Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- ECB FACED SIZABLE PUSH FAVORING 75 BASIS-POINT RATE INCREASE (BBG)

- ECB'S LAGARDE OFFERS BACK-TO-BACK RATE HIKES TO WOO DISSENTERS (RTRS)

- CHINA’S NDRC SAYS HARD WORK NEEDED TO ENSURE ECONOMIC RECOVERY (BBG)

- CHINA’S NEW STATE-RUN IRON ORE GIANT IS READY TO START PURCHASES (BBG)

- EU LEADERS URGE GAS PRICE CAP DEAL AS LEVEL REMAINS OPEN (BBG)

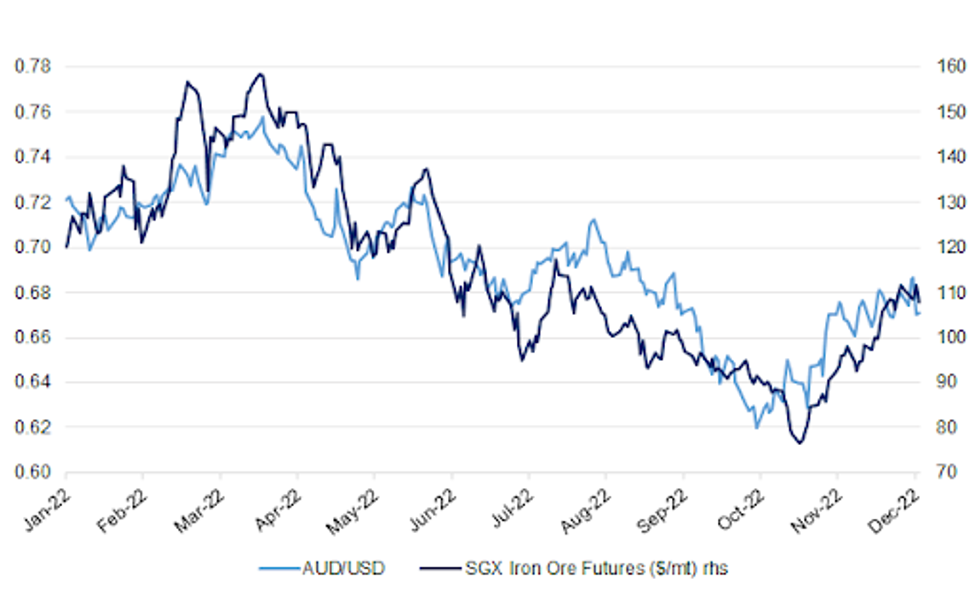

Fig. 1: AUD/USD Vs. SGX Iron Ore Futures

Source: MNI - Market News/Bloomberg

UK

ECONOMY: There will be little Christmas cheer for UK household budgets this December, as higher inflation, rising mortgage costs and soaring energy prices all weigh on sentiment, keeping consumer confidence close to the lowest levels in half a century, the head of a leading survey published Friday told MNI. (MNI)

FISCAL/POLITICS: Ministers are being urged to ask the independent pay review body to come up with fresh recommendations to resolve the NHS pay dispute. (Telegraph)

POLITICS: Labour have won the Stretford and Urmston by-election with Andrew Western holding the seat for the party with a majority of 9,906. (BBC)

EUROPE

ECB: More than a third of the European Central Bank’s policymakers favored a 75 basis-point interest-rate hike on Thursday, according to people with knowledge of the matter. (BBG)

ECB: European Central Bank President Christine Lagarde offered fellow policymakers back-to-back interest rate hikes worth 50 basis points each to secure a majority for Thursday's policy decision, four sources told Reuters. (RTRS)

ECB/ITALY: The European Central Bank’s rate hike decision is an unwelcome “present” for Italy, said Defense Minister Guido Crosetto, a close ally of Premier Giorgia Meloni. (BBG)

ECB: The European Central Bank extended existing repo and swap lines with non-euro area central banks until Jan. 15, 2024. (BBG)

SPAIN: Spanish Prime Minister Pedro Sanchez pushed through legislation to allow his two nominees to be appointed to a top court, escalating tensions with the judiciary over a long-running political impasse about the selection of judges. (BBG)

RATINGS: Sovereign rating reviews of note slated for after hours on Friday include:

- Moody’s on Luxembourg (current rating: AAA; Outlook Stable) & Slovakia (current rating: A2; Outlook Negative)

- S&P on Latvia (current rating A+; Outlook Negative)

U.S.

FISCAL: The Senate on Thursday passed the annual defense authorization bill, sending the $858 billion measure to President Biden’s desk for signature just before the year-end deadline. (The Hill)

OTHER

U.S./CHINA: The China Securities Regulatory Commission is looking forward to working with U.S. regulators to continue promoting future annual audit and supervision on companies listed in the U.S., it said on Friday. (RTRS)

U.S./CHINA: Senators in both parties Thursday pressed for more action by the Biden administration to address national security concerns raised by widespread use of TikTok a day after voting to ban the video-sharing app on government phones. (BBG)

U.S./CHINA: U.S. Treasury Secretary Janet Yellen met with China's ambassador to the United States, Qin Gang, on Thursday to discuss their "views on global macroeconomic and financial developments," the Treasury Department said in a statement. (RTRS)

JAPAN: Japan's ruling bloc agreed on Friday to raise corporate, tobacco and disaster-reconstruction income taxes by some 1 trillion yen ($7.3 billion) to double military outlay to 2% of GDP by 2027, a draft annual tax-code revision seen by Reuters showed on Friday. (RTRS)

NORTH KOREA: North Korea has tested a high-thrust solid-fuel engine that experts said would allow quicker and more mobile launch of ballistic missiles, as it seeks to develop a new strategic weapon and speeds up its nuclear and missile programmes. (RTRS)

HONG KONG: Thousands of customs, immigration and police officers will be sent to land checkpoints to manage predicted surge in traffic as the border between Hong Kong and mainland China is expected to fully reopen next month, the Post has learned. (SCMP)

BOC: The Bank of Canada is poised to say it is done hiking interest rates as the economy falls into a recession, punishing workers in a way that has been aggravated by bosses' use of Governor Tiff Macklem's bad advice to restrain pay raises, the country's top union leader told MNI. (MNI)

MEXICO: Mexico’s central bank slowed the pace of interest rate increases while saying it will continue hiking borrowing costs in early 2023 after inflation in Latin America’s second-biggest economy eased significantly last month. (BBG)

MEXICO: Just weeks before US President Joe Biden’s planned visit to Mexico, talks on the neighbors’ biggest trade dispute have stalled due to the departures of negotiators from the Latin American nation’s side and its reluctance to make concessions, according to people familiar with the matter. (BBG)

MEXICO: Mexico’s lower house approved in general terms a bill backed by President Andres Manuel Lopez Obrador that would reform parts of the electoral process. (BBG)

BRAZIL: Lower house voting on the bill requested by Lula’s transition team to pay for social aid is scheduled for Dec. 20, lower house Speaker Arthur Lira said late Thursday. (BBG)

RUSSIA: The Pentagon will expand military combat training for Ukrainian forces, using the slower winter months to instruct larger units in more complex battle skills, the Defense Department and U.S. officials said Thursday. (ABC)

RUSSIA: The US sanctioned Vladimir Potanin, Russia’s richest tycoon and the president and biggest shareholder of mining giant MMC Norilsk Nickel PJSC, but left his company untouched as it tries to maintain stability in the metals market. (BBG)

PERU: Peru congress postponed until Friday, Dec. 16, a debate on holding early presidential and legislative elections as a way out of the political crisis, it said on Twitter.(BBG)

PERU: A Peruvian judge ordered 18 months of preliminary detention for former President Pedro Castillo at a court hearing Thursday. (BBG)

METALS: China is about to upend the $160 billion iron ore trade with the biggest change in years, consolidating purchases of the raw material under a single state-owned buyer as Beijing expands efforts to increase control over the natural resources needed to feed its economy. (BBG)

METALS: Buenaventura said Peru political protests have adversely affected supply routes to mines throughout the country. (BBG)

METALS: Panama's government ordered Canada's First Quantum Minerals on Thursday to pause operations at its flagship copper mine in the country after missing a deadline to finalize a deal that would have increased payments to the government from the mine. (RTRS)

ENERGY: European Union leaders threw their weight behind a quick agreement on a natural gas price cap to put an end to months of political wrangling over an unprecedented intervention to contain the impact of an energy crisis. But they still have yet to settle on a price level. (BBG)

OIL: Russian deputy prime minister Alexander Novak said on Thursday that Russia was interested in increasing oil output as part of projects in Venezuela, the TASS news agency reported. (RTRS)

CHINA

PBOC: The 5-year Loan Prime Rate could be lowered at the December 20th fixing, according to the Securities Daily. (MNI)

ECONOMY: More hard work is needed to promote a sustained economic recovery as the external environment gets more complex and grim and global growth momentum weakens, the National Development and Reform Commission comments in a statement regarding the current economic situation. (BBG)

ECONOMY: China’s economy could remain weak until the end of Q1 next year, as disruption from Covid-reopening will suppress demand and business activity in the short term, according to the 21st Century Business Herald. (MNI)

PROPERTY: China is considering new measures to support the real estate sector, aiming to improve the balance sheets of the industry and boost market expectations and confidence, Xinhua News Agency reported late Thursday citing Vice Premier Liu He. (MNI)

CHINA MARKETS

PBOC SETS YUAN CENTRAL PARITY AT 6.9791 FRI VS 6.9343

The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 6.9791 on Friday, compared with 6.9343 set on Thursday.

PBOC NET INJECTS CNY39 BILLION VIA OMOS FRIDAY

The People's Bank of China (PBOC) on Friday injected CNY41 billion via 7-day reverse repos with the rates unchanged at 2.00%. The operation has led to a net injection of CNY39 billion after offsetting the maturity of CNY2 billion reverse repos today, according to Wind Information.

- The operation aims to keep liquidity reasonable and ample, the PBOC said on its website.

- The 7-day weighted average interbank repo rate for depository institutions (DR007) rose to 2.0000% at 9:27 am local time from the close of 1.4846% on Thursday.

- The CFETS-NEX money-market sentiment index closed at 46 on Thursday vs 45 on Wednesday.

OVERNIGHT DATA

JAPAN NOV, P JIBUN BANK MANUFACTURING PMI 48.8; OCT 49.0

JAPAN NOV, P JIBUN BANK SERVICES PMI 51.7; OCT 50.3

JAPAN NOV, P JIBUN BANK COMPOSITE PMI 50.0; OCT 48.9

The Japanese private sector economy saw a stabilisation in business activity in the final month of the year, with flash data indicating that the divergence between the manufacturing and services sectors has grown further. (S&P Global)

AUSTRALIA NOV, P JUDO BANK MANUFACTURING PMI 50.4; OCT 51.3

AUSTRALIA NOV, P JUDO BANK SERVICES PMI 46.9; OCT 47.6

AUSTRALIA NOV, P JUDO BANK COMPOSITE PMI 47.3; OCT 48.0

The Flash PMIs for December reveal a slowdown in activity across the Australian economy as we finish 2022. The service sector is clearly slowing having recorded three consecutive readings below 50 in the December quarter. The Flash Services PMI for December, at 46.9, is fast approaching levels typically associated with a contraction in economic activity. (Judo Bank)

NEW ZEALAND NOV NON-RESIDENT BOND HOLDINGS 59.7%; OCT 58.4%

NEW ZEALAND NOV BUSINESSNZ MANUFACTURING PMI 47.4; OCT 49.1

New Zealand’s manufacturing sector saw deeper levels of contraction in November, according to the latest BNZ - BusinessNZ Performance of Manufacturing Index (PMI). (BusinessNZ)

UK DEC GFK CONSUMER CONFIDENCE -42; MEDIAN -43; NOV -44

MARKETS

SNAPSHOT: ECB Sources Pick Apart Decision

Below gives key levels of markets in the second half of the Asia-Pac session:

- Nikkei 225 down 550.82 points at 27500.88

- ASX 200 down 56.082 points at 7148.7

- Shanghai Comp. down 13.099 points at 3155.549

- JGB 10-Yr future up 4 ticks at 148.04, yield down 0.4bp at 0.252%

- Aussie 10-Yr future up 0.3 ticks at 96.535, yield down 0bp at 3.455%

- U.S. 10-Yr future down 0-05 at 114-24, yield up 3.27bp at 3.4809%

- WTI crude down $0.33 at $75.78, Gold up $1.36 at $1778.25

- USD/JPY down 46 pips at Y137.32

- ECB FACED SIZABLE PUSH FAVORING 75 BASIS-POINT RATE INCREASE (BBG)

- ECB'S LAGARDE OFFERS BACK-TO-BACK RATE HIKES TO WOO DISSENTERS (RTRS)

- CHINA’S NEW STATE-RUN IRON ORE GIANT IS READY TO START PURCHASES (BBG)

- CHINA’S NDRC SAYS HARD WORK NEEDED TO ENSURE ECONOMIC RECOVERY (BBG)

- EU LEADERS URGE GAS PRICE CAP DEAL AS LEVEL REMAINS OPEN (BBG)

US TSYS: Bear Steepening As Light Cheapening Holds In Asia

TYH3 deals at 114-25+, -0-04, a little off the base of its 0-06+ range on light volume of ~57k.

- Cash Tsys bear steepened, with the major benchmarks 0.5-3.0bp cheaper into London.

- The broader Asia-Pac reaction to the hawkish guidance that accompanied the latest ECB monetary policy decision applied moderate pressure to Tsys in early trading.

- Continued concern surrounding the Chinese bond market, resulting in PBOC liquidity injections in recent days (via short- and medium-term facilities), may have helped to modestly extend the cheapening.

- The space looked through a pullback in the USD as cross-asset inputs were mixed, with e-minis little changed and the DXY down ~0.2%.

- Pre-NY we will see final Eurozone CPI readings and PMI data from Europe & the UK. Later on, San Francisco Fed President Daly will speak on inflation and the economy while NY Fed President Williams & Cleveland Fed President Mester will appear on BBG TV. We will also get flash Markit PMI data during NY hours.

JGBS: Notable Twist Steepening Into the Weekend

The early twist steepening impulse has developed further during the Tokyo afternoon.

- The bid out to 10s was perhaps aided by reports of gradual tweaks to tax settings in a bid to fund Japanese increased defense spending (slthough the space had already firmed ahead of that news), while 20+-Year paper seemed to fall afoul of ECB-related weakness as domestic participants turned their focus to next week’s BoJ meeting.

- That left futures hovering around neutral levels, operating in a narrow range, while the major cash JGB benchmarks run 1.5bp richer to 6.0bp cheaper, with a pivot around 10s.

- The swap curve has also twist steepened as the day wore on, albeit in a more muted manner than JGBs, taking cues from bonds.

- Next week’s local docket is headlined by the aforementioned BoJ monetary policy decision.

JGBS AUCTION: 3-Month Bill Auction Results

The Japanese Ministry of Finance (MOF) sells Y4.87299tn 3-Month Bills:

- Average Yield -0.1790% (prev. -0.1708%)

- Average Price 100.0481 (prev. 100.0459)

- High Yield: -0.1321% (prev. -0.1582%)

- Low Price 100.0355 (prev. 100.0425)

- % Allotted At High Yield: 80.1818% (prev. 80.0000%)

- Bid/Cover: 2.234x (prev. 3.479x)

AUSSIE BONDS: Winding Into The Weekend

Aussie bonds meandered through the final session of the week, initially showing lower as Sydney reacted to the hawkish ECB rhetoric that accompanied Thursday’s monetary policy decision, before pulling back from worst levels after both YM & XM failed to breach their overnight lows (XM didn’t get anywhere near testing post-Sydney session cheaps), with a lack of meaningful headline catalysts evident in onshore hours. That left YM +1.4 at the bell, while XM was +0.3. Cash ACGBs were flat to 4bp richer, with the 7- to 12-Year zone lagging the wider bid as 10s failed to widen further vs. their U.S. counterpart, as the 0bp zone limited the recent move in that spread.

- Bills were flat to -4 through the reds, with RBA dated OIS little changed on the day.

- The latest round of domestic flash PMI readings saw a slower rate of expansion for the manufacturing sector and a sharper rate of contraction in both the services and composite readings. Survey sponsor Judo Bank noted that "what we are seeing could be the first signs of a desired soft landing for the Australian economy in 2023.”

- Next week’s local docket thins out ahead of the Christmas break, with the minutes from the latest RBA decision and latest Westpac leading index print providing the only real points of note.

NZGBS: Modest Cheapening, Swaps Twist Steepen

Cash NZGBs finished flat to 2.5bp cheaper cross the curve, with the belly leading the weakness. Friday trade was relatively limited, with the early, modest cheapening adjustment holding.

- Swap rates were 5bp lower to 2bp higher as that curve twist steepened. 2s were unwilling to force a test of cycle highs after yesterday’s GDP-inspired shunt higher, which made for mixed direction on the curve. This came as RBNZ dated OIS pricing eased at the margin (after yesterday’s push higher), with just over 70bp of tightening now priced for the Bank’s Feb ’23 meeting alongside a terminal OCR of 5.55%, which probably aided the easing in 2-Year swap rates.

- BusinessNZ manufacturing PMI data saw a deeper move into contractionary territory, while Nov non-resident bond holding data saw the % of NZGBs held offshore move to the highest level seen since ’18.

- Next week’s local docket is busy, and somewhat front-loaded in the runup to Christmas, with the monthly ANZ business & consumer confidence readings, trade balance data, monthly credit card spending prints, PSI survey and quarterly Westpac consumer confidence data all slated.

EQUITIES: Positive China News Can't Offset Negative Global Leads

Regional equities are mostly lower, in line with weakness in major US/EU bourses through Thursday's session. Sentiment has been volatile though, particularly for HK indices. US futures tried to push higher mid-way through the session, but this move faltered, and we are now back slightly lower on opening levels.

- The HSI is close to flat at this stage, having had a 2.5% range for the session. Supports in the form of comments late yesterday from China Vice Premier Liu He that the authorities are considering new measures to boost financial conditions and confidence in the housing market have aided property shares, although we are off earlier session highs (+2.36% from earlier highs of +3.6%).

- US delisting risks for tech related names also appear to have subsided in the near term, although this was arguably already priced by the market. The HS China Enterprise Index is firmer, +0.30%, but was up as much as 1.7% earlier.

- Mainland shares are modestly lower, the CSI 300 down by 0.33% at this stage.

- Tech sensitive bourses have fallen, following the lead from major global indices. The Nikkei 225 is down by 1.9%, the Taiex -1.60%. The Kospi is down by 0.50%, although up from earlier session lows. The ASX 200 is down 0.80%.

GOLD: Stabilizes But Still Tracking Lower For The Week On Hawkish CB Rhetoric

Gold is tracking slightly above yesterday's lows, last close to $1779. This is in line with some pullback in USD sentiment, although gold's early run above $1784 quickly ran out of steam. Note the simple 200-day MA comes in at $1787, with the precious metal unable to hold gains above this resistance point through December. Near term support is evident around $1774 and beyond that around the $1766/67 region.

- The hawkish central bank tone this week, from both the Fed and ECB has weighed on gold. At this stage we are tracking 1% lower for the week.

- Gold ETF holdings have maintained a relatively flat trend this past week.

OIL: Momentum Wanes, 20-Day EMA Capping Brent Upside

Brent crude's early rally fizzled out, as we attempted a move towards $82/bbl. We last tracked close to $81/bbl, down slightly for the session. We remain above Thursday's lows, while further support should be evident ahead of $75/bbl. On the top side, resistance is evident above $83/bbl, which also coincides with the 20-day EMA ($82.87/bbl).

- Brent is still tracking higher for the week, +6.60% at this stage. Momentum has faltered though in recent sessions, likely owing to hawkish ECB rhetoric and concerns around the near term demand outlook from China.

- Still, there is a sense of underlying support from the supply side. Bloomberg reports that Russia supply to Asian markets has slowed since the introduction of the price cap, while the IEA earlier this week, stated prices should rise in 2023 on supply issues.

- Looking ahead next week sees EU energy ministers meet Monday to discuss the gas price cap level. Tuesday and Wednesday deliver the weekly US oil inventory reports.

FOREX: USD Up From Lows, A$ Underperforms On China Iron Ore News

The USD is away from lows for the session, the BBDXY index last around 1261.50, against lows near 1259. Cross asset signals have mostly supported the USD in the form of higher UST yields and lower regional equities and commodities. Still, outside of the AUD, the rest of the G10 complex is firmer against the USD.

- JPY strength has been notable for much of the session. USD/JPY sits above session lows sub 137.00, last at 137.30/35, but this is still 0.3% since the open for the yen.

- AUD/USD has underperformed, likely weighed by lower iron ore prices, after China announced a new state run buyer will launch in 2023 and that it will seek a discount from miners. The active Singapore iron ore contract is off by over 3% (last under $108/tonne). AUD/USD is back to 0.6700, versus highs for the day of 0.6736.

- NZD/USD is also away from session highs, last around 0.6350/55, but is outperforming the AUD. The AUD/NZD cross was last around 1.0545/50, with lows for day at 1.0541. The pair remains in a downtrend channel.

- Coming up is UK retail sales, along with a host of PMI print for the UK, EU and US. The Fed's Mester will do a Bloomberg TV interview., while the Fed's Daly is also scheduled to speak.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 16/12/2022 | 0700/0700 | *** |  | UK | Retail Sales |

| 16/12/2022 | 0700/0800 | ** |  | SE | Unemployment |

| 16/12/2022 | 0815/0915 | ** |  | FR | IHS Markit Services PMI (p) |

| 16/12/2022 | 0815/0915 | ** | | FR | IHS Markit Manufacturing PMI (p) |

| 16/12/2022 | 0830/0930 | ** |  | DE | IHS Markit Services PMI (p) |

| 16/12/2022 | 0830/0930 | ** | | DE | IHS Markit Manufacturing PMI (p) |

| 16/12/2022 | 0900/1000 | ** |  | EU | IHS Markit Services PMI (p) |

| 16/12/2022 | 0900/1000 | ** | | EU | IHS Markit Manufacturing PMI (p) |

| 16/12/2022 | 0900/1000 | ** | | EU | IHS Markit Composite PMI (p) |

| 16/12/2022 | 0930/0930 | *** | | UK | IHS Markit Manufacturing PMI (flash) |

| 16/12/2022 | 0930/0930 | *** | | UK | IHS Markit Services PMI (flash) |

| 16/12/2022 | 0930/0930 | *** | | UK | IHS Markit Composite PMI (flash) |

| 16/12/2022 | 1000/1100 | * | | EU | Trade Balance |

| 16/12/2022 | 1000/1100 | ** |  | IT | Italy Final HICP |

| 16/12/2022 | 1000/1100 | *** | | EU | HICP (f) |

| 16/12/2022 | 1030/1330 |  | RU | Russia Central Bank Key Rate Decision | |

| 16/12/2022 | - |  | US | 'Continuing Resolution On US Government Funding Expires | |

| 16/12/2022 | - | | UK | BOE Announce Q1 Active Gilt Sales Schedule | |

| 16/12/2022 | 1445/0945 | *** | | US | IHS Markit Manufacturing Index (flash) |

| 16/12/2022 | 1445/0945 | *** | | US | IHS Markit Services Index (flash) |

| 16/12/2022 | 1700/1200 | | US | San Francisco Fed's Mary Daly |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.