Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SOUTH KOREA

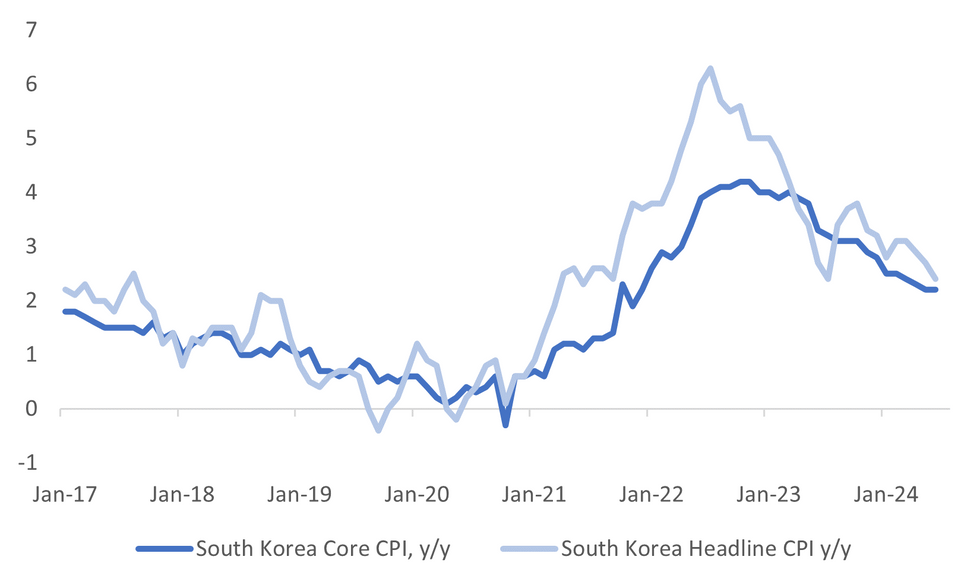

South Korea June CPI was below expectations. The m/m print fell 0.2%, against a +0.1% expectation, which was also the same as the prior outcome. As a result, the headline y/y print was also below forecasts, coming in at 2.4% y/y (2.6% forecast and 2.7% prior0. The core, ex food and energy, measure rose 2.2% y/y in line with the prior outcome and market forecasts. The chart below plots the headline and core CPI trends in y/y terms.

- In terms of the detail we had 5 out of 12 sub indices record m/m falls. The largest came from food, -1.0% (now down in m/m terms for 3 straight months). Transport fell 1.5%, while health and recreation fell modestly. Restaurants (+0.3% m/m) and the other category (+0.4%m/m) were the main positives.

- In y/y terms 8 out of the 12 sub indices saw either lower momentum compared with May or the same. Despite m/m falls, food and transport still have the highest y/y pace (after the other category).

- Today's result brings headline closer towards the 2% BoK target. This adds to the case for the BoK easing at some stage in H2 of this year, although next week's meeting is likely to see an unchanged outcome.

Fig 1: South Korea CPI Y/Y Trends

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok