Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

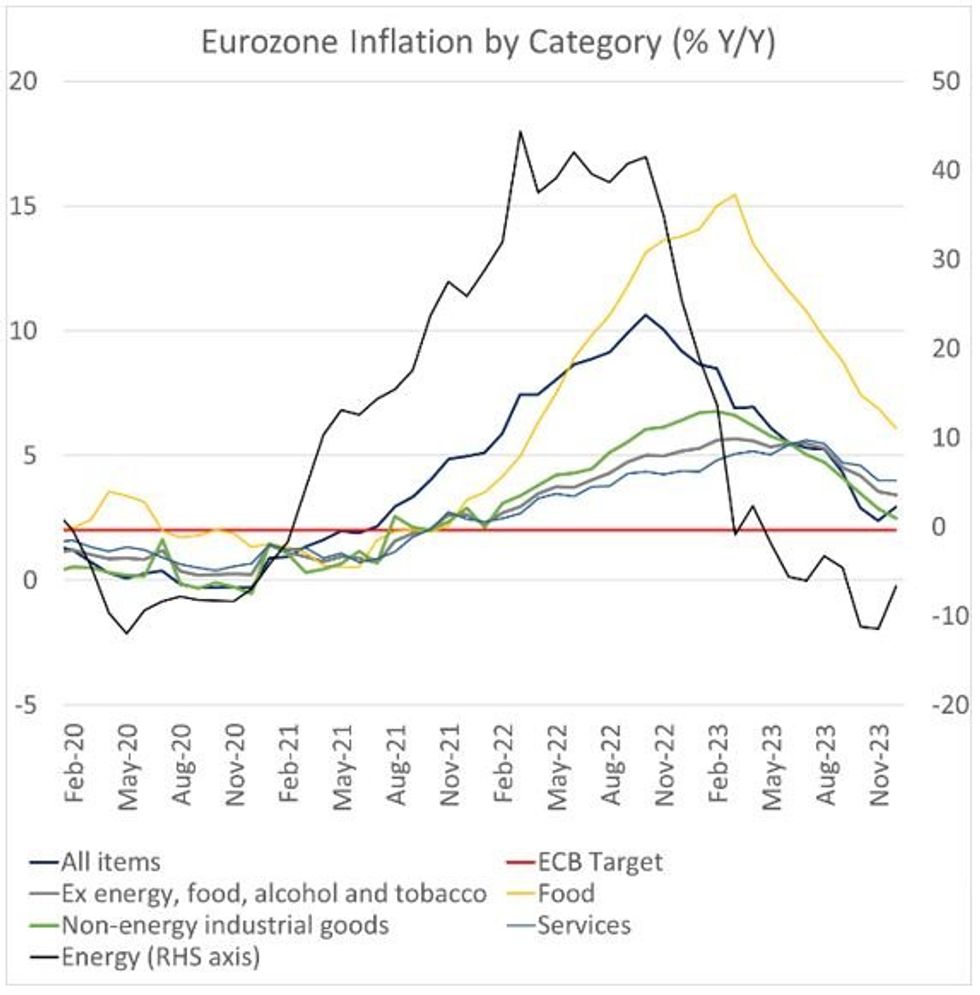

We have just published our preview of January's Eurozone flash inflation round, which began today and runs through Thursday morning's EZ-wide estimate. Our preview has been emailed to clients and is available in PDF here.

- The January flash eurozone inflation round is expected to show a pullback in Y/Y price gains versus December, with overall HICP printing 2.7% Y/Y (2.9% prior) and core 3.2% Y/Y (3.4%).

- This would represent a resumption in the overall downtrend: December’s Y/Y headline figure reflected an 0.5pp uptick but that was largely the result of base effects (German energy subsidies in December 2022), and while sequential core inflation ticked higher (+0.0% M/M vs -0.2% prior), Y/Y slipped to 3.4% Y/Y (vs 3.6% prior) and core momentum saw a deceleration (see our December HICP recap in the next section).

- January’s prints are set to be “noisy” with multiple hard-to-predict factors coming into play. The theme of energy-related distortions is expected to continue, with German, French, Italian, and Dutch energy support measures dropping out from year-earlier comparisons. Food and core goods prices are seen continuing to disinflate.

- While services prices are seen as disinflationary, there is uncertainty generated in part by annual weighting changes. Added to these uncertainties are tax changes to start the year, as well as the typical annual re-pricing of goods and services across multiple industries.

- In terms of the impact on ECB policy, below-expected incoming readings, along with progress on wage dynamics, will probably be required to bring a cut earlier than the summer.

- Our preview includes analysis of price categories to watch, assessments of underlying inflation trends, outlooks for the French, German, and Italian national inflation prints, and sell-side analyst previews.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok