Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- LAGARDE: THE ECB EXPECTS TO CONTINUE RAISING INTEREST RATES TO CONTROL INFLATION (DELFI BIZNESS)

- SUNAK SIGNS OFF ON TAX RISES ACROSS THE BOARD TO HELP PLUG £50BN HOLE (FT)

- UK LABOUR LEADS TORIES BY 23 POINTS IN LATEST POLL, GAP NARROWS (BBG)

- JAPAN'S STEALTH YEN INTERVENTION AIMS FOR MAXIMUM IMPACT - FINANCE MINISTER (RTRS)

- RBA HIKES 25BP; SEES INFLATION PEAK 'AROUND' 8% (MNI)

- U.S. SETS TIMELINE FOR RUSSIAN OIL CARGOES SUBJECT TO PRICE CAP (RTRS)

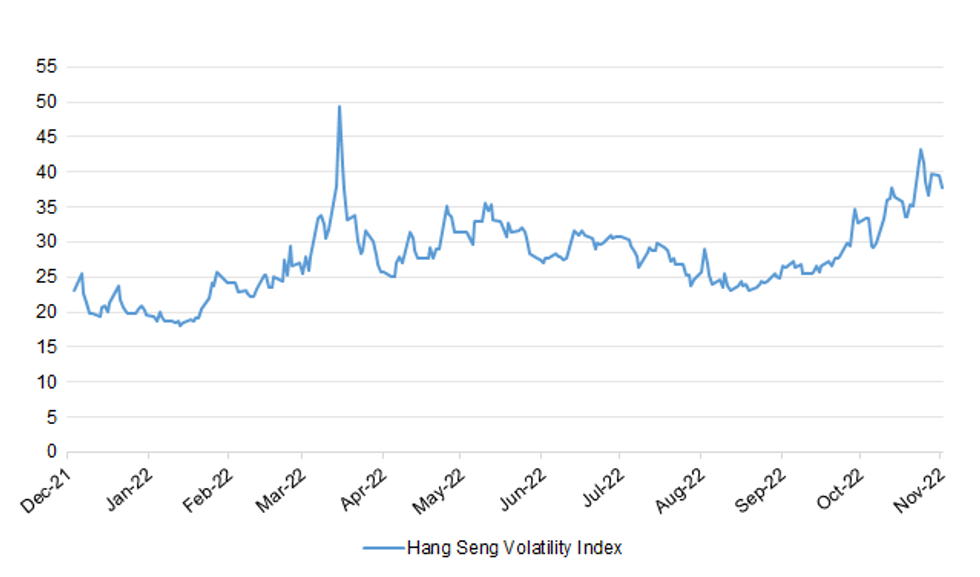

Fig. 1: Hang Seng Volatility Index

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

UK

FISCAL: Rishi Sunak is set to sign off on raising taxes across the board as the new British prime minister looks to plug a £50bn hole in public finances. (FT)

FISCAL: Tax rises are "likely" to come soon as the government faces an "unpalatable menu" to find ways to fill a £40bn fiscal black hole, a leading think tank has warned. (Sky)

FISCAL: Millions of public sector workers face a pay squeeze next year as the government seeks to fill a £35 billion gap in the public finances. (The Times)

POLITICS: The UK Labour Party led the Conservatives by 23 points in a poll on Monday that showed the opposition advantage over the ruling party narrowing since Rishi Sunak became prime minister last week. (BBG)

POLITICS: Keir Starmer has been urged to get Labour on a general election footing with a “laser-sharp” focus on wooing voters with a small number of key pledges that demonstrate the party’s priorities rather than a sprawling plethora of policies. (Guardian)

EUROPE

ECB: In an effort to curb the rapid rise in prices in the eurozone, the European Central Bank (ECB) has raised interest rates by 200 basis points since July this year, which is the fastest increase in the history of the euro. "The destination is clear, and we haven't reached it yet," says Christine Lagarde, president of the European Central Bank (ECB), in an exclusive interview with the "Delfi Bizness" portal. She points out that the ECB is committed to doing everything necessary to bring inflation back to the 2% target level. (Delfi Bizness)

BANKS: Any bargain hunters hoping to snap up Credit Suisse Group AG now that the lender’s revamp has pushed its stock down yet again may find themselves getting short shrift in Zurich. (BBG)

U.S.

FISCAL: The U.S. Treasury Department on Monday announced it expects to borrow USD550 billion in privately-held net marketable debt in the fourth quarter, USD150 billion more than previously announced in August. (MNI)

EQUITIES: Apple Inc.’s top executives in charge of its online retail store and information-systems divisions are stepping down, according to people with knowledge of the matter, bringing changes to two key parts of the tech giant’s operations. (BBG)

OTHER

GLOBAL TRADE: Russia is not ending its participation in a deal to export Ukrainian grain through Black Sea ports but rather is suspending it, President Vladimir Putin told a news conference on Monday. (RTRS)

GLOBAL TRADE: Russia warned that the security of ships sailing Ukraine’s grain-export corridor cannot be guaranteed without additional conditions, increasing risks for Black Sea trade after Russia halted involvement in a key accord. (BBG)

GLOBAL TRADE: The European Union hopes to resolve in upcoming negotiations a dispute with the US over new subsidies for North American manufacturers, a senior diplomat from the bloc said on Monday. (BBG)

GLOBAL TRADE: Australia’s resources minister said it was a “pipe dream” that Western countries could soon end their reliance on China for rare earths and critical minerals -- vital for the defense, aerospace and automotive industries -- due to the Asian powerhouse’s existing grip on global markets. (BBG)

GLOBAL TRADE: TSMC cuts as much as 40%-50% of initially planned orders this year to some suppliers, including recycled wafers, key consumables and equipment, Taipei-based Economic Daily News reports, citing unidentified people in the industry. (BBG)

JAPAN: Japan's currency interventions have been stealth operations in order to maximise effects of its forays into the market, Finance Minister Shunichi Suzuki said on Tuesday, after the government spent a record $43 billion supporting the yen last month. (RTRS)

JAPAN: Tokyo Electric Power will consider seeking government permission to raise household electricity bills, following similar moves by other utilities in Japan amid soaring fuel costs, Yomiuri reports without attribution. (BBG)

BOJ: Bank of Japan (BOJ) Governor Haruhiko Kuroda said on Tuesday the central bank must maintain ultra-loose monetary policy to support an economy that is still recovering from the COVID-19 pandemic. (RTRS)

RBA: The Reserve Bank of Australia raised rates 25bp to 2.85%, warning inflation will peak at "around" 8% later this year as it cut its growth forecasts out to 2024. (MNI)

RBNZ: The Reserve Bank of New Zealand said on Tuesday a preliminary analysis of its climate change stress test indicated that river and surface water flooding may pose an even greater risk to lenders' residential mortgage portfolios than coastal flooding. (RTRS)

SOUTH KOREA: South Korea's five large financial groups decided Tuesday to inject a large amount of liquidity into the financial market to help ease its recent volatility. (Yonhap)

NORTH KOREA: North Korea on Monday called on the United States and South Korea to stop large-scale military exercises in the region, calling them a provocation that may draw "more powerful follow-up measures" from Pyongyang, KCNA reported, citing a North Korean foreign ministry statement. (RTRS)

HONG KONG: Hong Kong Monetary Authority’s chief executive has defended Hong Kong’s currency peg, saying it helped see the city through some of its toughest economic challenges. (CNBC)

MEXICO: Mexico central bank deputy governor Jonathan Heath said in a tweet assuming no revisions and 4Q growth of 0.0%, GDP will have grown 2.6% in 2022. “It’s very likely we will see (minor) revisions in the growth of previous quarters,” Heath said. (BBG)

TURKEY: Turkey’s central bank warned commercial lenders against actions that it said lessen the effectiveness of official policies, and asked them to keep interest rates on deposits lower. (BBG)

BRAZIL: President Jair Bolsonaro will not publicly address his defeat in Brazil's presidential election until Tuesday, a minister said, amid doubts over whether the far-right nationalist will accept the victory of his leftist rival Luiz Inacio Lula da Silva. (RTRS)

BRAZIL: Brazilian Senator Jean Paul Prates, a close ally of President-elect Luiz Inacio Lula da Silva, is a strong candidate to head state-run oil company Petrobras next year, according to three people familiar with the matter. (RTRS)

RUSSIA: Russian President Vladimir Putin said that he had not yet decided on possible trips to the G20 and APEC summits. (Urdu Point)

RUSSIA: Japan will keep its investment in the Sakhalin-1 oil and gas project in Russia, said the nation’s trade chief. (BBG)

SOUTH AFRICA: Finance Minister Enoch Godongwana says government's commitment to take on between a third and two-thirds of Eskom's R400 billion debt will come with conditions – including that the utility invests in gas and nuclear power. (News 24)

OIL: The U.S. Treasury Department on Monday said vessels of Russian petroleum that are loaded before Dec. 5 and unloaded at their destination before Jan. 19, will not be subject to the price cap being planned by Western governments. The U.S. government, the G7 and the EU plan to impose the price cap which begins on Dec. 5 as part of sanctions against Russia for its invasion of Ukraine. The exact price levels of the caps, which will be placed on shipments of Russian crude oil and oil products, is still being worked out. (RTRS)

OIL: US president Joe Biden charged oil companies were “profiteering” from Russia’s invasion of Ukraine as he threatened them with legislation to impose a windfall tax unless they increase output. (FT)

CHINA

YUAN: Volatility in the yuan is still acceptable for China but it should stand ready to face down currency speculators with a greater force than Japan if needed, according to a former official at the country’s foreign exchange regulator. (BBG)

YUAN: The yuan may endure short-term depreciation pressure as the Federal Reserve continue to hike rates, while China's weak exports, Covid disruptions and real estate downturn also weigh on the currency, Yicai.com reported citing analysts. (MNI)

FISCAL: China's Ministry of Finance will support Shenzhen as it explores innovative fiscal policy and new management systems through measures to help the city meet housing demand and increase its local government bond issuance, according to a document released on the ministry's website. (MNI)

BONDS: There were net purchases of domestic yuan bonds by foreign investors in October, reported financial news agency Cls.cn citing a source close to the State Administration of Foreign Exchange. (MNI)

BONDS: China’s property debt crisis is entering a new phase as even partially state-backed developers and private-sector giants that had long been considered safer rapidly tumble into distress. (BBG)

CORONAVIRUS: Five districts in China’s Dandong city have been locked down from Tues. till Friday to cut Covid spread, the local government says in a statement on Weibo. (BBG)

CHINA MARKETS

PBOC NET DRAINS CNY215 BILLION VIA OMOS TUESDAY

The People's Bank of China (PBOC) on Tuesday injected CNY15 billion via 7-day reverse repos with the rates unchanged at 2.00%. The operation has led to a net drain of CNY215 billion after offsetting the maturity of CNY230 billion reverse repos today, according to Wind Information.

- The operation aims to keep liquidity reasonable and ample, the PBOC said on its website.

- The 7-day weighted average interbank repo rate for depository institutions (DR007) rose to 1.9500% at 9:28 am local time from the close of 1.9442% on Monday.

- The CFETS-NEX money-market sentiment index closed at 68 on Monday vs 50 on Friday.

PBOC SETS YUAN CENTRAL PARITY AT 7.2081 TUES VS 7.1768 MON

The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.2081 on Tuesday, compared with 7.1768 set on Monday, marking the weakest parity since Jan 24, 2008.

OVERNIGHT DATA

CHINA OCT CAIXIN MANUFACTURING PMI 49.2; MEDIAN 48.5; SEP 48.1

The Caixin China General Manufacturing PMI in October rose 1.1 points from the previous month to 49.2, but remained in contractionary territory. This marked the third consecutive month of contraction in manufacturing activities, still weighed down by Covid-19 outbreaks and consequent tightening of prevention and containment measures. (Caixin)

JAPAN OCT, F JIBUN BANK MANUFACTURING PMI 50.7; PRELIM 50.7

The latest survey data signalled that Japan’s manufacturing sector lost further momentum in October. Sluggish markets and weaker demand conditions, on both a domestic and international level, became a recurring trend throughout the report and were seemingly the driving forces behind the slower sector performance. Anecdotal evidence suggested that worsening conditions in China and South Korea were specifically detrimental to Japan’s exports this month. (S&P Global)

JAPAN OCT VEHICLE SALES +19.7% Y/Y; SEP +17.8%

AUSTRALIA OCT, F S&P GLOBAL MANUFACTURING PMI 52.7; PRELIM 52.8

The latest Australian Manufacturing PMI reflected continued expansion at the start of the fourth quarter, though the rate of growth slowed from September. Foreign demand for Australian manufactured goods notably saw growth slow to almost a halt in the latest survey. (S&P Global)

AUSTRALIA OCT CORELOGIC HOUSE PRICE INDEX -1.1% M/M; SEP -1.4%

AUSTRALIA ANZ-ROY MORGAN WEEKLY CONSUMER CONFIDENCE INDEX 79.9; PREV 81.1

Consumer confidence decreased 1.5% last week, with the federal budget having no clear positive impact. The Q3 CPI hitting a 32-year high has pushed household inflation expectations to 6.6%, their highest since February 2011. (ANZ)

AUSTRALIA OCT COMMODITY INDEX AUD 157.2; SEP 154.1

AUSTRALIA OCT COMMODITY INDEX SDR +22.4% Y/Y; SEP +31.9%

NEW ZEALAND SEP BUILDING PERMITS +3.8% M/M; AUG -1.6%

SOUTH KOREA OCT TRADE BALANCE -$6.700BN; MEDIAN -$3.500BN; SEP -$3.778BN

SOUTH KOREA OCT EXPORTS -5.7% Y/Y; MEDIAN -2.1%; SEP +2.7%

SOUTH KOREA OCT IMPORTS +9.9% Y/Y; MEDIAN +6.6%; SEP +18.6%

SOUTH KOREA OCT S&P GLOBAL MANUFACTURING PMI 48.2; SEP 47.3

PMI survey data for October continued to depict a negative image of the business conditions in South Korea's manufacturing sector. Both output and new orders contracted again, with the rates of decline remaining solid overall. (S&P Global)

MARKETS

SNAPSHOT: RBA Sticks To 25bp Step, Notes Material Tightening Deployed

Below gives key levels of markets in the second half of the Asia-Pac session:

- Nikkei 225 up 63.29 points at 27650.75

- ASX 200 up 113.44 points at 6976.9

- Shanghai Comp. up 29.2 points at 2922.338

- JGB 10-Yr future up 4 ticks at 148.81, yield up 0.3bp at 0.251%

- Aussie 10-Yr future down 0.5 tick at 96.230, yield down 0bp at 3.755%

- U.S. 10-Yr future +0-10 at 110-29, yield down 2.66bp at 4.0212%

- WTI crude up $0.62 at $87.15, Gold up $5.40 at $1638.96

- USD/JPY down 33 pips at Y148.38

- LAGARDE: THE ECB EXPECTS TO CONTINUE RAISING INTEREST RATES TO CONTROL INFLATION (DELFI BIZNESS)

- SUNAK SIGNS OFF ON TAX RISES ACROSS THE BOARD TO HELP PLUG £50BN HOLE (FT)

- UK LABOUR LEADS TORIES BY 23 POINTS IN LATEST POLL, GAP NARROWS (BBG)

- JAPAN'S STEALTH YEN INTERVENTION AIMS FOR MAXIMUM IMPACT - FINANCE MINISTER (RTRS)

- RBA HIKES 25BP; SEES INFLATION PEAK 'AROUND' 8% (MNI)

- U.S. SETS TIMELINE FOR RUSSIAN OIL CARGOES SUBJECT TO PRICE CAP (RTRS)

US TSYS: Firmer In Asia, Although Chinese Equity Bounce Caps Rally

Cash Tsys added to Monday’s late bounce from NY lows during Asia-Pac trade, with a move lower in the broader USD and then spill over from the ACGB space in the wake of the latest RBA decision helping the bid.

- The space has moved away from highs in recent dealing as Hong Kong & Chinese added to their already notable morning gains. Some have pointed to the verified and unverified re-opening headlines/whispers out of China that we have flagged in previous bullets as a driving factor for the bid in those equity indices.

- That leaves cash Tsys running 1.5-3.0bp richer across the curve, bull steepening. Meanwhile, TYZ2 deals +0-09 at 110-28, 0-03+ off the peak of its 0-11+ session range as volume in the contract nears 100K.

- The major flow in the space happened in the first half of Asia-Pac dealing, consisting of a 1.6K block sale of TY futures and a 5K screen lift of TYZ2 112.75 calls.

- NY hours will see the release of the ISM manufacturing survey and JOLTs job opening data, although participants are of course more focused on Wednesday’s FOMC decision.

JGBS: Notable Steepening Of The Curve Despite Solid 10-Year Auction

The JGB curve has extended its early steepening move during the Tokyo afternoon, with the major cash JGB benchmarks running 0.5bp richer to 7.5bp cheaper ahead of the bell. The pivot has occurred around the 10-Year zone, which continued to be capped by the upper boundary of the trading range permitted by the BoJ’s YCC mechanism.

- 20+-Year paper has more than unwound yesterday’s richening.

- JGB futures are +6 ahead of the bell, a little shy of best levels after drawing support from the latest 10-Year JGB auction, which went well. We would suggest that short covering and outright plays based on the BoJ’s YCC mechanism being successfully defended were the key drivers of demand at today’s auction.

- Domestic headline flow saw familiar rhetoric re: the aim and stance of BoJ monetary policy, as BoJ Governor Kuroda made his latest appearance in front of parliament.

- Elsewhere, familiar language was deployed by Finance Minister Suzuki when it comes to FX intervention matters.

- Looking ahead, Wednesday’s local docket will be headlined the latest round of BoJ Rinban operations.

JGBS AUCTION: 10-Year JGB Auction Results

The Japanese Ministry of Finance (MOF) sells Y2.1805tn 10-Year JGBs:

- Average Yield: 0.248% (prev. 0.248%)

- Average Price: 99.53 (prev. 99.53)

- High Yield: 0.249% (prev. 0.250%)

- Low Price: 99.52 (prev. 99.51)

- % Allotted At High Yield: 42.7523% (prev. 14.1495%)

- Bid/Cover: 5.243x (prev. 5.552x)

AUSSIE BONDS: Curve Twist Steepens, Bonds Firm After RBA’s 25bp Hike

Aussie bonds firmed in the wake of the latest RBA decision, as the Bank deployed the widely expected 25bp rate hike, after stepping down to that increment at last month’s meeting. This came after some overnight/early Sydney cheapening.

- The fact that 32bp of tightening was priced into OIS for today’s decision, coupled with the Bank’s reference to the “material” tightening now deployed in the current cycle and a more overt reference to the lagged impact of monetary policy, allowed Aussie bonds to firm post-decision.

- The major cash ACGB benchmarks were 4bp richer to 4bp cheaper at the close, twist steepening, with a pivot around 7s. YM was +4.0 & XM was -1.0. EFPs were wider again today, with the 3-/10-Year box flattening. Bills were 9bp richer to 5bp cheaper through the reds, as the strip twist steepened, pivoting around the front of the reds. Terminal cash rate pricing eased to ~3.95%.

- Focus now moves to the impending address from RBA Governor Lowe at the Bank’s Board dinner with the business community. Participants will be on the lookout for commentary around the scenarios that were discussed at today’s decision (with anywhere between no move in the cash rate to a 50bp rate hike having the potential to feature).

NZGBS: Bear Flattening On Tuesday

Weakness in NZGBs extended throughout the day as the space more than unwound yesterday’s WGBI inclusion-related bid.

- The major benchmarks finished 7.5-12.5bp cheaper across the curve, bear flattening, going out around cheapest levels of the session.

- Swap spreads were mixed, narrowing a touch at the shorter end, while they were wider to flat further out.

- RBNZ dated OIS pricing was little changed on the day.

- We suggest that some trans-Tasman spill over from the weaker ACGB complex ahead of today’s RBA decision may have aided today’s cheapening.

- Looking ahead, Wednesday’s local docket will see the release of the latest quarterly labour market report, CoreLogic house price data and the RBNZ’s FSR.

EQUITIES: Tracking Higher Led By HSI Rebound

Asia Pac stock indices are mostly higher. Focus remains on HK, where volatility continues, today to the upside. US equity futures are higher, but have not drifted too far from the +0.30/+0.40% range this afternoon.

- Dip buyers look to have emerged again to support the HSI. The index is up over 2.3% at this stage. We are down from earlier highs. The tech sub index was up +6% at one stage, but is now back to +4%. H shares are up by 2.24%.

- China mainland shares are higher, the CSI 300 +1.5%, the Shanghai Composite +0.86%. The Caixin manufacturing PMI surprised on the upside (49.2 versus 48.5 expected), which has helped at the margin. The property sub-index has underperformed though, down 1.42%. Debt payments were suspended by CIFI holdings, weighing on broader sentiment in the sector.

- The Kospi is up over 1.3%, with the index up over the 2300 level. The Taiex has lagged up 0.40%. TSMC is higher, but noted that it had cut procurement orders to some suppliers by up to 50%.

- The ASX 200 is up +1.28%, led by a mixture of names - finance and resource related.

- Indonesia (-0.65%) and Malaysia have been the two laggards today (-1.00%).

OIL: Softer USD Boosts Oil Prices Ahead Of Fed

Oil prices are slightly stronger today with WTI up 0.7% to just over $87/bbl and Brent + 0.8% to around $93.50 on the back of a weaker USD.

- WTI remains just above its 20-day moving average and continues to trade in the $85-$95/bbl range that it’s been in since the middle of the year.

- The market is awaiting the Fed decision on Wednesday, as another outsized 75bp hike is likely to worsen already heightened supply concerns. However, OPEC+ would probably reduce production further at any signs of weakening demand.

- The US tried to calm supply fears in the market by allowing ships that loaded Russian oil before December 5 until January 19 to unload.

- US President Biden made comments overnight that if oil and gas companies don’t use their excess profits from high prices to increase investment in increasing production, then the government would look at its options including increased taxation. In reality, this would be very difficult to achieve.

- OPEC expects demand for oil to remain strong into the mid-2000s and as a result called for more investment in the industry.

GOLD: Rebounds Amid Broad USD Pull Back

Gold is recouping some losses from the overnight session, up around 0.25% so far. This puts us back near $1638 for the precious metal, after the overnight 0.70% fall.

- Directional correlation with USD moves remains strong, with the BBDXY off by close to 0.20% so far today. Range for the session has been just under $1631 to $1640.

- The rebound in UST yields has us back in the bottom half of the recent range though. A move sub $1630 could see recent lows below $1620 targeted.

- Interestingly, the World Gold Council stated central bank demand for gold was quite strong in Q3, hitting record purchases. Countries like Turkey and Qatar raised holdings, although there also significant purchases which were not reported at the country level (see this link).

- This is likely to reflect FX reserve diversification flows.

- Elsewhere though, gold ETF holdings continue to trend lower.

FOREX: Greenback Sags Amid Positive Risk Tone, Aussie Trims Gains Post-RBA

The BBDXY dropped back towards the 1,330 level, roughly halving yesterday's advance, with U.S. Tsy yields easing across the curve. Pre-FOMC musings took centre stage, albeit another 75bp rate hike remains fully priced for this week's monetary policy review.

- Greenback underperformance was accentuated by the broader risk-on tone, which saw major safe haven currencies (JPY & CHF) trade on the back foot. E-mini futures crept higher, with the three main contracts last 0.32%-0.35% higher on the day, while strong performance from Hong Kong tech shares supported equity sentiment.

- The Aussie dollar pulled back from highs as the RBA raised the cash rate target by the expected 25bp, disappointing observers with more hawkish leanings (32bp of tightening was priced into dated OIS pre-decision). The central bank lowered its GDP outlook, while revising its CPI forecast higher.

- Post-RBA impetus helped AUD/NZD stage a clean breach of its 200-DMA, which provided support over the past 10 months. The spot rate sank in tandem with Australia/New Zealand 2-year swap spread amid the RBNZ's relatively hawkish posture. The kiwi tops the G10 scoreboard, leading the commodity-tied FX bloc higher.

- Offshore yuan weakened after the PBOC set the USD/CNY mid-point at a new cyclical high going back to early 2008, but recovered thereafter amid broad-based USD weakness. China's Caixin M'fing PMI rose to 49.2 last month, beating the consensus forecast of 48.5.

- A slew of manufacturing PMI readings from across the globe take focus from here. Speeches are due from RBA's Lowe, BoC's Macklem & Riksbank's Ingves.

FX OPTIONS: Expiries for Nov01 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9625(E1.2bln), $0.9700(E1.1bln), $0.9735-50(E724mln), $0.9800(E1.5bln), $0.9950(E2.0bln), $1.0000(E1.2bln)

- USD/CAD: C$1.3600($921mln)

- NZD/USD: $0.5685(N$619mln)

- AUD/NZD: N$1.1100(A$948mln), N$1.1300(A$1.3bln)

- USD/CNY: Cny7.2500($637mln)

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 01/11/2022 | 0800/0900 |  | CH | SECO Consumer Confidence | |

| 01/11/2022 | 0930/0930 | ** |  | UK | IHS Markit/CIPS Manufacturing PMI (Final) |

| 01/11/2022 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 01/11/2022 | - |  | DK | Danish General Election | |

| 01/11/2022 | - | *** |  | US | Domestic-Made Vehicle Sales |

| 01/11/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 01/11/2022 | 1345/0945 | *** | | US | IHS Markit Manufacturing Index (final) |

| 01/11/2022 | 1400/1000 | *** | | US | ISM Manufacturing Index |

| 01/11/2022 | 1400/1000 | * | | US | Construction Spending |

| 01/11/2022 | 1400/1000 | ** | | US | JOLTS jobs opening level |

| 01/11/2022 | 1400/1000 | ** | | US | JOLTS quits Rate |

| 01/11/2022 | 1530/1130 | ** | | US | US Treasury Auction Result for 52 Week Bill |

| 01/11/2022 | 2230/1830 |  | CA | BOC Governor Macklem at Senate bank committee |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.