Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- BAILEY SAYS ‘LAST MILE’ OF UK’s INFLATION FIGHT WILL TAKE TIME- BBG

- MORE OCR HIKES POSSIBLE - EX-RBNZ GOVERNOR - MNI

- RBA FORECASTS GDP SLOWDOWN - MNI BRIEF

- CHINA SCRAPS AUSTRALIAN BARLEY TARIFFS IN PLACE SINCE 2020 - BBG

- CHINA INPUT PRICES UP JUNE/JULY PERIOD - NBS, MNI BRIEF

- CHINA CENTRAL BANK PLEDGES STRONGER POLICY SUPPORT FOR ECONOMY - BBG

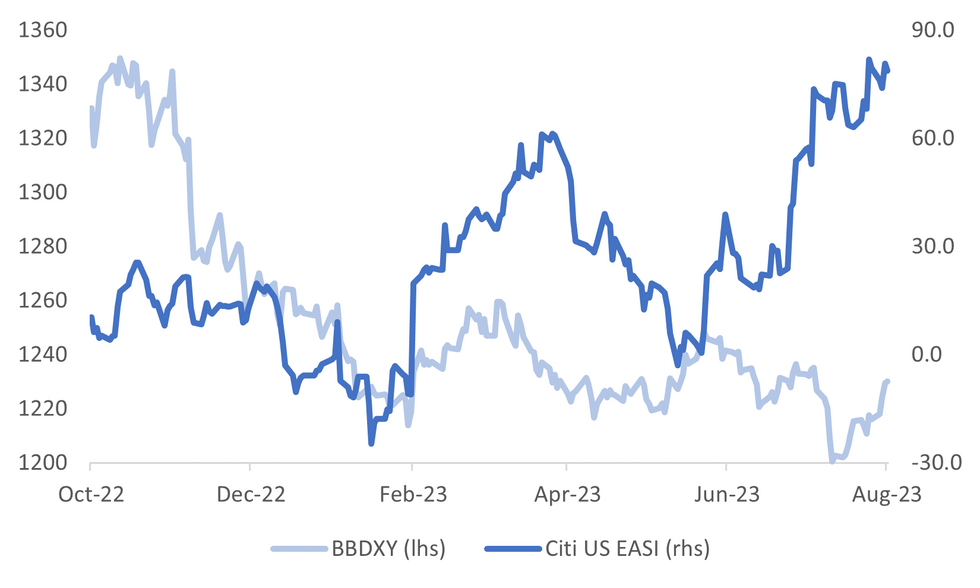

Fig. 1: BBDXY & US Citi Economic Surprise Index

Source: Citi/MNI - Market News/Bloomberg

U.K.

BOE: Bank of England Governor Andrew Bailey said it is too soon for the UK to declare victory in the battle against inflation and that the “last mile” will require a prolonged period of restrictive interest rates. “It’s the last mile which obviously is where policy is really doing the work, and we’re going to have to see policy stay restrictive,” he said Thursday in an interview with Bloomberg TV. “It’s going to have to remain restrictive to have this effect of bringing inflation down, and particularly next year.” (BBG)

EUROPE.

RUSSIA: Russian social media users reported hearing explosions and gunfire near the Russian Black Sea port of Novorossiysk on Friday morning. Videos posted on a local online community and circulated by Russian online news outlet Astra showed the movement of ships just off the coast with the sound of gunfire coming from the direction of the sea. (RTRS)

U.S.

EQUITIES: Amazon.com Inc. Chief Executive Officer Andy Jassy pulled off a financial double play this earnings season: generating strong revenue growth in the core e-commerce business while cutting the pace of spending. Wall Street applauded, sending the shares up about 10% in extended trading. (BBG)

US/CHINA: The chairman of the House Select Committee on the Chinese Communist Party is calling on President Joe Biden to include stocks and bonds in his upcoming executive order aiming at restricting US investments in China. (BBG)

POLITICS: Donald Trump pleaded not guilty to charges that he conspired to obstruct the 2020 presidential election and interfere with the voting rights of millions of Americans — a case his legal team said it was prepared to “vigorously” defend. (BBG)

OTHER

JAPAN: Bond traders are on guard for a further five-basis-points increase in benchmark Japanese bond yields amid speculation that it would trigger another foray into the market by the central bank. The yield on 10-year government notes has already climbed about 20 basis points to a nine-year high of 0.655% since July 27, the day before the Bank of Japan adjusted policy to allow the rate to increase to as high as 1%. The moves come amid upward pressure on rates globally, with long-term US yields surging to their highest since November as the Treasury market comes close to erasing this year’s gains. (BBG)

NEW ZEALAND: Persistently strong employment may force the Reserve Bank of New Zealand to raise the Official Cash Rate further despite its signaling to the contrary, a former RBNZ governor told MNI. While Don Brash, governor between 1988-2002, said the monetary policy committee (MPC) would rather avoid further rate hikes ahead of the Oct. 14 general election, he saw more tightening as being likely. (MNI)

AUSTRALIA: The Reserve Bank of Australia forecasts near-term GDP growth to slump – growing just 0.9% y/y in Dec. 2023, down from the previous 1.2% forecasts and the current 2.3% rate, according to the Statement on Monetary Policy released today. (MNI)

AUSTRALIA/CHINA: China will scrap anti-dumping and anti-subsidy tariffs on Australian barley, effective from Aug. 5, China’s commerce ministry said in a statement, in the latest sign of improving ties between the two countries. (BBG)

AUSTRALIA: Australia's competition regulator on Friday blocked a A$4.9 billion ($3.2 billion) buyout planned by No.4 bank ANZ Group of insurer Suncorp's banking arm, setting the scene for a drawn-out legal challenge. The Australian Competition and Consumer Commission (ACCC) said it was concerned a tie-up between the financial firms would worsen competition and "further entrench an oligopoly market structure" where four lenders including ANZ have three quarters of the country's A$2 trillion in home loans. (RTRS)

COMMODITIES: Iron ore climbed on more visible signs that China’s authorities are stepping up property-boosting measures that may lift steel consumption, while steel stockpiles fell. The steelmaking staple surged as much as 3.4%, the most in three weeks, before paring gains. Beijing’s latest efforts to bolster the property market include a pledge from the central bank to increase funding support to the private sector, while at least one Chinese city has encouraged banks to cut existing mortgage rates and down-payment ratios. (BBG)

PHILIPPINES: Bangko Sentral ng Pilipinas says it is ready to adjust monetary policy, if needed, in view of the “persistent” risks to inflation outlook. “The balance of risks to the inflation outlook continues to lean towards the upside,” BSP says in a statement, citing potential impact of transport fare hikes, minimum wage adjustments, food supply constraints, El Niño. (BBG)

CHINA

PRICES: China saw price increases in 39 out of 50 key production inputs over the mid-June to late July period, according to the National Bureau of Statistics on Friday. The economy experienced price decreases in seven inputs with four remaining flat. Buyers saw prices rises in key inputs such as steel rebar (1.8%), copper (0.3%) and coking coal (6.9%), which were partially offset by falls in prices for Liquefied natural gas (-3.3%). (MNI)

LOCAL GOVERNMENT DEBT: China is expected to speed up roll-out of a plan to resolve its local government debt risks, with measures including debt swap, extension and restructuring, China Securities Journal says in a front-page report Friday, citing experts. (CSJ)

POLICY: China will announce more tax break extensions soon focusing on tech, innovation, key industrial chain in order to expand consumption, Ministry of Finance official Wei Yan says at a briefing. China’s small enterprises and individual business owners still face difficulties. (BBG)

PBOC: PBOC will support banks to reasonably manage and control liability costs and enhance financial support for the real economy, the central bank’s head of the monetary policy department Zou Lan says at a briefing. PBOC will make timely and appropriate counter-cyclical adjustments based on the economic situation. (BBG)

PBOC: The People's Bank of China will strengthen coordination between financial, fiscal and industrial policies, and will guide more financial resources into the private economy, said PBOC Governor Pan Gongsheng at a symposium with heads of private enterprises and financial institutions on Thursday. Pan said the scale of instruments to support private enterprises in debt financing will be expanded. (MNI)

POLICY RATES: China will likely cut interest rates and increase sales of central government bonds in H2 to boost the economy, but it must remain vigilant against breaching risk regulatory principles and the legal framework, said Xiaojing Zhang, dean at the Institute of Economics of the Chinese Academy of Social Sciences. There is a great chance for rate cuts, including adjustments to rates of outstanding loans, said Zhang. (21st Century Business Herald)

MARKETS: China Securities Depository and Clearing (CSDC) plans to reduce the minimum settlement reserve fund payment ratio for stock-related businesses further to an average of about 13% from the 16% noted since October 2023. This could release over CNY30 billion funds to the market. It will encourage faster completion of fund settlements, further improve the efficiency of fund use by securities companies and fund managers, reduce market costs, and boost confidence. (Quanshang China)

CHINA MARKETS

PBOC Net Drains CNY63 Bln Via OMOs Friday

The People's Bank of China (PBOC) conducted CNY2 billion via 7-day reverse repos on Friday with the rate unchanged at 1.90%. The operation has led to a net drain of CNY63 billion after offsetting the maturity of CNY65 billion reverse repo today, according to Wind Information.

- The operation aims to keep banking system liquidity reasonable and ample, the PBOC said on its website.

- The 7-day weighted average interbank repo rate for depository institutions (DR007) rose to 1.6423% at 10:00 am local time from the close of 1.6182% on Thursday.

- The CFETS-NEX money-market sentiment index closed at 46 on Thursday, compared with the close of 35 on Wednesday.

PBOC Yuan Parity At 7.1418 Friday Vs 7.1495 Thursday

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1418 on Friday, compared with 7.1495 set on Thursday. The fixing was estimated at 7.1797 by BBG survey today.

MARKETS

US TSYS: Curve Marginally Flatter In Asia

TYU3 deals at 110-09+, +0-02, a 0-06 range has been observed on volume of 72k.

- Cash tsys sits 2bps cheaper to 2bps richer across the major benchmarks, the curve has twist flattened pivoting on 7s.

- Tsys firmed off session lows as risk sentiment improved in Asia, regional equities followed US equity futures higher after Amazon rose ~10% in post market trade. However there was little follow through on the move and tsys ticked away from session highs dealing in narrow ranges for the remainder of Friday's Asian session.

- Earlier, tsys had ticked lower in early dealing despite the absence of any macro headline driver. Pressure in ACGBs, ahead of the RBA's SoMP, perhaps weighed on the wider space.

- FOMC dated OIS remain stable, a terminal rate of 5.40% is seen in November with ~60bps of cuts by June 2024.

- There is a thin docket in Europe today. Further out we have the July NFP report which headlines Friday's session, the MNI preview is here.

JGBS: Futures Slide Back Into Negative Territory

JGB futures have slid back into negative territory, -6 compared to settlement levels, in the Tokyo afternoon session. The session range has been relatively narrow today ahead of US payrolls later today.

- There have been no economic releases today.

- (Bloomberg) “A rise to 0.7% is possible and the BoJ may continue to slow the pace of yield gains if it reaches that level too soon,” said Hideo Shimomura, senior portfolio manager at Fivestar Asset Management Co. in Tokyo. “The BoJ doesn’t want a sharp, one-way move close to 1%. Operations so far have seen more ‘smoothing’ actions rather than efforts to stop gains. They may tighten their grip more if the 10-year yield rises near 0.8%”. (See link)

- Cash JGBs are flat to 4.7bp cheaper (30-year zone) across the curve. The benchmark 10-year yield is unchanged at 0.653%, above BoJ's YCC old limit of 0.50% but below its new hard limit of 1.0%.

- The swaps curve has twist steepened, pivoting at the 7-year, with rates 0.1bp lower to 2.9bp higher (30-year). Swap spreads are tighter out to the 5-year and mixed beyond.

- On Monday, the local calendar sees the release the BoJ Summary of Opinions for the July MPM along with the Leading and Coincident Indices for June (preliminary).

AUSSIE BONDS: Cheaper After RBA Forecast Update, Eyeing US Tsys Ahead Of Payrolls

ACGBs (YM -8.0 & XM -8.0) are 1-3bp cheaper after the RBA released updated forecasts in the latest Statement on Monetary Policy (SoMP). The forecasts show inflation returning to within its 2-3% target band at the end of 2025. In May, the RBA predicted inflation will hit 3% by mid-2025 but that has now edged up to 3.1%.

- Cash ACGBs are 7-8bp cheaper on the day with the AU-US 10-year yield differential +5bp at +1bp.

- Swap rates are 4-5bp higher on the day with EFPs tighter.

- The bills strip has bear flattened with pricing flat to -7.

- RBA-dated OIS pricing is 1-3bp firmer across meetings after the SoMP release.

- (AFR) China has agreed to lift tariffs on imports of Australian barley from Saturday in a key concession to more than $20 billion worth of sanctions on exports imposed at the height of political tensions between Canberra and Beijing.

- On Monday the local calendar sees ANZ-Indeed Job Ads. It is worth noting that NSW has a bank holiday on Monday.

- Later today sees the release of US Non-Farm Payrolls, with +200k consensus versus +209k prior. (See MNI NFP Preview here)

- The AOFM announced plans to sell A$700mn of the 2.75% 21 June 2035 bond on Wednesday, 9 August 2023.

NZGBS: Weaker, Outperforms ACGBs, Awaits US Payrolls Data

NZGBs closed 5-7bp weaker but off session cheaps. Without a domestic catalyst, local participants have likely sought direction from US tsys ahead of non-farm payrolls. NZ/US 10-year yield differential closed unchanged on the day. NZGBs did however outperform ACGBs with the 10-year yield differential 3bp tighter at +64bp.

- US tsys have twist flattened, pivoting at the 7-year, in Asia-Pac trade with rates +2bp to -2bp.

- Swap rates closed 6bp higher.

- RBNZ-dated OIS pricing closed little changed across meetings with terminal rate expectations at 5.65%.

- The local calendar has no economic data on Monday. The next key release is Retail Card Spending for July on Wednesday.

- Later today sees the release of US Non-Farm Payrolls, with +200k expected versus +209k prior. The unemployment rate is forecast to remain unchanged at 3.6%. AHE is seen moderating to 0.3% m/m, although it doesn’t take much from an unrounded 0.36% m/m. No change is expected in average hours worked. (See MNI NFP Preview here)

FOREX: Greenback Marginally Pressured, NFP In View

The greenback is marginally pressured in the Asian session on Friday, higher US equity futures and firmer regional equities have seen risk sentiment firm and the USD tick marginally lower.

- The AUD is the strongest performer in the G-10 space at the margins. AUD/USD sits at $0.6570/75, ~0.3% higher. China scrapped tariffs on Australian barley facilitating a brief extension of gains before ticking away from session highs. Resistance is at $0.6630, the high from Aug 2, support comes in at $0.6514 (Aug 3 low).

- Kiwi is ~0.2% firmer, NZD/USD sits at $0.6090/95. The pair has not yet been able to breach the $0.61 handle as it consolidates early gains on Friday.

- Yen is a touch firmer however USD/JPY has observed narrow ranges for the most part of today's session.

- Elsewhere in G-10 GBP is ~0.2% firmer and EUR is up ~0.1%.

- Cross asset wise; US equity futures are firmer after Amazon gained 10% in post market trade following a bullish revenue forecast. E-minis are up ~0.3% and NASDAQ futures are up ~0.5%. The Hang Seng is up ~1%. BBDXY is down ~0.1% and the US Tsy curve is marginally flatter.

- The highlight of today's session is the July NFP print, the MNI preview is here.

EQUITIES: US Futures Tracking Higher, China/HK Markets Firm

A number of the major regional indices have tracked higher today, btu gains aren't strong, as the market awaits the NFP outcome later in the US. US equity futures are higher, buoyed by strength in Amazon in after-hours trading. The company presented a better-than-expected earnings backdrop. Eminis were last around 4537, +0.34%, with the active contract unable to sustain moves above 4540. Nasdaq futures are slightly firmer, last +0.49%.

- The other focus point has been HK/China shares, which opened strongly but now sit away from session highs. At the break, the HSI is up 0.99%. The CSI 300 is up 0.64%, the Shanghai Composite +0.47%.

- Early sentiment was buoyed by reports from late yesterday of the PBoC meeting with property developers and pledging to support finance to the private sector. The CSI 300 real estate index is around flat at this stage, but was 2.17% higher in Thursday trade.

- Officials from the PBoC, NDRC and MOF have spoken again today. Tax breaks for small businesses is being proposed, while the PBoC will utilize its full policy suite to ensure stable credit supply for the economy.

- Elsewhere, Japan stocks are a touch higher, the Topix last +0.25%. Tech sensitive plays like South Korea (Kospi flat) and Taiwan (Taiex -0.20%) have struggled though. Global tech indices have been under pressure in recent sessions maid the resurgent US yield backdrop. Offshore investors have also sold close to $1bn South Korean shares this week.

- In SEA, trends are mixed. Indian shares have opened higher, tracking +0.40% firmer at this stage.

OIL: Aiming For A 6th Straight Week Of Gains

Brent crude has largely tracked sideways in Friday trade to date. We were last near $85.25/bbl, against an earlier high of $85.60/bbl and low of $85.06/bbl. This keeps us comfortably in ranges seen this past week. At this stage we are tracking modestly higher for the week (~0.30%), which if maintained would be the 6th straight week of positive gains. WTI is near $81.75/bbl currently, but sits comfortably above closing levels from the end of last week (+1.45% at this stage).

- For Brent, bulls will target mid April highs around $87.50/bbl. Support was evident yesterday on the pull back to $82.50, which also coincides with the 200-day EMA.

- Thursday's rebound was driven by Saudi Arabia announcing it will extend its 1mbpd voluntary production cut until end-September, while leaving the door open to “extend” and/or “deepen” them. Following this announcement, Russia’s Novak has said Russia will cut oil exports by 300kbpd in September, down from a voluntary cut commitment of 500kbpd in August.

- These developments are likely to overshadow the OPEC+ meeting later, which is due to “assess market conditions” in an online meeting Friday 2pm Vienna time.

- The other focus point will be the NFP report from a broader macro standpoint.

- Russia reported today the Novorossiysk Port halted traffic after a Ukrainian drone attack. However, oil loadings for moored tankers continues and there hasn't been any reported damage to key infrastructure.

GOLD: Heading For The Worst Week In Six

Gold is +0.1% in the Asia-Pac session, after closing little changed at 1934.06 on Thursday. The day low was $1929.65. The precious metal experienced conflicting influences, with a softer USD index providing support, while a significant bear steepening in the Treasury curve posed challenges.

- The rise in longer-term global bond yields was the significant development observed on Thursday. Yields for the 10-year US Treasury benchmark and beyond were 10-12bp higher. The 10-year finished at 4.17%, the highest level since Nov’22. The US Treasury yield curve steepened for the eighth straight day. 10-year EGBs also rose around 10bp. JGB futures were slightly cheaper after 10-year JGBs were pressured on Thursday, taking its yield to 0.653%.

- Bullion is on track for its worst week in six, primarily due to the surge in US bond yields, which came in response to signs of unexpected economic strength in the nation and concerns about its widening budget deficit.

- According to the MNI technicals team, support remains at $1924.5 (Jul 11 low) after which lies $1902.8 (Jul 6 low).

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 04/08/2023 | 0600/0800 | ** |  | DE | Manufacturing Orders |

| 04/08/2023 | 0645/0845 | * |  | FR | Industrial Production |

| 04/08/2023 | 0700/0900 | ** |  | ES | Industrial Production |

| 04/08/2023 | 0730/0930 | ** |  | EU | IHS Markit Final Eurozone Construction PMI |

| 04/08/2023 | 0800/1000 | * |  | IT | Industrial Production |

| 04/08/2023 | 0830/0930 | ** |  | UK | IHS Markit/CIPS Construction PMI |

| 04/08/2023 | 0900/1100 | ** | | EU | Retail Sales |

| 04/08/2023 | 1115/1215 | | UK | BOE Pill and Shortall speak at MPR National Agency briefing | |

| 04/08/2023 | 1230/0830 | *** |  | CA | Labour Force Survey |

| 04/08/2023 | 1230/0830 | *** |  | US | Employment Report |

| 04/08/2023 | 1400/1000 | * | | CA | Ivey PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.