Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- BOJ KEEPS YCC, NEGATIVE RATE, FORWARD GUIDANCE - MNI BRIEF

- FED OFFICIAL SAYS RATE CUTS COULD BE NEEDED NEXT YEAR TO PREVENT OVERTIGHTENING - WSJ

- HOUTHI ATTACKS START SHUTTING DOWN RED SEA MERCHANT SHIPPING - BBG

- US ANNOUNCES NEW TASK FORCE TO COUNTER HOUTHI RED SEA THREAT - BBG

- RBA BOARD DISCUSSES QT, HOLDS FIRM - MINUTES - MNI

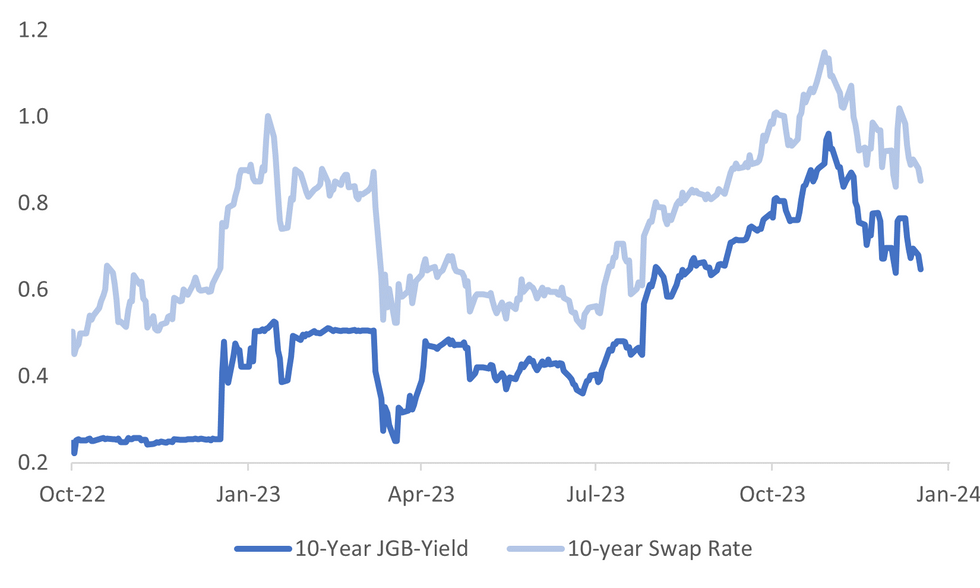

Fig. 1: Japan 10yr JGB Yield & 10yr Swap Rate

Source: MNI - Market News/Bloomberg

U.K.

Fiscal (RTRS): Britain plans to increase funding for local government councils by 4 billion pounds to 64 billion pounds ($81 billion) to address inflation-driven pressures, after cities Birmingham and Nottingham effectively declared bankruptcy.

EUROPE

SERBIA (BBG): Serbia’s snap election on Sunday was marred by irregularities, media bias and the misuse of state resources that skewed the race in favor of President Aleksandar Vucic’s ruling party, according to European observers.

ECB (BBG): Federal Reserve economist Chiara Scotti is poised to become a Bank of Italy executive after being nominated for the role on Monday. Currently head of research and a senior vice president at the Dallas Fed, she is set to move to Rome to succeed Piero Cipollone, who just became an Executive Board member at the European Central Bank in Frankfurt.

CZECH REPUBLIC (BBG): The Czech Republic is on track to meet its budget deficit target despite concerns earlier in the year that the shortfall was getting out of control, according to Finance Minister Zbynek Stanjura.

FISCAL/UKRAINE (FT): The European Bank for Reconstruction and Development shareholders have agreed a €4b capital increase, the Financial Times reports, citing EBRD president Odile Renaud-Basso. Capital increase to be announced on Tuesday. Will enable it to raise annual lending to Ukraine to €3b. EBRD president says capital increase is a sign that support for Ukraine will not waver

U.S.

FED (WSJ): A Federal Reserve official said it is appropriate for the central bank to begin looking ahead to lowering interest rates in 2024 because of how inflation has improved this year. San Francisco Fed President Mary Daly said her outlook for interest rates and inflation was "very close" to the median of projections from 19 Fed officials last week. Most of them penciled in at least three rate cuts next year amid a faster decline in inflation than they anticipated.

MID EAST (BBG): US Defense Secretary Lloyd Austin announced a new maritime task force intended to protect commercial vessels traveling through the Red Sea from attacks by Houthi militants. “The recent escalation in reckless Houthi attacks originating from Yemen threatens the free flow of commerce, endangers innocent mariners and violates international law,” Austin said in a statement Monday. “This is an international challenge that demands collective action.”

POLITICS (RTRS): Donald Trump in a second term would likely install loyalists in key positions in the Pentagon, State Department and CIA whose primary allegiance would be to him, allowing him more freedom than in his first presidency to enact isolationist policies and whims, nearly 20 current and former aides and diplomats said.

POLITIC (BBG): Senate Republican leaders made clear Monday that a quick deal on border security is out of reach before the Christmas holiday, all but guaranteeing votes on Ukraine and Israel aid will be punted to next year.

CORPORATE (BBG): Apple Inc., just days away from a US ban of its smartwatches, is plotting a rescue mission for the $17 billion business that includes software fixes and other potential workarounds.

OTHER

SHIPPING (BBG): Shipping in the Red Sea is grinding to a halt with oil tankers idling and container vessels rerouting around Africa as violence linked to the Israel-Hamas war threatens to undermine the global economy. Two European oil and gas giants said Monday that their tankers would avoid waters off the coast of Yemen — an unavoidable waypoint for ships using the Suez Canal to cut between Europe and Asia.

JAPAN (MNI BIREF): The Bank of Japan board on Tuesday decided unanimously to keep yield curve control policy, including the negative interest rate, and pledged to continue patiently with monetary easing amid high uncertainty on economies and financial markets.

JAPAN (MNI BRIEF): The Bank of Japan board on Tuesday left its assessment on the current economic climate but tweaked its assessment on private consumption and capital investment, which both recently fell.

JAPAN (BBG): Nippon Steel Corp. will buy United States Steel Corp. for $14.1 billion to create the world’s second-largest steel company — and the biggest outside of China — with a key role in supplying American manufacturers and automakers.

AUSTRALIA (MNI): The Reserve Bank of Australia board maintained its stance on the reduction of its legacy government bond portfolio and will continue to hold until maturity, according to the minutes from the December meeting released Tuesday.

NEW ZEALAND (RTRS): New Zealand's business confidence rose in December amid a bounce in most activity indicators and is now at its highest level since March 2015, an ANZ Bank survey showed on Tuesday. The survey's headline measure showed a net 33.2% of respondents expected the economy to improve over the year ahead, versus a 30.8% optimism level in the previous poll in November.

CHINA

YUAN (CIS.CN): The yuan will likely further strengthen against the U.S. dollar to break the 7 level next year as the Federal Reserve is expected to start rate cuts, financial news agency Cls.cn reported citing market insiders. Wang Tao, chief China economist at UBS, adjusted the yuan forecast for end-2023 to around 7.1 from the previous 7.3, and raised the forecast for 2024 to 7.0 from the previous 7.15.

INVESTMENT (SECURITIES DAILY) The National Conference on Development and Reform plans to use government investment to consolidate and enhance the positive trend of economic recovery next year. Leaders will utilise local government special bonds plus the additional CNY1 trillion of treasury bonds to boost sectors such as transport infrastructure, energy, agriculture, forestry and water conservancy, an NDRC statement noted.

REFORM (GOV.CN) China should accelerate the establishment of a national unified market by improving market access, property rights protection and fundamental institutions on transaction, data information, and social credit, according to a State Council executive meeting on Monday presided over by Premier Li Qiang.

PROPERTY (BBG): A Chinese developer partially owned by the southern city of Shenzhen warned it can’t pay interest due Wednesday as it races to win support from creditors to extend dollar bond deadlines, raising the risk of its first default.

CHINA MARKETS

MNI: PBOC Drains Net CNY113 Bln Via OMO Tues; Rates Unchanged

The People's Bank of China (PBOC) conducted CNY119 billion via 7-day reverse repo and CNY182 billion via 14-day on Tuesday, with the rates unchanged at 1.80% and 1.95%, respectively. The reverse repo operation has led to a net drain of CNY113 billion reverse repos after offsetting CNY414 billion maturity today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.7529% at 09:38 am local time from the close of 1.8419% on Monday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 50 on Monday, compared with the close of 45 on Friday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

PBOC Yuan Parity Higher At 7.0982 Tuesday vs 7.0933 on Monday

The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.0982 on Tuesday, compared with 7.0933 set on Monday. The fixing was estimated at 7.1338 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND NOV TRADE BALANCE NZD -1234MN; PRIOR -1730MN

NEW ZEALAND NOV TRADE BALANCE 12 MTH YTD NZD -13874MN; PRIOR -14823MN

NEW ZEALAND NOV EXPORTS NZD 5.99BN; PRIOR 5.73BN

NEW ZEALAND NOV EXPORTS NZD 7.23BN; PRIOR 7.10BN

NEW ZEALAND DEC ANZ ACTIVITY OUTLOOK 29.3; PRIOR 26.3

NEW ZEALAND DEC ANZ BUSINESS CONFIDENCE 33.2; PRIOR 30.8

MARKETS

US TSYS: Narrow Session In Asia, Fedspeak from Barkin & Bostic Due

TYH4 deals at 112-09+, +0-01+, a 0-07 range has been observed on volume of ~88k.

- Cash tsys sit ~1bp cheaper across the major benchmarks.

- Tsys have observed narrow ranges for the most part in Asia today with little follow through on moves. A retreat from session highs was seen alongside JGBs paring post-BOJ gains.

- Flow-wise the highlight was a block buyer in TU (2.3k lots).

- On today's docket we have Home Sales and Consumer Confidence before Fedpseak from Richmond Fed President Barkin and Atlanta Fed President Bostic provide the highlight.

JGBS: Few Surprises From The BoJ, MoF Set To Reduce 20Y Auction Size

JGB futures are slightly stronger at 146.07, +11 compared to settlement levels, after paring the initial spike higher (high of 146.35) following the BoJ Policy Decision. The BoJ left the policy rate at -0.1% and the 10-year yield target at 0%, as expected. The BoJ also kept the upper bound reference rate on long-term yields at 1%.

- The decision to keep all policy parameters unchanged is likely to have disappointed those advocating for a January 2024 exit from the negative interest rate policy (NIRP). The prospect of the BoJ terminating NIRP without prior adjustments to forward guidance is generally perceived as improbable.

- The explicit easing bias was also maintained, with the BoJ stating that it will “patiently continue with monetary easing”. The removal of this easing bias is generally seen as a necessary step before rate hikes are considered.

- The market now awaits Governor Ueda’s press conference at 15:30 Japan time today.

- Cash JGBs have strengthened with the curve bull-flattening. Yields are 0.3bp to 2.5bps lower across benchmarks. The 10-year yield is 2.5bps lower at 0.655% versus today’s high of 0.688%

- The swaps curve has also shifted to a bull-flattening following the decision.

- (Reuters) The MoF is set to front-load reductions in 20-year JGBs by Y200bn from January as rising interest rates dampen investor appetite for the interest-bearing long-dated debt, two government sources said.

AUSSIE BONDS: Cheaper, BoJ Decision Absorbed With Little Impact

ACGBs (YM -6.0 & XM -6.5) sit in the middle of today’s Sydney session ranges after the RBA Minutes did not serve as a significant domestic market driver ahead of the BoJ Policy Decision, which stood out as the focal point for today’s Asia-Pac session.

- The RBA board considered two options at the Dec meeting, a rate hike or holding steady. The on-hold outcome won out with the RBA in a wait-and-see mode, particularly with so little fresh data compared to the prior meeting in November.

- The BoJ decision revealed unchanged policy parameters, as expected. Nevertheless, the market exhibited a mild strengthening following the announcement, indicating that certain participants had positioned themselves for a potentially hawkish surprise. The market now awaits Governor Ueda’s press conference at 15:30 Japan time today.

- The domestic market and US tsys have absorbed the BoJ decision without significant impact, with the latter trading flat to 2bps cheaper in today's Asia-Pac session, despite the strengthening in JGBs.

- Cash ACGBs are 6bp cheaper, with the AU-US 10-year yield differential 2bps wider at +17bps.

- Swap rates are 5-6bps higher.

- The bills strip is cheaper, with pricing -5 to -7.

- RBA-dated OIS pricing is 2-6bps firmer on the day. 54bps of easing is still priced for Nov’24.

- The local calendar is empty tomorrow and Thursday.

NZGBS: Cheaper Ahead Of Tomorrow’s Fiscal Update, BoJ Delivered Few Surprises

NZGBs have closed flat to 2bps cheaper across benchmarks after trading within a relatively narrow ranges during today’s local session. Despite the trade balance outperforming expectations, it did not serve as a significant domestic market driver ahead of the BoJ Policy Decision, which stood out as the focal point for today's Asia-Pac session.

- In line with expectations, the BoJ decision revealed unchanged policy parameters. Nevertheless, the market exhibited a mild strengthening following the announcement, indicating that certain participants had positioned themselves for a potentially hawkish surprise. The market now awaits Governor Ueda’s press conference at 15:30 Japan time today. The local market was closed when JGB futures resumed trading after the BoJ decision.

- US tsys are dealing flat to 2bp cheaper in today’s Asia-Pac session despite the richening in JGBs.

- The swaps curve finished with a twist-flattening, with rates 4bps higher to 3bps lower.

- RBNZ dated OIS pricing closed 1-4bps firmer across meetings. 97bp of easing is still priced for Nov’24.

- Tomorrow, the local calendar sees the Half-Year Economic and Fiscal Update.

FOREX: Yen Pressured After BOJ Holds Policy Steady

The Yen has been pressured as the BOJ held policy unchanged as expected with the short-term rate at -0.1% and a target for the 10-year JGB yield at about 0%. USD/JPY last prints at ¥143.45/50, ~0.5% higher today. We sit a touch below the immediate post decision high of ¥143.73.

- Resistance at ¥143.16, high from Dec 18, has been breached and the next target for bulls is ¥143.78, 50.0% retracement of Dec 11-14 sell off. A break through here opens ¥146.59, High from Dec 11 and key short term resistance.

- Kiwi is firmer, NZD/USD is up ~0.3% as yesterday's NY session losses are trimmed. A reminder that early in today's session the November Trade Balance narrowed a touch from October printing at $1.234bn. ANZ Business Confidence ticked higher in December to 33.2 from 30.8, the Activity Outlook rose to 29.3 from 26.3.

- AUD/USD is up ~0.2%, the pair is consolidating above the $0.67 handle today. Support was seen for the AUD after the RBA minutes were a touch hawkish.

- Elsewhere in G-10 there have not been any moves of note.

- Cross asset flows are muted; US Tsys and US Equity futures are little changed today, as is WTI.

EQUITIES: Japan Markets Firm Post Dovish BoJ Hold, HK Markets Weighed By Property

Regional equities are mixed in Asia Pac markets for Tuesday trade. Japan markets have risen post the dovish BoJ hold. Hong Kong and China markets have struggled somewhat amid further property related concerns. US futures have been range bound, Eminis last close to 4793, nearly flat for the session. Nasdaq futures sit down a touch.

- Japan shares opened up after the lunch time break on a positive footing, albeit losing ground from best levels. The Nikkei 225 was last around +1%, while the Topix was around 0.40% higher.

- The BoJ left all major policy parameters unchanged, while it also didn't hint an imminent policy shift in early 2024. The announcement weakened the yen, aiding the share backdrop, although bank stocks have underperformed.

- At the break in HK, the HSI sits down 0.61%. Country Garden services fell sharply as it set aside funds for an impairment provision. Stocks in the company hit an all time low. This comes after yesterday's announcement from China South City Holdings that it wouldn't be able to pay interest due tomorrow.

- On the mainland, the CSI 300 and Shanghai Composite are close to flat at the break.

- Elsewhere, the Taiex is down -0.85%, while the Kospi is near flat. The ASX 200 is up 0.80%, aided by higher commodity prices.

- In SEA, most markets are higher, but gains are limited (sub 0.50%) at this stage.

OIL: Largely Holding Monday Gains, As US Announces Red Sea Naval Task Force

Oil benchmarks have largely drifted sideways in the first part of Tuesday trade. We were last near $78.10/bbl for Brent, a touch above end Monday levels. WTI was last around $72.35bbl, down slightly from end Monday levels near $72.50/bbl.

- Near term focus remains on developments in the Red Sea, where attacks from Houthi rebels in Yemen is threatening a major oil shipping route. Several companies announced yesterday they were diverting shops away from the region.

- Headlines earlier today crossed that the US has put together a new naval task force to patrol the troubled area and protect commercial vessels (see this link for more details).

- Focus will be whether Houthi (who are backed by Iran) attacks escalate from here and cause further stress in terms of shipping lines.

- For Brent we are above $77.81 (20-day EMA) with Monday's high of $79.49 stopping short of resistance at $80.76 (50-day EMA).

GOLD: Geopolitical Tensions Buoyed Bullion

Gold is little changed in the Asia-Pac session, after closing 0.4% higher at $2027.19 on Monday.

- Increased geopolitical tensions buoyed bullion. Vessel attacks in the Red Sea are increasing. Yemen’s Iranian-backed Houthi rebels have claimed responsibility for attacks on two ships on December 18 - the Swan Atlantic and MSC Clara - using naval drones, according to Alarabiya news.

- The precious metal’s gain came despite Fedspeak continuing to push back against expectations for early and significant rate cuts next year.

- Fed Mester told the FT that the market had gotten “a little bit ahead” by pencilling in early interest rate cuts, “the next phase is … about how long do we need monetary policy to remain restrictive in order to be assured that inflation is on that sustainable and timely path back to 2%”. Meanwhile, Fed Goolsbee told CNBC he was confused with the market’s reaction to the Fed’s policy update last week.

- However, the cheapening in US Treasury benchmarks was small, with yields finishing flat to 4bps higher.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 19/12/2023 | 0900/1000 |  | EU | ECB Elderson Statement On Banking Risks and Priorities | |

| 19/12/2023 | 1000/1100 | *** | | EU | HICP (f) |

| 19/12/2023 | 1000/1000 | ** |  | UK | Gilt Outright Auction Result |

| 19/12/2023 | 1300/1300 | | UK | BOE Breeden Speech At IIF Policy Series | |

| 19/12/2023 | 1330/0830 | *** |  | CA | CPI |

| 19/12/2023 | 1330/0830 | * | | CA | Industrial Product and Raw Material Price Index |

| 19/12/2023 | 1330/0830 | *** |  | US | Housing Starts |

| 19/12/2023 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 19/12/2023 | 1630/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 19/12/2023 | 1730/1230 | | US | Atlanta Fed's Raphael Bostic | |

| 19/12/2023 | 2100/1600 | ** | | US | TICS |

| 20/12/2023 | 2350/0850 | ** |  | JP | Trade |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.