Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- REPUBLICAN AND DEMOCRAT NEGOTIATORS ARE MOVING CLOSER TO A DEAL ON THE DEBT CEILING - BBG

- MOODY’S SAYS A MID-JUNE PAYMENT OF INTEREST WILL BE CRITICAL FOR US TO MAINTAIN AAA RATING - BBG

- CLEARING HOUSES ARE WORKING OUT HOW TO USE US TREASURY BILLS AND BONDS USED AS COLLATERAL AS A DEFAULT LOOMS - RTRS

- PERSISTENT INFLATION HAS HELPED PUSH GERMANY INTO RECESSION - BBC

- CHINA'S CENTRAL BANK WILL LIKELY CUT THE RESERVE REQUIREMENT FOR MAJOR BANKS EARLIER THAN EXPECTED - BBG

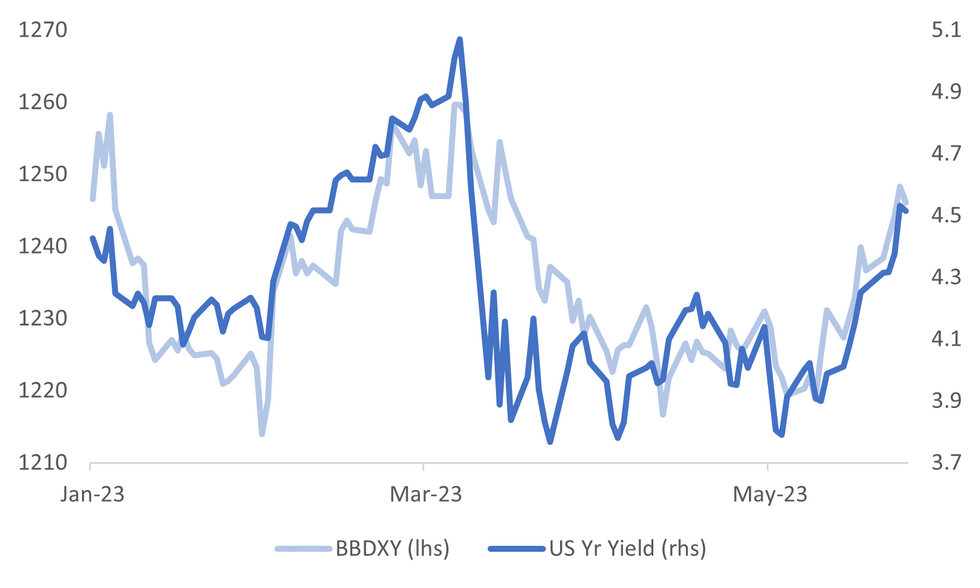

Fig. 1: US Yields & Dollar Indices A Touch Down From Recent Highs

Source: MNI - Market News/Bloomberg

U.K.

MORTGAGE RATES: Britain's biggest building society has said it will increase some of its mortgage rates from Friday due to the current economic outlook. Nationwide said rates on new fixed deals will rise by up to 0.45 percentage points. It comes amid expectations the Bank of England will have to raise interest rates higher than previously thought. (BBC)

INVESTMENT: The UK is set to win a battle with Spain to host a multi-billion-pound electric car battery plant in Somerset, the BBC understands. The boss of Jaguar Land Rover-owner Tata is expected to fly to London next week to finalise the deal. Some in the car industry have described the plant as the most significant investment in UK automotive since Nissan came to Britain in the 1980s. (BBC)

DOWNING ST: London police have said they have arrested a man after a car crashed into the gates of Downing St, the road that’s home to the UK PM Sunak. (BBG)

VOTING: More than 13,000 people were denied a vote in English local elections this month because of the government's new identification law, with those in poorer areas most impacted, according to a Reuters survey of local authorities. (RTRS)

EUROPE

GERMANY: Persistent inflation has helped push Germany into recession in the first three months of the year, an upgrade to growth data shows. Europe's largest economy was also badly affected when Russian gas supplies dried up after the invasion of Ukraine, analysts said. The economy contracted by 0.3% between January and March, the statistics office said. (BBC)

CREDIT SUISSE: UBS and the Swiss government haven't reached a consensus on the precise terms of a state guarantee, which may delay the close of its takeover of Credit Suisse (BBG)

INVESTMENT: The EU is cautious about imposing controls on investments into China despite encouragement from the US. EU Trade Ministers discussed their misgivings about the plan which could pose a risk to European security. (BBG)

U.S.

DEBT CEILING: Republican and White House negotiators are moving closer to an agreement to raise the debt limit and cap federal spending for two years, according to people familiar with the matter. (BBG)

DEBT CEILING: With investor attention on the US sovereign credit rating rising as the federal government gets ever closer to running out of cash Moodys says that a mid June payment of interest will be critical for maintaining the top AAA grade. (BBG)

DEBT CEILING: Republican debt-limit negotiators are setting aside demands for large increases in defense spending and instead settling for a smaller increase people familiar with talks said (BBG)

DEBT CEILING: Noble Prize winning economist Paul Krugman played down concerns over the US governments debt ahead of a potential default and said budget negotiators risk undermining the nations future prosperity by focusing their efforts on spending cuts (BBG)

DEFAULT FEARS: Clearing houses and their members are working out how to treat certain U.S. Treasury bills and bonds commonly used as collateral, as the United States nears a deadline that could see it default on its debt, according to four industry sources. (RTRS)

NVIDIA: Nvidia Corp surged 24% on Thursday in one of the largest one-day gains in value for a U.S. stock, after its stellar revenue forecast showed that Wall Street has yet to price in the game-changing potential of AI. (RTRS)

POLITICS: Florida Governor Ron DeSantis' fledgling presidential campaign was looking to push forward on Thursday after a troubled online launch event drew mockery from his rivals and renewed doubts about his viability as a national candidate. (RTRS)

OTHER

JAPAN: Japan will place additional sanctions on Russia after the Group of Seven (G7) summit the country hosted last week agreed to step up measures to punish Moscow's invasion of Ukraine, Chief Cabinet Secretary Hirokazu Matsuno said on Friday. (RTRS)

JAPAN: Core consumer inflation in Japan's capital slowed in May, but a key index stripping away the effect of fuel hit a four-decade high, underscoring broadening price pressure that may keep alive expectations of a withdrawal of ultra-loose monetary policy. (RTRS)

AUSTRALIA: Retail Sales in Australia stalled as consumers felt the impact of inflation and rising interest rates (BBG)

RBNZ: A cyclone that devastated large parts of New Zealand's North Island has proven to be less inflationary than first feared. The RBNZ downgraded its impact to just 0.1% on CPI from 0.3%. (BBG)

NEW ZEALAND: Consumer confidence fell flat in May, with Kiwis still wary about the economy according to ANZ. The ANZ-Roy Morgan Consumer Confidence Index in May was at 79.2 per cent compared with 79.3 per cent last month while more Kiwis believe inflation pressures will ease in the next two years easing from 5.2 per cent in April to 4.8 per cent this month. (NZ Herald)

TRADE: U.S. Commerce Secretary Gina Raimondo and Chinese Commerce Minister Wang Wentao traded barbs on trade, investment and export policies in talks on Thursday described by Raimondo's office as "candid and substantive." (RTRS)

SOUTH KOREA: South Koreas Hyundai and LG Energy Solutions will invest 5.7tn won to produce electric-car batteries in the US to comply with the US’s clean energy tax law. (BBG)

TAIWAN: The government will offer new insight on the economic impact of slowing global demand for electronics when it releases its latest estimate for 2023 gross domestic product on Friday. (BBG)

CHINA

ECONOMY: Chinas central bank will likely cut the reserve requirement ratio for major banks earlier than expected as economic recovery loses steam. (BBG)

POWER SUPPLY: Local governments have taken various measures to increase power supply as peak electricity consumption arrives earlier than usual amid continued economic recovery and hot weather (BBG)

LOANS: Chinese financial institutions should be alert to the risk of companies investing bank loans with low interest rates in higher-yielding wealth management products instead of putting them to use in the real economy (CSJ)

INFRASTRUCTURE SPENDING: CSJ urges More Funding Tools for Infrastructure Spending. China is expected to step up the use of “quasi-fiscal” tools - usually financing from state policy banks - to help stabilize infrastructure investment and economic growth in the second half of this year (CSJ) https://blinks.bloomberg.com/news/stories/RV8N86T0G1KW

CHINA MARKETS

PBOC Net Injects CNY3 Bln Via OMOs Fri

The People's Bank of China (PBOC) conducted CNY5 billion via 7-day reverse repos on Friday, with the rates unchanged at 2.00%. The operation has led to a net injection of CNY3 billion after offsetting the maturity of CNY2 billion reverse repo today, according to Wind Information.

- The operation aims to keep banking system liquidity reasonable and ample, the PBOC said on its website.

- The 7-day weighted average interbank repo rate for depository institutions (DR007) rose to 2.0087% at 09:23 am local time from the close of 1.9235% on Thursday.

- The CFETS-NEX money-market sentiment index closed at 48 on Thursday, lower than the close of 50 on Wednesday

PBOC SETS YUAN CENTRAL PARITY RATE AT 7.0760 FRI VS 7.0529 THURS

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.0760 on Friday, compared with 7.0529 set on Thursday

OVERNIGHT DATA

NEW ZEALAND MAY ANZ CONSUMER CONFIDENCE 79.2; PRIOR 79.3

JAPAN MAY TOKYO CPI Y/Y 3.2%; PRIOR 3.5%

JAPAN MAY TOKYO CPI EX-FRESH FOOD Y/Y 3.2%; PRIOR 3.5%

JAPAN MAY TOKYO CPI EX-FRESH FOOD, ENERGY Y/Y 3.9%; PRIOR 3.8%

MARKETS

US TSYS: Marginally Richer In Asia

TYM3 deals at 112-21, +0-01, a 0-05+ range has been observed on volume of ~76k.

- Cash tsys sit 1-2bps richer across the major benchmarks, the curve has bull steepened.

- Tsys were pressured in early dealing as concerns over the US Debt Ceiling impasse weighed. House Speaker McCarthy noted that this is no agreement on the US Debt Ceiling. TY dealt below Thursdays lows, however the move did not follow through.

- A recovery off session lows was seen as the USD retreated off best levels and e-minis pared early losses.

- Tsys held richer for the remainder of the Asian session however ranges remained narrow and moves had little follow through..

- In Europe today we have UK Retail Sales, further out US Consumer income, Wholesale Inventories, Durable Goods and UofMich Consumer Sentiment crosses.

JGBS: Futures Reverse Morning Weakness in Afternoon Trade, 40-Year Outperforms

JGB futures strengthen in the afternoon session, unwinding morning weakness, to be -5 compared to the settlement levels.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Tokyo CPI and PPI Services data.

- Local market participants seemed content to track US tsys in anticipation of the release of April US PCE deflator data later in the day. US tsys were 1-2bp richer in Asia-Pac trade.

- Cash JGBs are little changed out to the 10-year zone, but richer beyond. The benchmark 10-year yield is 0.1bp higher at 0.427%, below the morning session high of 0.454%. The 40-year has reversed morning underperformance to be the star performer in the afternoon session. The yield is 2.2bp lower at 1.450% after hitting a morning high of 1.509%.

- Swap rates are trading mixed with the curve exhibiting a flattening bias. Swap spreads are generally narrower out to the 30-year zone and wider beyond.

- The local calendar next week sees Leading and Coincident Indicators (Mar F) on Monday, Jobless Rate (Apr) on Tuesday, Retail Sales (Apr), IP (Apr P) and Housing Starts (Apr) on Wednesday, and Capital Spending (Q1) and Company Profits (Q1) on Thursday.

- The next week also has slated BoJ Rinban operation covering 3-25-year+ JGBs (Mon) along with 2-year (Tue) and 10-year (Thu) supply.

AUSSIE BONDS: Cheaper, Narrow Range, Awaits US PCE Deflator

ACGBs are weaker (YM -5.0 & XM -4.0) although holding above session lows. ACGBs traded within a relatively narrow range in the Sydney session with no significant domestic catalysts.

- Local market participants seemed content to adopt a wait-and-see approach in anticipation of the release of April US PCE deflator data later in the day. According to BBG consensus, the core PCE deflator is expected to show a monthly increase of 0.3% and a year-on-year figure of 4.6%, remaining unchanged from March.

- US tsys were 1-2bp richer in Asia-Pac trade.

- Cash ACGBs are 4bp cheaper with the AU-US 10-year yield differential -1bp at -6bp.

- Swap rates are 3-4bp higher with EFPs slightly tighter.

- The bills strip is steeper with pricing flat to -7.

- RBA dated OIS is little changed across meetings.

- The RBA has reiterated that it will consider later this year whether there is a case for selling Commonwealth government bonds off its balance sheet once banks have repaid the first tranche of the circa A$190bn they borrowed from RBA during the pandemic (AFR).

- The local calendar next week sees Building Approvals (Apr) on Tuesday, Construction Work Done (Q1), Private Sector Credit (Apr) and CPI Monthly (Apr) on Wednesday, Capex (Q1) on Thursday and Home Loan data (Apr) on Friday.

NZGBS: Continue To Outperform in the $-Bloc

NZGBs closed 3-4bp cheaper after trading in a relatively narrow range. Without domestic drivers, local participants appear to have been happy to sit on the sidelines ahead of April US PCE deflator data later today. BBG consensus expects the core PCE deflator to print 0.3% m/m 4.6% y/y unchanged from March.

- NZGBs have continued their outperformance in the $-Bloc since the RBZ decision with NZ/US and NZ/AU 10-year yield differentials 3bp and 2bp respectively lower.

- Swap rates are 2-4bp higher with the implied long-end swap spread wider.

- RBNZ dated OIS closed with pricing 1-4bp firmer for meetings beyond August.

- RBNZ Silk said the impact of cyclone Gabrielle has been less inflationary than first feared. The Reserve Bank had initially estimated that Cyclone Gabrielle would add 0.3ppt to inflation in both the first and second quarters but has since downgraded that impact to just 0.1ppt. (link)

- ANZ consumer confidence index fell to 79.2 in May from 79.3 in April. Inflation expectations eased to 4.8% from 5.2%.

- The local calendar next week sees Building Permits (Apr) on Monday, ANZ Business Confidence (May) and CoreLogic House Prices (May) on Wednesday and Terms of Trade (Q1) on Friday.

FOREX: Greenback Marginally Pressured In Asia

The USD is a touch lower in Asia on Friday, the Antipodeans were pressured in early dealing however losses were pared. AUD and NZD sit a touch firmer. Early in the session House Speaker McCarthy noted that this is no agreement on the US Debt Ceiling. He also said he will stay at the Capitol and continue working until a deal is done.

- Yen is ~0.2% firmer, USD/JPY deals below the ¥140 handle however we remain well within recent ranges. Tokyo Headline and Core CPI were a touch below estimates.

- Kiwi is marginally firmer, NZD/USD was down as much as ~0.3% in early trade as e-minis extended losses and RBNZ's Silk noted that rates need to stay on hold for an extended period and that the bank is wary of over tightening. Support was seen ahead of year to date lows and losses were pared.

- AUD/USD is ~0.1% firmer, the pair dealt below the $0.65 printing a low of $0.6491 before paring losses to sit a touch firmer at $0.6510/15.

- Elsewhere in G-10 SEK is ~0.2% firmer, however liquidity is generally poor in Asia. EUR and GBP are both up 0.1%.

- Cross asset wise; e-minis are 0.1% softer however they were down as much as 0.3% in early trade. BBDXY is down ~0.2% and US Treasury Yields are softer across the curve.

- In Europe today we have UK Retail Sales, further out US Consumer income, Wholesale Inventories, Durable Goods and UofMich Consumer Sentiment crosses.

EQUITIES: Tech Still Outperforming, Mixed Trends Elsewhere

Regional equity sentiment is mixed in Asia Pac for the final trading session of the week. Hong Kong markets have been closed today, which has lightened liquidity for the region. Tech related plays are outperforming modestly, while China and parts of SEA remain weaker.

- US futures are in the red, albeit with losses not extending beyond -0.30% for Eminis. The index was last at 4152, down by -0.2%, with Nasdaq futures off by a similar amount. Headlines from US House Majority Leader McCarthy that there is no agreement on the debt ceiling weighed at the margins in early trade. Negotiations are likely to continue into the weekend.

- In Taiwan, the Taiex is the outperformer, up over 1%, with positive Chip/Tech sentiment from Thursday trade in the US aiding moves. This is fresh highs for the index back to early June last year.

- The Kospi is also up but a more modest 0.15%, although offshore investors have bought another $487.7mn in local locals, brining week to date inflows to $881.6mn.

- China markets are weaker to the break, the CSI 300 off a further 0.40%. We are up from fresh lows though.

- In SEA, Philippines stocks are down around 0.80%, while Thai stocks are -0.40% at this stage, unwinding gains from earlier in the week.

OIL: Brent Close To Flat For The Week On Mixed OPEC Views

Brent crude is modestly lower versus NY closing levels from Thursday. We were last close to $76/bbl. This is well below highs for the week above $78.50/bbl, but we haven't tested Thursday session lows near $75/bbl so far today. WTI was last under $72/bbl, following a similar trajectory.

- Brent is barely in positive territory for the week, as the market continues to digest conflicting signals from OPEC+ members. Russia's Deputy Premier stating the group was unlikely to adjust production targets in June (next meeting is next weekend June 3-4). This contrasted with earlier comments from the Saudi Arabia Energy Minister, which stated speculators should 'watch out'.

- Speculation around the meeting outcome is likely to dominate market sentiment over the coming week.

- For Brent, a break sub $75/bbl would open up a move to the May 15 low around $73.50/bbl. On the topside, the 20-day simple MA comes in close to $79/bbl.

GOLD: Touched Two-Month Low, 6% From Peak

Gold is firmer at 1948.74 (+0.4%) in the Asia-Pacific session, after closing 0.8% lower on Thursday at 1941.41, a two-month low.

- Gold is on track for its largest weekly decline, currently standing at 1.5%, in nearly four months. This decline comes as indications of resilience in the US economy raise the likelihood of the Federal Reserve continuing its rate hikes. The US GDP saw a slight upward revision for Q1, reaching an annualized rate of 1.3%. Additionally, the core PCE deflator was revised upward by 0.1% to a 5.0% annual rate for Q1.

- Traders have now fully factored in another 25bp hike by July. Higher interest rates traditionally having a negative impact on gold, which does not offer interest-bearing returns. As a result, the metal has experienced a decline of approximately 6% since its peak in early May, largely driven by speculation surrounding interest rates.

- However, the ongoing impasse concerning the US debt-ceiling is providing some support to the haven asset.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 26/05/2023 | 0600/0700 | *** |  | UK | Retail Sales |

| 26/05/2023 | 0600/0800 | ** |  | SE | Retail Sales |

| 26/05/2023 | 0600/0800 | ** | | SE | PPI |

| 26/05/2023 | 0645/0845 | ** |  | FR | Consumer Sentiment |

| 26/05/2023 | 0740/0940 |  | EU | ECB Lane Panels Dubrovnik Econ Conference | |

| 26/05/2023 | 0800/1000 | ** |  | IT | ISTAT Business Confidence |

| 26/05/2023 | 0800/1000 | ** | | IT | ISTAT Consumer Confidence |

| 26/05/2023 | 1230/0830 | ** |  | US | Durable Goods New Orders |

| 26/05/2023 | 1230/0830 | ** | | US | Personal Income and Consumption |

| 26/05/2023 | 1230/0830 | ** | | US | Advance Trade, Advance Business Inventories |

| 26/05/2023 | 1400/1000 | *** | | US | Final Michigan Sentiment Index |

| 26/05/2023 | 1500/1100 |  | CA | Finance Dept monthly Fiscal Monitor (expected) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.