Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- LAST-MINUTE US SHUTDOWN DEAL UNLIKELY AS MCCARTHY LACKS LEVERAGE - BBG

- ABSENT DONALD TRUMP DRAWS FIRE FROM REPUBLICAN RIVALS - FT

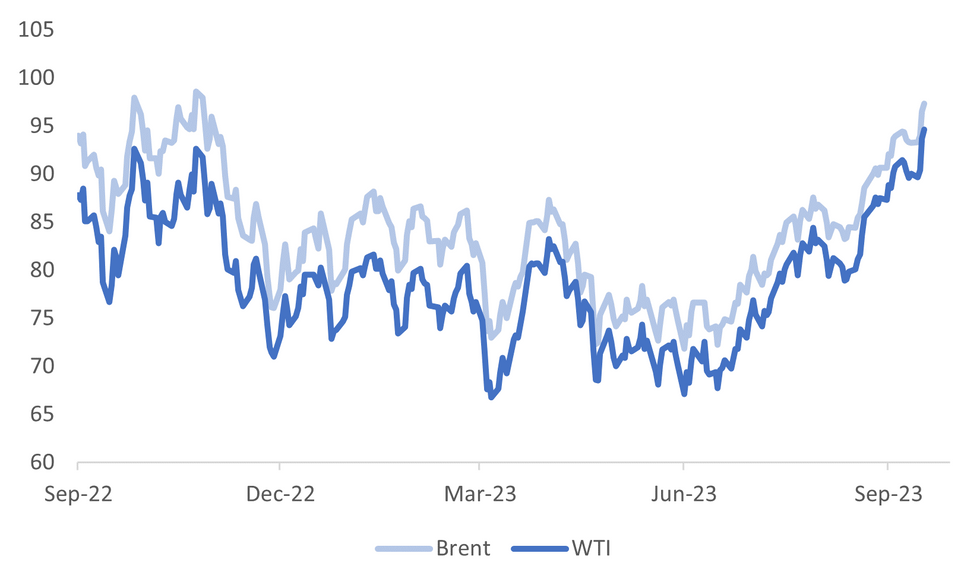

- OIL HITS $95 AFTER STOCKPILES AT US HUB DROP TO CRITICAL LEVELS - BBG

- AUSTRALIAN RETAIL SALES COOL, BOOSTING CASE TO EXTEND RATE PAUSE - BBG

- YUAN SUPPORTED BY PBOC FIXING BEFORE GOLDEN WEEK - BBG

- TARIFF CUTS HARD, DESPITE REFRESHED CHINA-US DIALOUGE - MNI

Fig. 1: Brent & WTI Hit Fresh Year-To-Date Highs

Source: MNI - Market News/Bloomberg

U.K:

ENERGY: Britain’s electricity and gas grid operators said on Thursday they expect to have sufficient supplies this winter, with more power generation available than last year and brimming gas stores across Europe, but cautioned geopolitical risks remain. (RTRS)

HOUSING: Almost a quarter of British mortgage holders are considering selling up after the surge in borrowing costs, threatening to pile pressure on the struggling housing market. Just under a 10th of mortgage holders have already sold and moved to a cheaper property in response to the surge in interest rates, according to a survey released Thursday by KPMG. However, a further 22% are considering moving to a cheaper home as they refinance loans at at much higher costs. (BBG)

HOUSING: London and southeast England are seeing the biggest UK home discounts as buyers across the country secure the largest price cuts nationwide in almost five years. The average discount to asking price for a newly agreed home sale was nearly 5% in London and southeast England this month, according to a report from property portal Zoopla. That compared with a 2.8% discount for properties elsewhere in the UK and a national average of 4.2%, the biggest reduction since March 2019. (BBG)

EUROPE:

FRANCE: France is exploring ways to cap national electricity prices without falling foul of EU subsidy rules, including a possible windfall levy to deliver President Emmanuel Macron’s pledge to take control of energy prices. (FT)

EU/CHINA: As Europe’s top trade chief headed to Beijing this month shortly after announcing a probe into China’s electric vehicle subsidies, some in the bloc braced for fiery criticism and any hint of retaliation. Instead, the Europeans found President Xi Jinping’s government ready to talk, make promises and avoid aggressive rhetoric that could inflame an economic relationship worth $900 billion. While Vice Premier He Lifeng expressed “concern and dissatisfaction” over the probe, he agreed to set up several working groups including on financial services and trade curbs. (BBG)

ITALY: Banca Monte dei Paschi di Siena SpA could form the country’s third-biggest bank through a merger with a peer, Italian Finance Minister Giancarlo Giorgetti said. “Monte Paschi can become the core from which to build a strong banking group,” Giorgetti told reporters during a press conference in Rome on Wednesday. “We don’t need to cash in right away,” he added referring to a possible sale of the bank. (BBG)

DEFENSE: The European Union will seek to boost its defense capabilities in response to a more hostile global environment as the bloc’s 27 governments start to define the political direction for the coming years.“We will strengthen our defence readiness and develop the European defence technological and industrial base, including with more investments,” according to the draft of the declaration EU leaders will discuss in Granada, Spain, next week and seen by Bloomberg News. (BBG)

U.S.

FISCAL: A late deal to avert a US government shutdown beginning this weekend isn’t likely — with House Speaker Kevin McCarthy making big demands of President Joe Biden and bringing little leverage to the clash. The Republican leader counts as one his proudest achievements an agreement on long-term spending cuts he extracted from Biden in last spring’s showdown over a potential US debt default and now he wants to use a shutdown to get more concessions. (BBG)

POLITICS: Republican candidates led by Ron DeSantis attacked Donald Trump for skipping the second Republican presidential debate, as they scrapped to stand out in a crowded field that remains dominated by the former president. The taunts from Republican rivals came shortly after Trump spoke in Michigan to rally support for a new term in the White House from blue- collar workers in the rustbelt, amid a strike roiling the car sector. (FT)

OTHER

COMMODITIES: US benchmark oil hit $95 a barrel for the first time in more than a year after a drop in stockpiles at the nation’s major storage hub to critical levels highlighted a widening global deficit. (BBG)

JAPAN: Major Japanese casualty insurers found that they fixed prices in dealings with more than 100 corporate clients in internal probes, Nikkei reports citing an unidentified person.(Nikkei)

HONG KONG: Hong Kong’s finance chief hints that the government could soon ease the city’s property cooling measures, South China Morning Post reports. Financial Secretary Paul Chan said conditions that prompted authorities to impose such moves more than 10 years ago no longer prevailed today. (SCMP)

AUSTRALIA: Australian retail sales rose at a weaker pace than expected in August in a sign that the Reserve Bank’s rapid interest-rate increases are weighing on the economy. Sales advanced 0.2% from a month earlier, slightly below estimates for a 0.3% rise, Australian Bureau of Statistics data showed Thursday. The gain was driven by clothing and dining out. (BBG)

AUSTRALIA: Australian Treasurer Jim Chalmers described as “bizarre and wrong” claims that a planned overhaul of the Reserve Bank represents a radical reshaping of the institution, saying its board structure will remain essentially the same as it has for the past 60 years. (BBG)

NEW ZEALAND: New Zealand's business confidence index rose to 1.5 in September from -3.7 in August, according to ANZ Bank New Zealand. The New Zealand economy is certainly patchy, and the rebound in activity indicators that’s been evident since the start of the year may be running out of steam. Inflation pressures are gradually waning in the big picture, but not rapidly nor in a straight line, and the jury remains out on whether it’s occurring fast enough to bring core inflation pressures down in a timely fashion. (BBG)

BRAZIL: President Luiz Inacio Lula da Silva and central bank chief Roberto Campos Neto agreed to talk more often during a much-anticipated meeting at the presidential palace, their first face-to-face encounter following months of tension between Brazil’s leftist leader and the head of the monetary authority. (BBG)

CHINA

CHINA/US: The resumption of regular economic China-U.S. dialogue via the creation of working groups shows both countries want to avoid a costly decoupling, but any substantial breakthrough – such as tariff reduction – remains a distant prospect, policy advisors and market analysts told MNI. (MNI)

CREDIT: China is expected to step up its pro-growth efforts via monetary policy tools, and issue more loans in the fourth quarter, the Economic Information Daily reports Thursday, citing analysts. (ECONOMIC INFORMATION DAILY)

YUAN: The yuan was supported by another strongest fix signal on record before the Golden Week holidays in China starting Friday. (BBG)

PROPERTY: A record share of Chinese investors plan to cut their allocation in property over the next year, a new survey showed, underlining the difficulties Beijing is having breathing life back into the sector. The net share of respondents planning to cut their investment in domestic real estate over the next year rose to a record 31.7% in the third quarter of this year, according to the quarterly investor sentiment survey published by the Cheung Kong Graduate School of Business in Beijing. (BBG)

PROPERTY: China Evergrande Group and its units suspended trading in Hong Kong, a day after people familiar with the matter said the property giant’s founder had been taken away by police. No reason was given for the halt in a notice to the Hong Kong stock exchange on Thursday. (BBG)

DEBT: Inner Mongolia plans to issue CNY66.32 billion of refinancing bonds to repay corporate accounts in arrears that the government guaranteed before 2018. This is the first time a local government has used refinancing bonds to pay off debt in arrears, compared to the previous use of repaying the principal of maturing local-government bonds as well as swapping out existing local implicit debts. (Caixin)

CONSUMPTION: Services consumption will help support the economy next week during the week-long Mid-Autumn Festival and National Day holiday. A total of 217 million train tickets were sold from Sept 13-23, according to data by the China Railway, while the Civil Aviation Administration estimates over 21 million passengers will travel by plane during the break, with an average of over 17,000 flights a day. (Securities Daily)

PORK: The fall holidays in China are usually boom-time for pork consumption, as parties and cooler weather entice households to splurge on the nation’s favorite meat. But consumption is falling flat and supplies are ample. Much of the blame lies with a weak economy and financial uncertainty that to some degree has affected all of China’s commodities markets. Prices of hogs and pork, which usually rise in anticipation of shoppers opening their wallets, have actually fallen. It’s a troubling sign for an industry that has yet to recover from the constraints imposed by the pandemic. (BBG)

CHINA MARKETS

PBOC Injects Net 440 Bln Via OMO Thurs; Rates Unchanged

The People's Bank of China (PBOC) conducted CNY101 billion via 7-day reverse repo and CNY508 billion via 14-day reverse repo on Thursday, with the rate unchanged at 1.80% and 1.95%, respectively. The operation has led to a net injection of CNY440 billion after offsetting the maturity of CNY169 billion reverse repos today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.8118% at 09:27am local time from the close of 1.9513% on Wednesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 50 on Wednesday, compared with the close of 43 on Tuesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

PBOC Yuan Parity Higher At 7.1798 Thursday Vs 7.1717 Wednesday.

The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1798 on Thursday, compared with 7.1717 on Wednesday. The fixing was estimated at 7.3224 by Bloomberg survey today.

MARKET DATA

NZ SEPTEMBER ANZ ACTIVITY OUTLOOK 10.9; PRIOR 11.2

NZ SEPTEMBER ANZ BUSINESS CONFIDENCE 1.5; PRIOR -3.7

AUSTRALIA AUGUST RETAIL SALES M/M 0.2%; MEDIAN 03%; PRIOR 0.5%

AUSTRALIA AUG JOB VACANCIES Q/Q -8.9%; PRIOR -2.5%

CHINA AUGUST SWIFT GLOBAL PAYMENTS CNY 3.47%; PRIOR 3.06%

MARKETS

US TSYS: Marginally Richer In Asia

TYZ3 deals at 107-24, +0-05+, a narrow 0-05 range was observed on volume of ~105k.

- Cash tsys sit ~1bp richer across the major benchmarks.

- Tsys have observed narrow ranges in a data light session in Asia, there has been little follow through on moves and little meaningful macro news flow crossed.

- Flow wise the highlight was a TY block buyer (5k lots).

- Regional German CPI provides the highlight in Europe today, further out we have Initial Jobless Claims and 3rd read of GDP. Fedspeak from Chair Poweel and Chicago Fed President Goolsbee is due. We also have the latest 7-Year Supply.

JGBS: Futures Weaker, Near Toyo Session Lows, Heavy Local Calendar Tomorrow Incl. Tokyo CPI

JGB futures are sitting cheaper and near Tokyo session cheaps, -15 compared to session cheaps.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined international investment flows.

- The cash JGB curve has bear-steepened, with yields 0.1bp to 1.5bps higher. The benchmark 10-year yield is 1.1bps higher at 0.752%. It is slightly lower than the cycle high of 0.756%, set prior to the September BOJ decision.

- The 2-year yield is at 0.031%, 0.4bp higher on the day, but 0.4bp lower in post-auction dealings. This is despite only adequate demand exhibited in today’s auction.

- Considering that today's auction took place amidst more positive demand indicators for 5-, 20-, and 40-year JGB offerings, the results might be viewed as somewhat lacklustre, especially given that the outright yield was the highest since January. The notable steepening of the 2/5 JGB yield curve over the past month, reaching its most pronounced point since January, appears to have influenced demand compared to the recent 5-year auction.

- The swaps curve has bear-steepened, with rates 0.5bp to 2.1bps higher. Swap spreads are wider beyond the 1-year.

- Tomorrow the local calendar is heavy with the release of Tokyo CPI, Jobless Rate, Job-To-Applicant Ratio, Retail Sales, Housing Starts and Consumer Confidence data.

AUSSIE BONDS: Hovering Near Session Cheaps Despite Weakish Data

ACGBs (YM -8.0 & XM -8.5) are hovering near the lows of the Sydney session, despite a generally soft release of domestic data. As previously mentioned, August retail sales slightly underperformed expectations (+0.2% m/m versus an estimated +0.3%), and job vacancies experienced an 8.9% decline q/q in the three months leading up to August. With US tsys richer in Asia-Pac trading, the afternoon dip in ACGBs appears to be more of a correction following their earlier outperformance relative to US tsys.

- Cash ACGBs are 7-8bps cheaper, with the AU-US 10-year yield differential 1bp lower at -14bps.

- Swap rates are 6bps higher on the day.

- The bills strip bear-steepens, with pricing -1 to -10.

- RBA-dated OIS pricing is 3-6bps firmer on the day for '24 meetings.

- Tomorrow the local calendar sees Private Sector Credit data for August.

- Tomorrow the AOFM plans to sell A$800mn of the 2.25% 21 May 2028 bond.

- Households have drawn down on their bank account savings for the first time since the last major interest rate tightening cycle in 2007, as higher borrowing costs also squeeze retail spending. (See link)

NZGBS: Closed Near Session Highs, Outperformed $-Bloc Peers

NZGBs closed at or near session bests, with benchmarks 3-6bps cheaper. The move away from session cheaps came despite a lift in ANZ business confidence and lacklustre demand metrics for weekly supply. The cover ratios for today’s auction lines were a low 1.65x to 2.44x. Nonetheless, the bond lines were 2-3bps richer in post-auction dealings, with the May-51 bond outperforming.

- The NZGB 10-year benchmark outperformed its $-bloc peers by 2-3bps.

- Swap rates are 2-4bps higher, with the 2s10s steeper.

- RBNZ dated OIS pricing is flat to 2bps firmer across meetings, with terminal OCR expectations at 5.77%.

- The business confidence index rose to 1.5 in September from -3.7 in August, according to ANZ. This was the first positive read since May 2021. The business activity outlook index fell to 10.9 from 11.2 in August. Inflation expectations eased to 4.95% from 5.06%. ANZ said the NZ economy is certainly patchy, and the rebound in activity indicators that’s been evident since the start of the year may be running out of steam, according to Bloomberg. Inflation pressures are gradually waning in the big picture, but not rapidly nor in a straight line: ANZ.

- Tomorrow the local calendar sees ANZ Consumer Confidence.

EQUITIES: Ex-Dividend Day/Oil Surge Hits Japan Stocks, China Property Concerns Remain

Japan stocks are noticeably weaker in Thursday trade, the major indices off nearly 2%. A number of markets are shut including South Korea and Indonesia. This is also China's last trading day ahead of the extended Golden Week break. US equity futures were higher in early trade, but couldn't sustain these levels. Eminis sit down slightly, last at 4309, after getting to 4326.50 earlier. We are above Wednesday intra-day lows sub 4280 though.

- Japan stocks are noticeably weaker. The Nikkei 225 off around 2% at this stage. The Topix down ~1.90%. The continued climb higher in oil prices have weighed from a broader macro standpoint. The local 20yr yield hit fresh highs back to 2014, while the yen also strengthened marginally.

- Also note that the Topix was weighed by over 1000 stocks going ex-dividend. Local analysts also indicated that a possible portfolio adjustment from the GPIF may be weighing as well.

- At the break the HSI is down a little 1%. Shares of struggling property conglomerate Evergrande have been suspended, which hasn't helped sentiment. While Country Garden dollar bond holders are reportedly yet to receive coupon payments which were due on Wednesday.

- In China, the CSI 300 is off 0.28% at the break. The other major indices slightly higher. Note this is the final trading session for China markets until we return from the Golden Week break on Oct 9.

- In Australia, the ASX 200 is off 0.40%. In SEA Thailand and Philippine stock indices are modestly higher.

FOREX: Antipodeans Trim Wednesday's Losses

The Antipodeans have firmed in Asia trimming some of Wednesdays losses, US Tsy Yields have ticked lower and the Bloomberg Commodity Index has ticked higher.

- AUD/USD is up ~0.4% and last prints at $0.6375/80. The pair looked through a weaker than forecast Retail Sales print in August (0.2% M/M vs exp 0.3%). The trend condition remains bearish and support now comes in at $0.6287, 2.000 projection of the Jun 16-Jun 29-Jul 13 price swing. Resistance comes in at the 20-Day EMA ($0.6435).

- Kiwi is firmer, NZD/USD is up ~0.4% and sits at $0.5945/50. The pair has continued the move seen late in yesterdays NY session and now targets the Sep 22 high ($0.5989) after recovering above the 20-Day EMA today.

- The Yen is a touch firmer however ranges have been relatively narrow. USD/JPY last prints at ¥149.40/45. The trend continues to be bullish, resistance comes in at ¥147.71, high from Oct 24 2022. Support is at ¥147.29, the 20-Day EMA.

- Elsewhere in G-10 there hasn't been much movement and ranges have been narrow.

- Regional German CPI provides the highlight in Europe today.

OIL: Tight Supply/China Demand, Fuel Further Gains

Brent crude extended Wednesday gains in the first bit of Thursday trade. We touched fresh highs of $97.69/bbl, but have consolidated somewhat since. The benchmark was last at $97.30/bbl, still +0.80% above Wednesday closing levels and tracking higher for the fourth straight session. WTI poked above $95/bbl (high of $95.03), but now sits slightly lower, last near $94.60/bbl.

- Today's momentum has largely been about concern on the supply side, following US data on Wednesday showing inventories at Cushing dropped below 22mln barrels, the weakest result since July 2022 and near operating minimums. Not surprisingly WTI prompt spreads remain very elevated.

- Analysts at J.P. Morgan also note that stronger China trucking activity as well as a pick in international travel ahead of the Golden Week period is providing additional support from a demand stand point (see this link).

- Focus for Brent is on whether we can break above $100/bbl, levels that haven't been seen since August last level. Note that the Nov 2022 high was $99.56/bbl. The 20-day EMA is back near ~$92/bbl on the downside.

GOLD: Steady In Asia-Pac After A Very Heavy Wednesday

Gold is steady in the Asia-Pac session, after closing -1.3% at $1875.12 on Wednesday Bullion faced downward pressure driven by a strengthening US dollar, which surged to a new year-to-date high, primarily due to the soaring US Treasury yields, reaching fresh multi-year peaks.

- Both the 2-year and 10-year yields concluded the day 7 basis points higher, settling at 5.135% and 4.61%, respectively. These moves were influenced by factors such as the rising oil prices, the looming possibility of a federal government shutdown within days, and escalating labour disputes, notably involving the United Auto Workers.

- He suggested that the Federal Reserve might need to implement more than one additional interest rate hike. However, he also acknowledged that a potential US government shutdown or an extended strike by automotive workers could potentially slow down the economy, potentially obviating the need for the Federal Reserve to deploy its policy tools to combat inflation.

- According to MNI’s technical team, the yellow metal pushed through two support levels including the bear trigger at $1884.9 (Aug 21 low). However, Wednesday’s low of $1872.7 stopping short of next support at $1871.6 (Mar 13 low).

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 28/09/2023 | 0530/0730 | *** |  | DE | North Rhine Westphalia CPI |

| 28/09/2023 | 0700/0900 | *** |  | ES | HICP (p) |

| 28/09/2023 | 0800/1000 | ** |  | IT | ISTAT Business Confidence |

| 28/09/2023 | 0800/1000 | ** | | IT | ISTAT Consumer Confidence |

| 28/09/2023 | 0800/1000 | *** | | DE | Baden Wuerttemberg CPI |

| 28/09/2023 | 0800/1000 | *** | | DE | Bavaria CPI |

| 28/09/2023 | 0900/1100 | ** |  | EU | EZ Economic Sentiment Indicator |

| 28/09/2023 | 0900/1100 | ** | | IT | PPI |

| 28/09/2023 | 0900/1100 | *** | | DE | Saxony CPI |

| 28/09/2023 | 0930/1030 |  | UK | BoE's Hauser Speaks at MNI | |

| 28/09/2023 | 1200/1400 | *** | | DE | HICP (p) |

| 28/09/2023 | 1230/0830 | *** |  | US | Jobless Claims |

| 28/09/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 28/09/2023 | 1230/0830 | * |  | CA | Payroll employment |

| 28/09/2023 | 1230/0830 | *** | | US | GDP |

| 28/09/2023 | 1300/0900 | | US | Chicago Fed's Austan Goolsbee | |

| 28/09/2023 | 1400/1000 | ** | | US | NAR Pending Home Sales |

| 28/09/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 28/09/2023 | 1445/1545 | | UK | BOE's Greene speaks on panel | |

| 28/09/2023 | 1500/1100 | ** | | US | Kansas City Fed Manufacturing Index |

| 28/09/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 28/09/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 28/09/2023 | 1700/1300 | ** | | US | US Treasury Auction Result for 7 Year Note |

| 28/09/2023 | 1700/1300 | | US | Fed Governor Lisa Cook | |

| 28/09/2023 | 1900/1500 | *** |  | MX | Mexico Interest Rate |

| 28/09/2023 | 2000/1600 | | US | Fed Chair Jerome Powell | |

| 28/09/2023 | 2300/1900 | | US | Richmond Fed's Tom Barkin |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.