Source: MNI - Market News/Bloomberg

UK

UK/EUR Relations: (BBG): “The European Union proposed allowing London to continue clearing the bloc’s trades until 2028, a departure from its previous vow that the post-Brexit arrangement would end this summer. A spokesperson for the European Commission, the EU’s executive arm, said it would consult with member states on extending the transition period for three years, until the end of June 2028”.

EU

EU Rates: (BBG): “ECB Should Wait ‘a Bit’ With Next Rate Cut. It would be better for the European Central Bank “to wait a bit more” before lowering interest rates again, Governing Council member Robert Holzmann tells Kronen Zeitung in an interview.”

EU DEFENSE SPENDING: (BBG): “EU Must Arm Itself to ‘Survive’ in Uncertain World, Tusk Says. The European Union must arm itself to “survive” in an increasingly uncertain global order, Polish Prime Minister Donald Tusk said on Wednesday, calling on the bloc’s member states to boost spending on defense. “If Europe wants to survive, it has to be armed,” Tusk told a session of the European Parliament in Strasbourg, France. Poland holds the EU’s six-month rotating presidency through June, during which its top priority is to shore up the 27-nation bloc’s security, he said. “

US

US/MIDDLE EAST: (BBG) :”President Donald Trump signed an order on Wednesday that again would categorize the Houthi militant group in Yemen as a terrorist organization — nearly four years after the Biden administration revoked the designation. Since then, the Houthis, who are aligned with Iran, have engaged in a lengthy campaign of missile and drone attacks on cargo ships and other vessels sailing in the Red Sea and Gulf of Aden. The attacks started after the Hamas assault on Israel and the war in Gaza began.”

US/CHINA: (BBG): “President Donald Trump downplayed the national security risk posed by TikTok in an interview with Fox News on Wednesday, days after offering the social video app a reprieve from legislation that would have forced it to shut down. “Is it that important for China to be spying on young people, on young kids, watching crazy videos?” Trump said. Trump suggested all electronic products manufactured in China could carry a spying risk, adding that TikTok’s was not the most serious of them.”

OTHER

SOUTH KOREA: (BBG): “South Korea’s economy continued to splutter last quarter, after President Yoon Suk Yeol’s short-lived declaration of martial law battered consumer confidence at a time when export growth is slowing. Gross domestic product grew 0.1% in the three months through December from the previous quarter, the Bank of Korea said Thursday. That figure missed economists’ forecast of a 0.2% expansion. From a year earlier, the economy gained 1.2%, less than a projection of 1.4%.”

NEW ZEALAND : (BBG): “New Zealand plans to establish a one-stop shop to bolster foreign direct investment and drive faster economic growth. Invest New Zealand will streamline its process and provide tailored support to foreign investors, Prime Minister Christopher Luxon said Thursday in his State of the Nation address in Auckland. It will operate within the existing New Zealand Trade and Enterprise agency before transitioning into a separate Crown entity.”

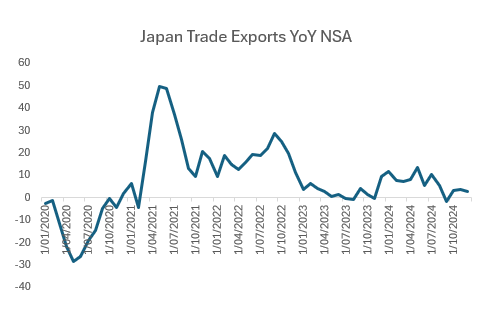

JAPAN EXPORTS: (BBG): “Japan’s exports rose for a third month in December on the back of a weaker yen, as businesses waited for further clarity on likely US trade policy in President Donald Trump’s second term. "

CHINA

CHINA STOCKS: (MNI BRIEF): China To Attract Long-term Funds For Stock Market. China will steadily increase the proportion of A-share investment by medium-and long-term funds by setting an investment ratio and extending the assessment period, Wu Qing, chairman of the China Securities Regulatory Commission told reporters on Thursday.

CHINA STOCKS: (MNI BRIEF) : CSRC To Promote Investment Value Of A-shares. China’s top securities watchdog said it will increase policy support to promote the quality and investment value of listed companies and strengthen regulations to improve the capital market ecosystem.

CHINA/US: (MNI BRIEF): US Firms In China Less Optimistic For 2025. US firms in China are less confident in the country's market growth and more pessimistic on U.S.-China relations this year, an American Chamber of Commerce in China survey showed on Thursday.

CHINA MARKETS

MNI: PBOC Net Injects CNY139.5 Bln via OMO Thursday.

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY480 billion via 14-day reverse repos, with the rate unchanged at 1.65%. The operation led to a net injection of CNY139.5 billion after offsetting the maturity of CNY340.5 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) rose to 1.8850% at 09:32 am local time from the close of 1.8721% on Wednesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 68 on Wednesday, compared with the close of 45 on Tuesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.1708 Thurs; -1.14% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1708 on Thursday, compared with 7.1696 set on Wednesday. The fixing was estimated at 7.2845 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND FIVE-MONTH BUDGET DEFICIT NZ$3.93B

NEW ZEALAND ANNUAL NET IMMIGRATION SLOWS TO 30,592

SOUTH KOREA JAN COMPOSITE BUSINESS SURVEY MANUFACTURING 89.0; PRIO 87.1.

SOUTH KOREA JAN COMPOSITE BUSINESS SURVEY NON-MANUFACTURING 83.6; PRIOR 87.5

SOUTH KOREA GDP YOY 4Q +1.2%; PRIOR +1.5%

SOUTH KOREA SA QoQ 4Q +0.1%; PRIOR +0.1%.

SOUTH KOREA GDP ANNUAL YOY +2.0%; PRIOR +1.4%

JAPAN TRADE BALANCE DEC: Y130.9bn; PRIOR Y110.3bn.

JAPAN TRADE BALANCE ADJUSTED DEC: Y33.0bn; PRIOR Y388.7bn.

JAPAN EXPORTS YoY DEC +2.8%; PRIOR +3.8%.

JAPAN IMPORTS YoY DEC +1.8%; PRIOR -3.8%.

MARKETS

US TSYS: Tsys Futures Trade In Narrow Ranges, Volumes Well Below Averages

- There has been very little to mention in tsys futures today, ranges have been very tight, while volumes are well below recent averages. TU is +00⅜ at 102-22¾, while TY is -00+ 108-17+. There has been no notable tsys flow trades.

- Looking at technical levels in the TY contract, The medium-term trend remains bearish and the recovery that started Jan 13, appears to be a correction. The contract has traded through the 20-day EMA, at 108-17+. This exposes 109-06, the Dec 31 high, and 109-16+, the 50-day EMA. A clear break of the 50-day EMA is required to strengthen a bullish theme. The bear trigger is unchanged at 107-06, the Jan 13 low.

- Cash tsys curve is slightly steeper today, with yields 0.5bps to 1bps lower. The 2yr is -0.8bps at 4.289%, while 10yr is -0.8bps at 4.603%. The 2s10s curve is unchanged at 31bps, after hitting lows of 28.5bps overnight.

- There was little to note from the Trump interview, with part 2 of the interviewing airing at the same time tomorrow on Fox, which will likely focus on foreign policy.

- Cash tsys curve is slightly steeper today, with yields 0.5bps to 1bps lower. The 2yr is -0.8bps at 4.289%, while TY is -0.6bps at 4.605%. The 2s10s curve is unchanged at 31bps, after hitting lows of 28.5bps overnight.

- Projected rate cuts through mid-2025 running largely steady vs. Wednesday's levels (*) as follows: Jan'25 at -0.1bp, Mar'25 at -6.4bp, May'25 at -11.9bp (-12.4bp), Jun'25 at -22.5bp (-22.7bp), Jul'25 steady at -26.6bp.

- Later today we have Jobless claims & Kansas City Fed Manf. Activity.

AUSSIE BONDS: Flat, Subdued Data-Light Session, Jun-31 Supply Tomorrow

ACGBs (YM flat & XM -0.5) are little changed after a subdued session of trading.

- The local calendar has been empty today.

- Cash US tsys are flat to 1bp richer in today’s Asia-Pac session after yesterday’s modest losses.

- Cash ACGBs are flat to 1bp cheaper with the AU-US 10-year yield differential at -14bps.

- Swap rates are 1bp higher.

- The bills strip is -1 to -2 across contracts.

- Given the very high correlations between NZ and Australian CPIs and their major components, there is information to be gained about the upcoming Q4 Australian data on January 29 from NZ’s Q4 data.

- Given government electricity subsidies, it is difficult to compare the headline measures. However, the NZ data suggest there will be a further moderation in Australia’s trimmed mean inflation but possible upside risks to services, which is a particular focus of the RBA.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut is more than fully priced for April (110%), with the probability of a February cut at 71% (based on an effective cash rate of 4.34%).

- Tomorrow, the local calendar will see S&P Global PMI(P) for January.

- The AOFM plans to sell A$700mn of the 1.50% 21 June 2031 bond tomorrow.

BONDS: NZGBS: Closed At Session Bests After Paring Early Weakness

NZGBs closed at session bests, little changed on the day across benchmarks.

- Outside of the previously outlined Five-Month Budget Deficit and Net Migration, there hasn't been much by way of domestic drivers to flag.

- Today’s NZGB supply saw strong demand metrics, with cover ratios ranging between 2.94x to 3.93x.

- Invest NZ will streamline its process and provide tailored support to foreign investors, Prime Minister Christopher Luxon in his State of the Nation address in Auckland.

- Swap rates closed flat to 1bp higher.

- RBNZ dated OIS pricing is flat to 2bps firmer across meetings today but remains flat to 3bps softer than yesterday’s pre-Q4 CPI levels.

- BNZ believes that the data won’t change the central bank’s view as it also didn’t alter its own view of 50bp of easing in February. It sees a greater chance of 25bp than 75bp. BNZ also believes that the pace of easing will moderate to 25bp from April as inflation surprises to the upside.

- Tomorrow, the local calendar is empty, with the next release being Filled Jobs data on Tuesday.

ASIA STOCKS: China & Hong Kong Equities Giving Back Earlier Gains

Chinese and Hong Kong markets opened higher today, driven by optimism over new measures to stabilize the stock market, however those gains are quickly being erased now with the CSI 300 Index up 0.90% now after earlier being up 1.50%, while China Enterprise Index up just 0.35% after earlier being up 1.6%. The gains come after Beijing announced initiatives such as boosting pension fund investments in listed companies and requiring mutual funds to increase onshore stock holdings by 10% annually for three years.

- China’s securities regulator announced a plan to guide more insurance funds into equities and expand the scale of equity funds to boost the stock market. The initiative aims to attract medium- and long-term capital by encouraging large state-owned insurers to increase A-share investments and raising the equity proportion in the National Social Security Fund and corporate annuities. Regulators will also enhance the investment ecosystem by promoting share buybacks and allowing multiple dividend distributions annually.

- China's property de-stocking initiative has gained traction, with December 2024 seeing slight price recoveries in first- and second-tier cities due to favorable policies, active second-hand home markets, and strong land auction results. Analysts emphasize balancing inventory reduction with optimizing new supply, such as repurposing old properties, to ensure market stability. Property benchmarks are under-performing today with Mainland Property Index -0.30%, HS Property Index -0.50%, while the BBG China Property Gauge is +0.10%

- Despite this optimism, concerns persist over China's sluggish economic recovery, the ongoing property slump, and potential tariffs from the U.S. Investors are closely monitoring consumption-related stocks ahead of the Lunar New Year holidays, with hopes that increased spending will support sectors like airlines, hospitality, and entertainment.

ASIA STOCKS: Equities Mostly Higher, Further China Support, BoJ Tomorrow

Asian stocks advanced for the fourth consecutive day, driven by gains in China as government measures to encourage long-term institutional investments supported sentiment. The MSCI Asia Pacific Index is 0.2% higher, marking its longest winning streak since December. Chinese equities outperformed, with the CSI 300 Index rising 0.6% and Hong Kong's Hang Seng China Enterprises Index gaining 0.5%. Easing US-China tensions and optimism around AI investments further lifted market sentiment.

- Japan’s Topix and Nikkei indices rose 0.5% and 0.7%, respectively, with Mitsubishi Heavy Industries gaining on AI-related demand expectations.

- In contrast, South Korea’s Kospi fell 0.6%, dragged by a 4.7% drop in SK Hynix due to underwhelming results, Australia’s ASX 200 Index also fell 0.6%, while New Zealand’s NZX 50 rose 0.2%.

- There was very little to note from the Trump interview on Fox earlier today, the 2nd part of the interview will air tomorrow at the same time which is likely to be more focused on Foreign Policy.

- US equity futures have trading in a narrow range during the Asian session today, giving back just a bit of the overnight gains. The NASDAQ is -0.20%, although was up 1.3% overnight, while S&P 500 Eminis are trading -0.10%.

- Investors are closely monitoring China’s consumer sector ahead of the Lunar New Year and waiting for the Bank of Japan’s rate decision on Friday. Meanwhile, global markets remained calm, with the 10-year US Treasury yield and Bloomberg Dollar Index showing little movement.

FOREX: FX Trends Little Changed, Markets Awaiting Tariff News

Aggregate G10 FX moves have been negligible in the first part of Thursday trade. The USD BBDXY index sits unchanged in latest dealings, holding just under 1304.

- There was focus on a Fox News interview with President Trump, but this was largely focused on domestic issues. Trump defended TikTok during the interview, but broader sentiment didn't shift. part 2 of the interviews late US time on Thursday (so Friday time for Asia Pac markets), where foreign policy and China relations are expected to be in greater focus. For FX markets the tariff issue remains a central watch point.

- US equity futures sit modestly lower, but this follows recent strong cash gains. Most regional Asia Pac markets are higher (except for South Korea). China markets have recovered as further supports were unveiled by policy makers, but we sit off best levels. US yields are down a touch, but losses are not much beyond 1bps at this stage.

- USD/JPY is holding close to 156.55/60 in latest dealings, little changed for the session. Earlier lows were at 156.29. Export growth was slightly better than forecast but still sub other NEA economies. The trade position also improved.

- AUD and NZD are little changed. AUD/USD last 0.6275, NZD/USD around 0.5665/70.

- Looking ahead, we get French manufacturing sentiment, along with EU consumer confidence. Canada retail sales and US initial jobless claims are also out.

Gold Steadies, Watching Tariff Headlines.

- The ever-evolving story of the new US President’s plans for tariffs has given gold a boost, enjoying its safe-haven status amid the uncertainty.

- Having initially indicated that tariffs were not on the immediate agenda for China, Trump performed an about face and to add to the impending tariffs for Mexico and Canada, China and the European Union are now in his sights.

- Tariffs can be inflationary and when paired with the potential tax cuts he has indicated, this has the potential to abruptly alter the course for Fed policy this year.

- Gold hit new highs overnight reaching US$2,763.48 before backing off to open in Asia at $2,756.17 before heading marginally lower to $2,753.04.

- The driving force behind gold’s advance in 2024 was the potential for interest rate cuts whereas going forward this may be overtaken by safe-haven status.

OIL: Crude Continues Trending Lower To Be Down Almost 3% This Week

Oil has continued to trend lower during APAC trading today as the market worries about the impact a trade war would have on demand. There is also likely to be an increase in US output. Brent is down 0.3% to $78.73/bbl, close to the intraday low, and WTI 0.4% lower at $75.17/bbl just above support at $75.05 (Wednesday’s low). The USD index is flat.

- The first part of US President Trump’s Fox interview focused on domestic issues with the second part due to air later today to be about foreign policy.

- Tightened sanctions on Russian crude has increased its shipping costs and boosted demand for oil from other suppliers especially Middle Eastern, thus pushing up prices from that region. As a result, some Asian refineries are looking to reduce output due to narrower margins.

- EIA US inventory data print later. Bloomberg reported earlier that there was a US crude inventory build of 1mn barrels last week, according to people familiar with the API data. Products also continued to rise with gasoline up 3.2mn and distillate 1.9mn. There could be a number of weeks of higher inventories as both Canadian producers and US refiners sharply front load supplies ahead of threatened 25% tariffs from February 1.

- Later US jobless claims, January Kansas Fed manufacturing, Canadian November retail sales and preliminary January euro area consumer confidence print.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 23/01/2025 | 0745/0845 | ** | Manufacturing Sentiment | |

| 23/01/2025 | 0900/1000 | *** | Norges Bank Rate Decision | |

| 23/01/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 23/01/2025 | 1100/0600 | *** | Turkey Benchmark Rate | |

| 23/01/2025 | 1100/1100 | ** | CBI Industrial Trends | |

| 23/01/2025 | 1330/0830 | ** | Retail Trade | |

| 23/01/2025 | 1330/0830 | *** | Jobless Claims | |

| 23/01/2025 | 1330/0830 | ** | Retail Trade | |

| 23/01/2025 | 1500/1600 | ** | Consumer Confidence Indicator (p) | |

| 23/01/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 23/01/2025 | 1600/1100 | ** | DOE Weekly Crude Oil Stocks | |

| 23/01/2025 | 1600/1100 | ** | Kansas City Fed Manufacturing Index | |

| 23/01/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 23/01/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 23/01/2025 | 1800/1300 | ** | US Treasury Auction Result for TIPS 10 Year Note | |

| 24/01/2025 | 2200/0900 | *** | Judo Bank Flash Australia PMI | |

| 24/01/2025 | 2330/0830 | *** | CPI | |

| 24/01/2025 | 0001/0001 | ** | Gfk Monthly Consumer Confidence | |

| 24/01/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI | |

| 24/01/2025 | 0300/1200 | *** | BOJ Policy Rate Announcement | |

| 24/01/2025 | 0700/0800 | ** | PPI | |

| 24/01/2025 | 0700/0800 | ** | Unemployment | |

| 24/01/2025 | 0800/0900 | ** | PPI | |

| 24/01/2025 | 0815/0915 | ** | S&P Global Services PMI (p) | |

| 24/01/2025 | 0815/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 24/01/2025 | 0830/0930 | ** | S&P Global Services PMI (p) | |

| 24/01/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 24/01/2025 | 0900/1000 | ** | S&P Global Services PMI (p) | |

| 24/01/2025 | 0900/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 24/01/2025 | 0900/1000 | ** | S&P Global Composite PMI (p) | |

| 24/01/2025 | 0930/0930 | *** | S&P Global Manufacturing PMI flash | |

| 24/01/2025 | 0930/0930 | *** | S&P Global Services PMI flash | |

| 24/01/2025 | 0930/0930 | *** | S&P Global Composite PMI flash | |

| 24/01/2025 | 1000/1100 | ECB's Lagarde in dialogue on the global economic outlook | ||

| 24/01/2025 | 1100/1100 | ** | CBI Distributive Trades | |

| 24/01/2025 | 1100/1200 | ECB's Cipollone in panel discussion on the effects of CB digital currencies |