Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- US TREASURY CUTS JAN-MAR BORROWING ESTIMATE BY $55B - MNI BRIEF

- US VOWS 'ALL NECESSARY ACTIONS' AFTER DRONE STRIKE, QATAR FEARS IMPACT ON GAZA HOSTAGE TALKS - RTRS

- JAPAN PM KEEPS UP PUSH FOR HIGHER WAGES AS ELECTION TALKS SWIRLS - BBG

- AUSTRALIAN RETAIL SALES SHIFT INTO REVERSE IN DECEMBER - RTRS

- RBNZ HAS WAY TO GO TO GET INFLATION TO 2%, CHIEF ECONOMIST - BBG

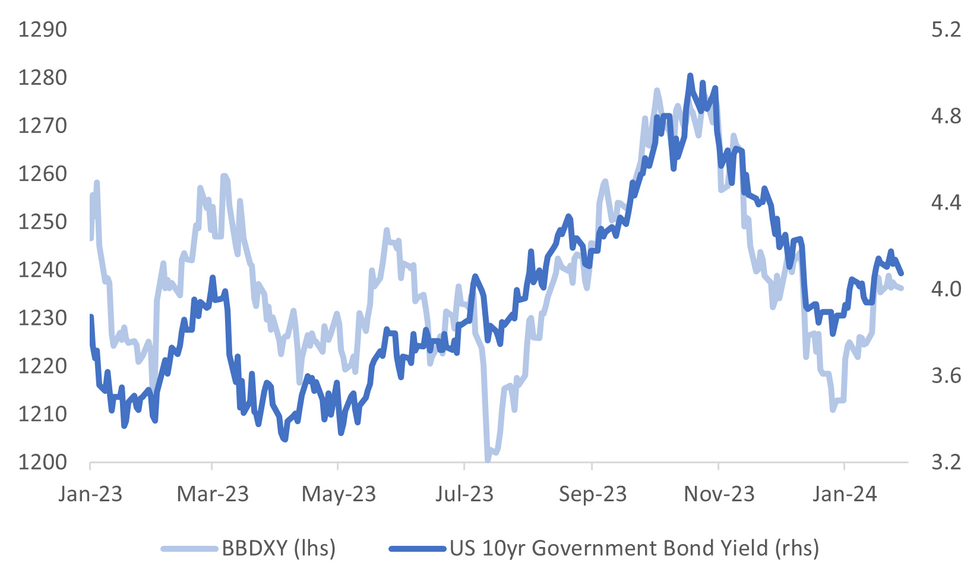

Fig. 1: US 10yr Yield Versus BBDXY USD Index

Source: MNI - Market News/Bloomberg

U.K.

INFLATION (BBG): Inflation in UK stores fell to the lowest level in more than 18 months in another sign that the cost-of-living crisis is starting to ease. Shop prices were 2.9% higher year-on-year in January compared with a 4.3% annual increase in December, the British Retail Consortium said Tuesday. That’s the lowest since May 2022 as retailers offered heavy discounts to attract shoppers.

EUROPE

ECB (BBG): The European Central Bank won’t rush into cutting interest rates to avoid undoing progress on inflation, according to Governing Council member Peter Kazimir, who said June is more likely than April for a first move.

BANKS (MNI BRIEF): European banks are going to see a deterioration in the quality of their assets as Stage 2 delinquencies have increased “significantly in recent months,” European Central Bank’s Vice President Luis de Guindos said Monday.

SPAIN (MNI BRIEF): The impact on inflation from taffic disruptions in the Red Sea “would, for now, be very small,” the Bank of Spain wrote in its latest blog published Monday, noting that the situation must be closely monitored due to the high levels of uncertainty.

FRANCE (BBG): Emmanuel Macron stepped up his opposition to a trade deal between the European Union and the South American Mercosur bloc as he is faced at home with farmer protests sparked in part by foreign competition.

U.S.

FISCAL (MNI BRIEF): The U.S. Treasury Department said on Monday it expects to borrow USD760 billion in the first quarter, USD55 billion less than forecast in October, largely due to higher net fiscal flows and a higher cash balance at the beginning of the quarter.

FED (MNI): The Federal Reserve’s framework review that begins later this year is likely to yield modest but significant changes to the existing average-inflation targeting regime, putting more emphasis on the need to respond to inflation when it is too high as well as when it is too low, nearly a dozen former Fed officials and senior staffers told MNI in a series of interviews.

FED (BBG): Senator Elizabeth Warren and three Democratic colleagues urged Federal Reserve Chair Jerome Powell to lower interest rates to help bring down housing costs ahead of the central bank’s policy meeting this week.

OTHER

MIDEAST (RTRS): The United States vowed to take "all necessary actions" to defend American forces after a drone attack killed three U.S. troops in Jordan, while Qatar said it hoped U.S. retaliation would not damage regional security or undercut progress toward a new Gaza hostage-release deal.

VENEZUELA (BBG): The Biden administration will restore sanctions on Venezuela’s energy sector if the country upholds its ban on an opposition candidate from running for president, two US officials said, a move that risks chilling recent efforts to improve ties between the two adversaries.

NORWAY (BBG): Norway’s $1.5 trillion wealth fund added to its bets in the biggest technology companies last year after interest in artificial intelligence drove a surge in the sector.

JAPAN (BBG): Japanese Prime Minister Fumio Kishida is pressing forward with his campaign for higher wages as his slumping support rate levels out and speculation re-emerges that he could opt to call a general election this year.

AUSTRALIA (RTRS): Australian retail sales flipped into reverse in December as shoppers restrained themselves after a big splurge the month before, while annual growth in spending slowed to lows last seen during the COVID-19 pandemic lockdowns.

NEW ZEALAND (BBG): New Zealand needs more time to get inflation back into the central bank’s 1-3% target band even though the economy is weaker than expected, Reserve Bank Chief Economist Paul Conway said. The currency gained.

NEW ZEALAND (BBG): ANZ forecasts the RBNZ will start cutting interest rates from August but doesn’t rule out the chance of a rate hike next month, following comments from the central bank’s chief economist.

HONG KONG (RTRS): Hong Kong's leader confirmed on Tuesday his intention to pass fresh national security laws soon to build on sweeping legislation Beijing imposed on the city in 2020, saying the city has the constitutional responsibility to impose the new laws.

NORTH KOREA (RTRS): North Korea fired multiple unidentified cruise missiles on Tuesday into the sea off its west coast, South Korea's military said, the third time Pyongyang has tested cruise missiles in less than a week.

CHINA

PBOC (SHANGHAI SECURITIES NEWS): The People’s Bank of China will continue with large-scale injections via reverse repos to offset the liquidity gap due to increasing demand for cross-month capital and cash withdrawals before the Chinese New Year, Shanghai Securities News reported citing analysts.

EVERGRANDE (YICAI): The Hong Kong judge's decision to liquidate China Evergrande will not directly impact the group’s domestic business, according to Li Shuguang, professor at China University of Political Science and Law. Li noted each company in the group would remain an independent legal entity, as China Evergrande was an overseas holding platform company.

YIELDS (BBG): China’s benchmark government bond yield fell to its lowest in nearly 22 years on mounting expectations for further monetary easing amid a fragile economic recovery and stock-market selloff.

REAL ESTATE (BBG): China’s top economic official called on city authorities to follow through on measures compiled by national policymakers aimed at easing the nation’s property market downturn.

CHINA MARKETS

MNI: PBOC Injects Net CNY98 Bln Via OMO Tues; Rates Unchanged

The People's Bank of China (PBOC) conducted CNY563 billion via 7-day reverse repo on Tuesday, with the rates unchanged at 1.80%. The reverse repo operation has led to a net injection of CNY98 billion reverse repos after offsetting CNY465 billion maturity today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.8383% at 09:52 am local time from the close of 1.9401% on Monday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 43 on Monday, compared with the close of 44 on Friday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

PBOC Yuan Parity Lower At 7.1097 Monday vs 7.1047 Friday

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1055 on Tuesday, compared with 7.1097 set on Monday. The fixing was estimated at 7.1739 by Bloomberg survey today.

MARKET DATA

JAPAN DEC JOBLESS RATE 2.4%; MEDIAN 2.5%; PRIOR 2.5%

JAPAN DEC JOB-TO-APPLICANT RATIO 1.27; MEDIAN 1.28; PRIOR 1.28

AUSTRALIA DEC RETAIL SALES M/M -2.7%; MEDIAN 1.7%; PRIOR 1.6%

SOUTH KOREA DEC RETAIL SALES Y/Y 7.5%; PRIOR 8.7%

UK BRC SHOP PRICE INDEX Y/Y 2.9%; PRIOR 4.3%

MARKETS

US TSYS: Yields Lower, Market Awaits Response On Troop Attack

TYH4 is trading at 111-24, + 07+ from NY closing levels.- Tsy futures remained rangebound most of the day, before breaking the overnight highs of 111-23 and is currently holding above it. Technical resistance at 112-01+ (High Jan 17).

- Cash yields have seen the curve move lower today trading in a 1-3bps range, the 2Y now trading 0.6bp lower, while the 10Y is currently 2.3bps lower.

- News flow has been reasonably light so far today, with markets waiting for the US response following the attack on its troops stationed in Jordan over the weekend.

- Data Tonight: House Price Index, Consumer Confidence, Job Openings

JGBS: Futures Stronger, Sitting Mid-Range, US JOLTS Data Later Today

In the afternoon session, JGB futures are holding in positive and in the middle of the session’s range, +15 compared to settlement levels.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined somewhat mixed December jobs data.

- Cash JGBs have ground out a slight bull-flattening of the curve in the afternoon session, with yields flat to 1.4bps lower. The benchmark 10-year yield is 0.8bp lower at 0.715% versus the Nov-Dec rally low of 0.555%.

- The 2-year is unchanged after today’s supply. The 2-year auction demonstrated mixed demand metrics, as the low price failed to meet dealer expectations but the cover ratio increased to 3.742x from 3.340x in December. It was the highest cover ratio for a 2-year auction since July last year. The auction tail was also shortened.

- Unlike recent JGB auctions, today’s result appears to indicate that the current outright yield adequately accounts for uncertainties surrounding the BoJ policy outcome.

- Swap rates are flat to slightly lower, with swap spreads mixed.

- Tomorrow, the local calendar sees Retail Sales and Industrial Production data for December, along with the BoJ Summary of Opinions (Jan. MPM).

- Attention turns to US JOLTS job openings data later today.

AUSSIE BONDS: Futures Richer But Off Post-Retail Sales Highs, Q4 CPI Tomorrow

ACGBs (YM +3.0 & XM +6.5) sit stronger but below session highs sparked by the release of weaker-than-expected December Retail Sales data. The move away from the session’s best levels likely reflected the fact that at least a part of December’s weakness was related to shifting spending patterns between December and November.

- Notably, afternoon weakness in ACGBs comes despite an extension of yesterday’s US tsys rally in today’s Asia-Pac session. Cash US tsys are currently dealing flat to 3bps richer, with a flattening bias.

- Cash ACGBs are 3-6bps richer on the day, with the AU-US 10-year yield differential 1bp wider at +10bps.

- Swap rates are 1-5bps lower, with the 3s10s curve flatter.

- The bills strip is dealing mixed, with pricing -1 to +2.

- RBA-dated OIS pricing is little changed across meetings. A cumulative 44bps of easing is priced by year-end.

- Tomorrow, the local calendar sees Q4 CPI print. This will be a crucial input into deliberations at next week's RBA meeting. Bloomberg consensus is expecting headline CPI to print +0.8% q/q and 4.3% y/y versus +1.2% and 5.4% prior. Trimmed Mean CPI is expected to show +0.9% q/q and 4.3% y/y versus +1.2% and 5.2% prior.

- Tomorrow, the AOFM plans to sell A$800mn of 3.75% 21 May 2034 bond.

NZGBS: Richer, Closed Mid-Range, Hawkish Comments From Officials

NZGBs closed flat to 4bps richer, with the 2/10 curve flatter.

- Bloomberg reported that NZ Finister Minister Willis responds to questions in parliament stating that annual inflation of 4.7% in Q4 is an improvement but “is still far too high”. She added that on tradables inflation has stayed stubbornly high indicating domestic factors rather than global factors are playing the greatest role in driving inflation.

- (Bloomberg) ANZ forecasts the RBNZ will start cutting interest rates from August but doesn’t rule out the chance of a rate hike next month, following comments from the central bank’s chief economist today.

- ICYMI, RBNZ Chief Economist Conway said in a speech today in Wellington that “we still have a way to go to get inflation back to the target midpoint.”

- Swap rates closed 1bp higher to 3bps lower, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed flat to 3bps firmer across meetings, with July-August leading. A cumulative 92bps of easing is priced by year-end.

- Tomorrow, the local calendar sees ANZ Business Confidence. Australia sees the release of Q4 CPI data.

FOREX: Dollar Up From Earlier Lows, NZD Marginally Outperforms On Hawkish RBNZ Comments

The BBDXY sits up from earlier lows, last close to 1235.8, down only slightly for the session. We have seen generally tight ranges for most pairs in the G10 space, albeit with modest NZD outperformance.

- In early trade, NZD spiked on hawkish comments from RBNZ Chief Economist Conway. Notably he noted Q4 non-tradables was stronger than they expected and that there is still some way to go to achieve the inflation target.

- NZD/USD got to 0.6144 on the initial move higher, before pulling back to 0.6125/30. This afternoon we have pushed higher though, back to 0.6140/45. The 20 and 50-day EMAs sit slightly higher, rough 0.6150/60, which may be in focus on further upside in the pair.

- USD/JPY dipped to 147.20, sub Monday lows, before support emerged. The pair was last near 147.35, slightly firmer in yen terms for the session. Dec jobless data was mixed, with the unemployment rate ticking down, but the job to applicant ratio also fell.

- US yields are mostly lower, more so at the back end of the curve. Yen hasn't reacted much to these moves though.US equity futures are steady.

- AUD/USD sits unchanged, last near 0.6610. The Dec retail sales was weaker than expected , but the initial market reaction was muted. Earlier highs were at 0.6625. Weaker China/HK equity sentiment is likely weighing at the margin.

- Looking ahead, EU GDP prints later, while in the US house prices and consumer confidence is on tap.

EQUITIES: Regional Equities Mixed, China Down On Property Concerns

Asia equities are mixed today with Australia and Japan the standouts. US Equity Futures have been very uneventful today, trading flat but holding onto the late rally post the Treasury cut Jan-March borrow estimates from $816B to $760B, and estimates April-June at $202bn. Hong Kong and Mainland China stocks are sending clear signs that last weeks rescue package wont be enough to support the market and more needs to be done, to support them.

- Japan equity indices are trading higher today. Japan job data was out earlier and was somewhat mixed with the jobless rate ticking lower at 2.4% vs 2.5% est, Nintendo hit all time highs and there has been positive bank earnings numbers. The Topix is 0.26% higher, while the Nikkei is 0.30% higher.

- Hong Kong indices are much lower today as the market continues to react to the China Evergrande news that was out yesterday, traders now believe putting China Evergrande into liquidation will set a dangerous precedent for the rest of Chinas troubled property names, Hong Kong also unveiled details of a new planned security laws, which is weighing on stocks. Currently the Hang Seng is lower by 2.00%, Hang Seng tech index is 2.70% lower, while the Mainland China Property index is down 3.5%.

- Mainland China equities, much like Hong Kong are being dominated by China Evergrande, Chinese builder Radiance holdings has announced it's intention to hold meetings with bond holders of its march 2024 bond, which was last trading 65c on the dollar. China Yields have move to levels not seen since 2002, with the 10Y now trading at 2.46%. Equity Indices are all lower CSI 300 down 0.90%, while ChiNext is 1.10% lower.

- Taiwan is lower today, largely being pulled down by negative sentiment in the region, currently the Taiex is lower by 0.20%.

- South Korea, is flat today with no notable headlines to note.

- Australia had retail sales data out earlier, dropping 2.7% vs expectations of just a 1.7% fall, however the market has brushed that off and is continuing its winning run today, with the ASX 200 trading another 0.45% higher, all sectors are in the green today with tech names leading the way.

- In SEA today, most market are trading higher with the exception of Malaysia and Thailand. Poor results from Indian Banks has been weighing on the market, however the Nifty 50 are clinging onto gains today, currently up 0.15%

OIL: Marginally Higher, Market Awaits US Response To Jordan Attack

Brent is higher versus end Monday levels, although has largely tracked sideways in the first part of Tuesday trade. We were last around $82.65/bbl, around 0.30% firmer, but this follows Monday's 1.38% drop. WTI was last just above $77/bbl, showing a similar trajectory to Brent so far today.

- News flow has been reasonably light so far today, with markets waiting for the US response following the attack on its troops stationed in Jordan over the weekend. The most likely outcome is a strike on Iranian assets in the Middle East, but not within Iran itself (see this link).

- A number of US officials have stated that the US will respond but is not seeking to escalate the conflict.

- Elsewhere, the US administration may re-instate sanctions on Venezuela's energy sector if the country does not allow the opposition leader to run for President (see this BBG link).

- For Brent, recent lows rest near $82/bbl. Note the simple 200-day MA is near $81.70/bbl. On the topside, focus is likely to rest on whether we can test the $85/bbl.

GOLD: Helped Higher By Lower Bond Yields, Focus On Wednesday’s FOMC Meeting

Gold is slightly lower in the Asia-Pac session, after closing 0.7% higher at $2033.23 on Monday.

- Bullion was boosted on Monday by lower US Treasury yields, as investors turned their focus towards the Federal Reserve policy decision on Wednesday that could provide fresh clues on when the US monetary easing cycle will start.

- Fed speakers have been in a blackout ahead of this week’s FOMC meeting.

- The market is currently assigning around a 40% chance to a 25bp rate cut in March. This compares to the near 70% chance seen a couple of weeks ago.

- Lower interest rates are typically positive for non-interest-bearing gold.

- Resistance is seen at $2039.4 (Jan 19 high), according to MNI’s technicals team.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 30/01/2024 | 0630/0730 | ** |  | FR | Consumer Spending |

| 30/01/2024 | 0630/0730 | *** | | FR | GDP (p) |

| 30/01/2024 | 0800/0900 | *** |  | ES | HICP (p) |

| 30/01/2024 | 0800/0900 | *** | | ES | GDP (p) |

| 30/01/2024 | 0800/0900 | ** |  | CH | KOF Economic Barometer |

| 30/01/2024 | 0800/0900 | ** |  | SE | Economic Tendency Indicator |

| 30/01/2024 | 0900/1000 | *** |  | IT | GDP (p) |

| 30/01/2024 | 0900/1000 | ** | | IT | PPI |

| 30/01/2024 | 0900/1000 |  | EU | ECB's Lane on 'a year with the euro in Croatia' | |

| 30/01/2024 | 0900/1000 | *** |  | DE | GDP (p) |

| 30/01/2024 | 0930/0930 | ** |  | UK | BOE M4 |

| 30/01/2024 | 0930/0930 | ** | | UK | BOE Lending to Individuals |

| 30/01/2024 | 1000/1100 | *** | | EU | EMU Preliminary Flash GDP Q/Q |

| 30/01/2024 | 1000/1100 | *** | | EU | EMU Preliminary Flash GDP Y/Y |

| 30/01/2024 | 1000/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 30/01/2024 | 1000/1100 | ** | | EU | EZ Economic Sentiment Indicator |

| 30/01/2024 | 1000/1100 | * | | EU | Consumer Confidence, Industrial Sentiment |

| 30/01/2024 | 1355/0855 | ** |  | US | Redbook Retail Sales Index |

| 30/01/2024 | 1400/0900 | ** | | US | S&P Case-Shiller Home Price Index |

| 30/01/2024 | 1400/0900 | ** | | US | FHFA Home Price Index |

| 30/01/2024 | 1400/0900 | ** | | US | FHFA Home Price Index |

| 30/01/2024 | 1500/1000 | *** | | US | Conference Board Consumer Confidence |

| 30/01/2024 | 1500/1000 | ** | | US | housing vacancies |

| 30/01/2024 | 1500/1000 | *** | | US | JOLTS jobs opening level |

| 30/01/2024 | 1500/1000 | *** | | US | JOLTS quits Rate |

| 30/01/2024 | 1530/1030 | ** | | US | Dallas Fed Services Survey |

| 30/01/2024 | 1630/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 31/01/2024 | 2350/0850 | * |  | JP | Retail sales (p) |

| 31/01/2024 | 2350/0850 | ** | | JP | Industrial production |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.