Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

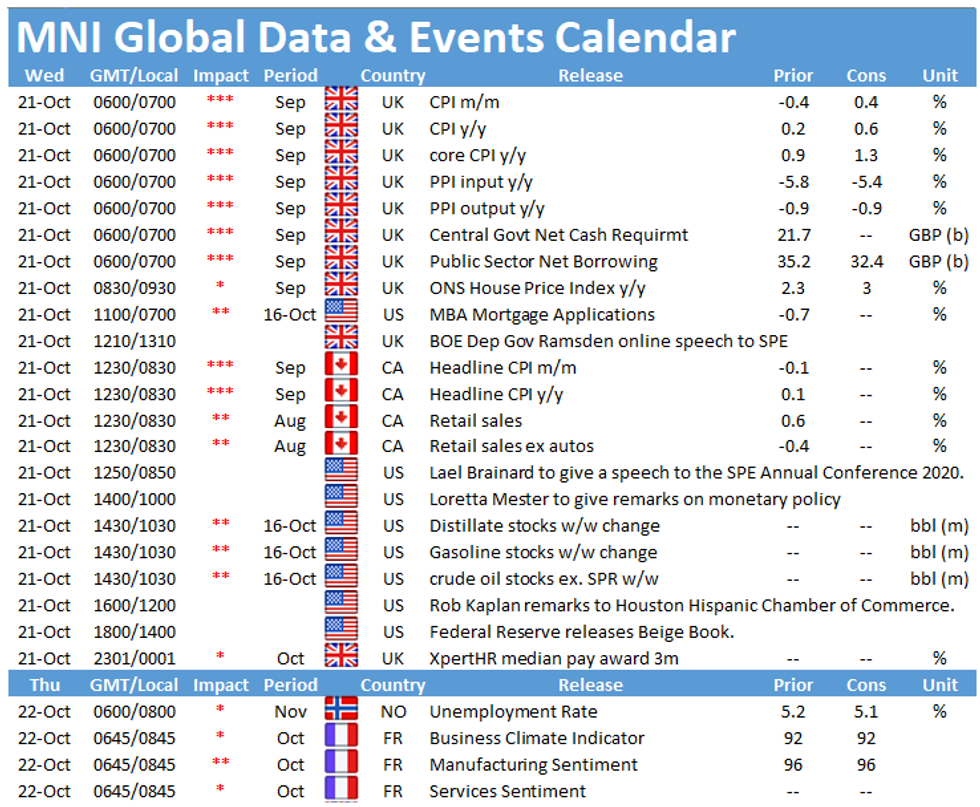

Wednesday morning kicks off with the publication of UK inflation figures alongside the UK public sector finances, both released at 0700BST. In the North Americas, the highlight of the day is the release of Canadian inflation figures at 1330BST.

UK inflation expected to rise

Inflation in the UK is forecast to accelerate slightly to 0.6% in September after plunging to 0.2% in August which was the lowest level since 2015. Following a sharp decline of core inflation in August to 0.9%, the indicator is seen rising to 1.3% in September. August's downtick was mainly driven by falling prices in restaurants and cafes due to the government's "eat out help out" scheme. The scheme closed at the end of August, hence prices in restaurants should see an uptick in September. The BRC shop price index posted another decline in September and the report noted that non-food prices drove the decrease, led by clothing and footwear. According to the UK's services PMI, inflation was modest in September as firms reported lower employment expenses, while operating costs ticked up marginally.

UK budget deficit seen lower

The budget deficit (PSNB-ex Banking Groups) is expected to improve slightly to GBP 33.6bn in September after recording GBP 35.9bn. Borrowing was GBP 30.5bn more in August 2020 than in the previous year and the third highest level since records began. Nevertheless, the budget deficit is slightly better than the OBR expected in recent months. As the furlough scheme gets less generous in October, the deficit is likely to reduce further. However, this is depended on the development of the pandemic and the ONS noted that borrowing is subject to more uncertainty than usual and larger revisions are likely.

Canadian consumer prices forecast to edge higher

Annual inflation remained unchanged in August at July's level of 0.1%, while excluding gasoline, CPI rose by 0.6% which is slightly less than July's reading of 0.7%. In September, markets look for an uptick to 0.5% which would be the highest level since June. While gas prices were still down in August compared to a year ago, the costs for personal care services increased sharply in August due to safety measures introduced as a result of the pandemic. According to the BOC's business outlook survey firms expect inflation to remain low going forward as demand remains weak.

The events calendar throws up a busy schedule on Wednesday including speeches by ECB's Luis de Guindos and Philip Lane, BOE's Dave Ramsden, Cleveland Fed's Loretta Mester, Dallas Fed's Rob Kaplan and St. Louis Fed's James Bullard.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.