can be “optimized marginally.” (BBG)

PROPERTY: At least two holders of a Sino-Ocean Group Holding Ltd. dollar bond have yet to receive a coupon payment that was due Thursday, heightening debt worries surrounding the Chinese state-backed developer that’s shaken the nation’s junk-note market in recent weeks. (BBG)

CHINA MARKETS

MNI: PBOC Net Injects CNY18 Bln Via OMOs Friday

The People's Bank of China (PBOC) conducted CNY20 billion via 7-day reverse repos on Friday, with the rates at 1.90%. The operation has led to a net injection of CNY18 billion after offsetting the maturity of CNY2 billion reverse repo today, according to Wind Information.

- The operation aims to keep banking system liquidity reasonable and ample, the PBOC said on its website.

- The 7-day weighted average interbank repo rate for depository institutions (DR007) rose to 1.8909% at 09:43 am local time from the close of 1.7851% on Thursday.

- The CFETS-NEX money-market sentiment index closed at 46 on Thursday, compared with the close of 48 on Wednesday.

PBOC Yuan Parity Lower At 7.1318 Friday Vs 7.1527 Thursday.

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower for the sixth trading day at 7.1318 on Friday, compared with 7.1527 set on Thursday. The fixing was estimated at 7.1425 by BBG survey today.

OVERNIGHT DATA

SOUTH KOREA MAY MONEY SUPPLY M2 SA M/M -0.3%; PRIOR -0.4%

JAPAN MAY F INDUSTRIAL PRODUCTION M/M -2.2%; PRIOR -1.6%

JAPAN MAY F INDUSTRIAL PRODUCTION Y/Y 4.2%; PRIOR 4.7%

JAPAN MAY CAPACITY UTILIZATION M/M -6.3%; PRIOR 3.0%

MARKETS

US TSYS: Marginally Pressured In Asia

TYU3 deals at 112-29+, -0-04, a 0-07+ range has been observed on volume of ~80k.

- Cash tsys sit flat to 1bp cheaper across the major benchmarks, light bear flattening is apparent.

- Tsys were pressured in early dealing as an offer in JGBs spilled over into the wider space.

- Fedspeak from Gov Waller this morning noted that he sees two more 25bp increases this year and that policy will need to remain restrictive for some time. Waller also said that September is a live meeting for rate policy.

- The move lower didn't follow through and tsys dealt in a narrow range for the remainder of the session after marginally paring losses.

- There is a thin docket in Europe today, further out we have Terms of Trade and the latest UofMich consumer sentiment. A reminder that the Fed blackout period starts at midnight EDT today.

JGBS: Futures Cheaper But Off Worst Levels Sparked By YCC Tweak Speculation

In the Tokyo afternoon session, JGB futures are weaker, -21 compared to settlement levels, but have dramatically pared the cheapening seen in the morning session. As previously flagged, early weakness centred on speculation about a possible tweak to YCC at the BoJ’s late July meeting.

- Just released, industrial production for May printed -2.2% m/m and +4.2% y/y versus -1.6% and +4.7% previously. Capacity utilisation printed -6.3% m/m versus +3.0% in April.

- Japan’s Government Pension Investment Fund boosted its holdings of Treasuries to a three-year high as the dollar’s strength against the yen offset losses on the securities. (See link)

- Cash JGBs are mixed with yield movements ranging from -1.4bp (1-year) to +2.0bp (40-year). The benchmark 10-year yield is unchanged at 0.475%, below the BoJ's YCC limit of 0.50%. The intraday high so far has been 0.485%.

- The swap curve has also bear steepened with swap spreads wider out to the 20-year and tighter beyond.

- Next week the local calendar sees the Marine Day public holiday on Monday followed by the Tertiary Industry Index on Tuesday, Trade Balance and Machine Orders on Thursday and National CPI and International Investment Flow data on Friday.

- Liquidity Enhancement Auctions are scheduled for Wednesday (1-5-year) and Friday (5-15.5-year).

AUSSIE BONDS: Sharply Richer, At Bests, RBA Minutes & Employment Data Next Week

ACGBs are holding sharply higher (YM +9.0 & XM +7.0), near session highs, as US tsys regain losses seen early in the Asia-Pac session. There hasn’t been much domestic news flow other than the previously outlined appointment of RBA Deputy Governor Bullock as the new RBA governor when incumbent Philip Lowe’s term expires in September.

- DJ's Glynn writes the appointment of Michele Bullock represents continuity for financial markets, but it will also bring her career background in financial stability to the fore with household budgets teetering near collapse due to soaring interest rates. (See link)

- AFR's Joye writes that Bullock is the right choice for RBA at a critical time in the inflation fight (See link)

- Cash ACGBs are 7-10bp richer with the AU-US 10-year yield differential unchanged at +21bp.

- Swap rates are 7-9bp lower with the 3s10s curve steeper.

- The bill strip has bull flattened with pricing +4 to +11.

- RBA dated OIS is 4-5bp softer for meetings beyond November.

- Next week the local calendar sees the RBA Minutes for the July Meeting on Tuesday and NAB Business Confidence (Q2) and Employment data on Thursday.

- The AOFM has announced that it plans to sell A$800mn of the 3.5% December 2034 bond on Wednesday.

FOREX: Yen Firms In Asia

The yen has continued its recent gains in Asia on Friday, USD/JPY is down ~0.3% Thursday's lows have been breached. Elsewhere in G-10 ranges have been narrow with little follow through.

- USD/JPY prints at ¥137.60/70, the next resistance level for the pair is ¥137.36 50.0% retracement of Mar 24 - Jun 30 bull leg. The Yen benefited from speculation from a report in Yomiuri that the BoJ will likely raise the FY23 Inflation forecast above 2%.

- Kiwi is marginally firmer, benefitting from some spillover in the Yen bid and higher regional equities. Local markets have been closed for the observence of a national holiday today. NZD/USD sits a touch above the $0.64 handle having marginally pared gains.

- AUD/USD is little changed, The pair last prints at $0.6885/90, resistance comes in at $0.69 and support is at $0.6784 the low from Jul 13. There has been little reaction thus far to the appointment of Michele Bullock as the next RBA Governor.

- Elsewhere in G-10 EUR is marginally firmer and GBP is a touch pressured.

- Cross asset wise; BBDXY is down ~0.1% and Hang Seng is up ~0.3%. US Tsy Yields are a touch firmer across the curve.

- There is a thin docket in Europe today, further out the latest UofMich Consumer Sentiment headlines.

EQUITIES: Regional Equities Track Higher, PBoC Pledges Policy Support

Regional equities are tracking higher, albeit with less positive impetus compared to recent sessions. US equity futures are mixed, with Eminis down a touch to 4541, although we are above session lows of 4534.50. Nasdaq futures are a touch higher, last 15724.

- The HSI started higher, but is back sub 19400 at the break, still +0.25% above closing levels from Thursday. The tech sub index is down -0.40%, possibly ending the strong positive run seen this week.

- The PBoC had a press confidence where it pledged to support the economic recovery with available policy tools. The authorities also stated that it would tailor support for the property sector.

- The CSI 300 is +0.17% at the break, holding above 3905.

- Elsewhere, the Kospi and Taiex are both +1% higher, buoyed by recent tech gains amid the core yield pull back. The Kospi is now back above the 2600 level. We aren't too far off early June highs around 2650.

- The ASX 200 has climbed 0.83%, with the Australian Government picking Deputy Governor Bullock to replace Phil Lowe as Governor, which should ensure policy continuity.

- SEA markets are in the green, except for the Philippines (-0.50%). Thai stocks are +1% firmer, despite continuing uncertainty as to who will be the new PM.

OIL: Tracking Higher For The 3rd Straight Week, Brent Close To 200-day MA Resistance

Current Brent levels, $81.45/bbl, are little changed to NY closing levels from Thursday. We aren't too far off session lows ($81.35/bbl), with Brent consolidating so far in the Asia Pac session. Earlier highs were at $81.70/bbl. We are tracking firmly higher for the week though, ~+3.75% at this stage. This follows the 4.77% gain last week and would be the 3rd straight week of gains. WTI was last around $77/bbl, and tracking +4.15% firmer for the week.

- For Brent, focus remains on late April highs, just above $83/bbl, which would also coincide with a test of the simple 200-day MA (close to $82.50/bbl). Note the 200-day EMA is slightly lower around $82.30/bbl.

- The combination of the USD pull back, tighter supply (with disruptions in Libya announced on Thursday), coupled with China pledges of policy support, have been supportive of recent gains.

- Looking ahead, the G20 meetings kick off this Sunday in India and continue to the 18th.

- On Monday we get an update on China's economic backdrop, with 2Q GDP out, along with June monthly activity figures.

GOLD: On Track For Best Week Since April

Gold remains steady in the Asia-Pacific session, following a relatively unchanged closing on Thursday. This occurred despite the US dollar dropping below 100 for the first time since April 2022 and a significant rally in US Treasury yields. Nevertheless, bullion is on track to achieve its best week since April, as investors solidify their belief that the Federal Reserve is nearing the end of its interest rate hikes, supported by recent US data indicating a slowdown in inflation.

- Some traders are now cautioning about the potential for disinflation, considering the cooler-than-expected US CPI and PPI figures released this week.

- Gold's recent gains indicate a turnaround from the loss of momentum experienced in June, which was fueled by successive reports suggesting elevated price pressures.

- Having previously cleared resistance at the 50-day EMA, resistance is next eyed at $1968.0 (Jun 16 high), according to MNI’s technicals team. Key resistance has been defined at $1985.3, the May 24 high where a break would highlight a stronger reversal. The key support and the bear signal is at $1893.1, the Jun 29 low. Initial support is at $1931.70, the 20-day EMA.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 14/07/2023 | 0600/0800 | *** |  | SE | Inflation Report |

| 14/07/2023 | 0900/1100 | * |  | EU | Trade Balance |

| 14/07/2023 | - | | EU | ECB de Guindos in Ecofin Meeting | |

| 14/07/2023 | 1230/0830 | ** |  | CA | Monthly Survey of Manufacturing |

| 14/07/2023 | 1230/0830 | ** |  | US | Import/Export Price Index |

| 14/07/2023 | 1300/0900 | * | | CA | CREA Existing Home Sales |

| 14/07/2023 | 1400/1000 | ** | | US | U. Mich. Survey of Consumers |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.