Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

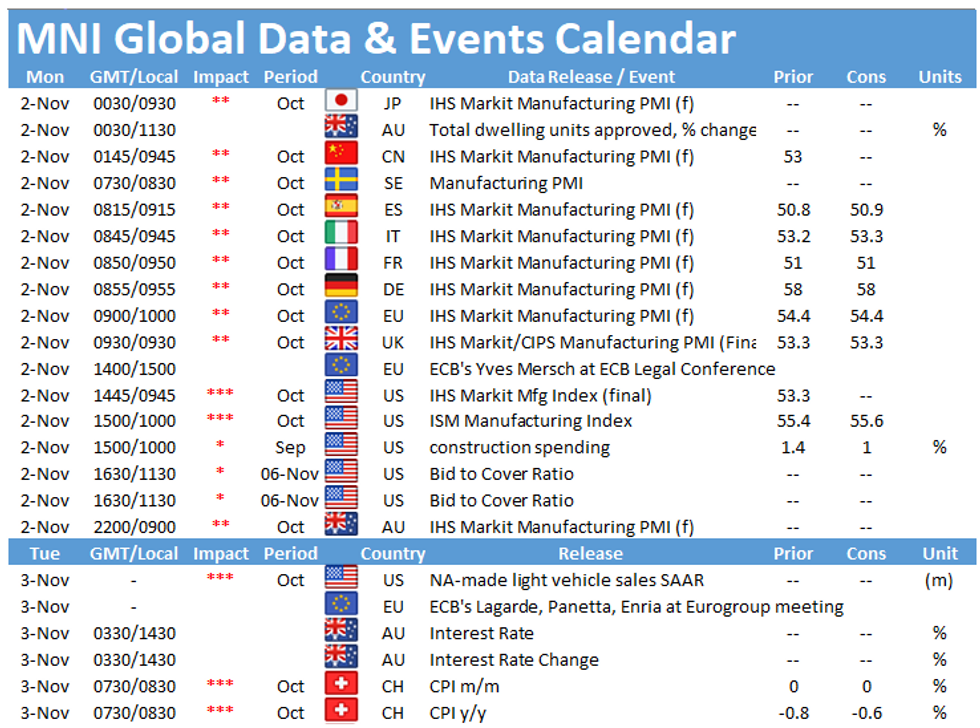

The main focus on Monday will be on the release of the final manufacturing PMIs, starting with Spain (0815GMT) and followed by Italy (0845GMT), France (0850GMT), Germany (0855GMT), the EZ (0900GMT) and the UK (0930GMT). In the US the publication of the ISM manufacturing PMI at 1500GMT will be closely followed.

Manufacturing PMIs continue to signal expansion

The final manufacturing PMIs for France, Germany, the EZ and the UK are forecast to register in line with the flash results. All four manufacturing PMIs remained in expansion territory in October according to the flash estimate. The flash estimate further noted the divergence of the manufacturing and the service sector as the renewed social distancing measures weigh more on service sector business activity.

Among the major Eurozone countries, Germany outperformed its peers. The countries manufacturing PMI rose to a 30-month high of 58.0 in October and markets expect an unchanged reading for the final results. The overall EZ PMI increased as well to 54.4, marking a 26-month high. The French and the UK's manufacturing PMI eased in October to 51.0 and 53.3, respectively.

The Spanish and the Italian manufacturing PMIs, for which no flash estimates are released, are expected to edge slightly higher in October. Markets look for the Spanish index to tick up 0.1pt to 50.9 and for the Italian PMI to increase to 53.3, up from 53.2 recorded in September.

ISM Manufacturing PMI seen slightly higher

The ISM manufacturing PMI cooled slightly in September to 55.4, down from 56.0 recorded in August. In October, markets are looking for a marginal increase to 55.6. September's downtick was driven by a sharp drop in New Orders, falling by 7.4pt. Production declined as well, while Employment, Inventories and Supplier Deliveries ticked up. Similar survey evidence provides a mixed picture. While the Chicago Business Barometer eased slightly in October, the Dallas Fed manufacturing index improved further to a two-month high. Meanwhile, flash IHS manufacturing PMI edged up modestly in October, signalling expansion in the sector.

The events calendar remains quiet on Monday. The only event scheduled is a speech by ECB's Yves Mersch at ECB Legal Conference.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.