Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI Fed Preview - Dec 2023: Analyst Outlook

MNI Fed Preview - Dec 2023: Analyst Outlook

- Note to readers: This is an update to the MNI Fed preview published on Friday Dec 8. Please see Page 32-38 of this document for sell-side analysts' outlooks for the Dec 13 2023 FOMC decision and future policy.

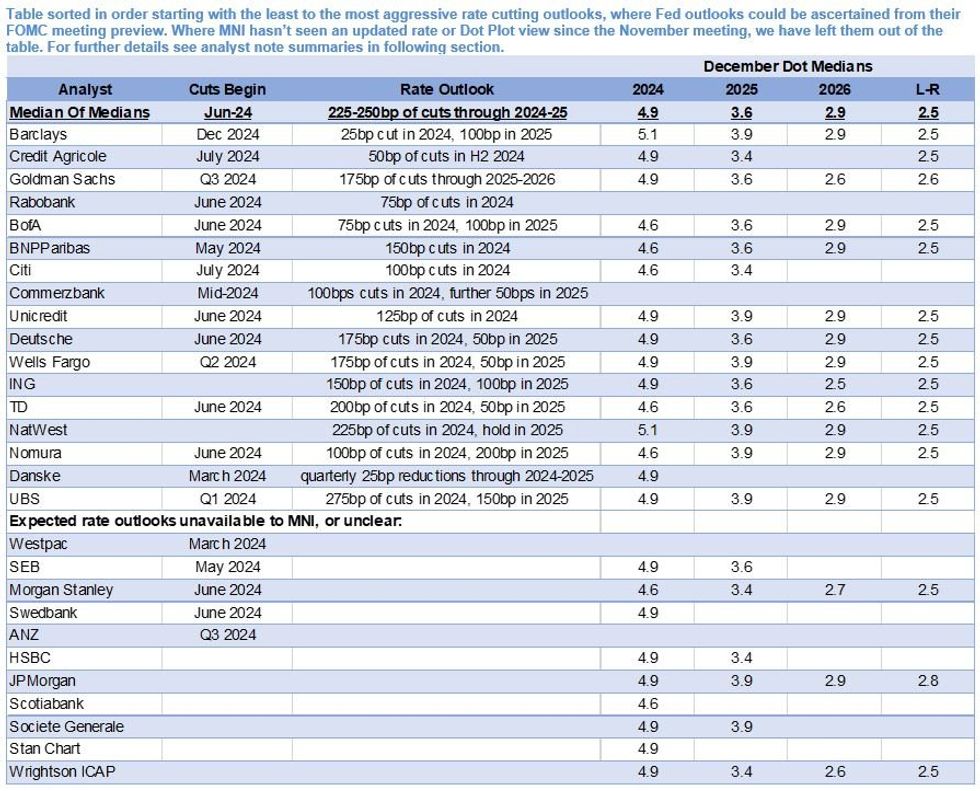

EXECUTIVE SUMMARY:

Analysts Split On 2024 Dot And Forward Guidance Changes

Sell-side analysts are unanimously agreed that the FOMC will leave rates on hold at the December meeting, but there is more disagreement than usual over changes to communications in the 31 previews we read.

- Starting with the Dot Plot, which will probably the most closely-watched part of the communications: the median of analysts’ medians for the 2024 Fed funds rate dot is 4.9%, representing 50bp of cuts next year, and 25bp lower than the September projection of 5.1%. ·Opinion is quite split though: the 21 analysts who provided their Dot expectations, 2 saw a 5.1% 2024 median (Barclays and NatWest), while 7 saw a 4.6% median.

- For the outer years, the median expectations are 3.6% for 2025 (range of 3.4-3.9%) and 2.9% for 2026 (range of 2.5-2.9%). Almost all analysts expect the longer-run median dot to remain at 2.5%, with notable exceptions Goldman Sachs (2.6%) and JPMorgan (“good chance” of 2.75%).

- As for the rate path ahead: there is a wide range of expectations for Fed easing, with the most restrained being Barclays (just one 25bp cut in 2024, with 100bp in 2025), and the most reductions seen by UBS ( 275bp of cuts in 2024, 150bp in 2025).

- General consensus is that Fed easing will start in mid-2024, though there’s no clear expectation of timing.

FOR THE FULL PUBLICATION PLEASE USE THE FOLLOWING LINK:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok