Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

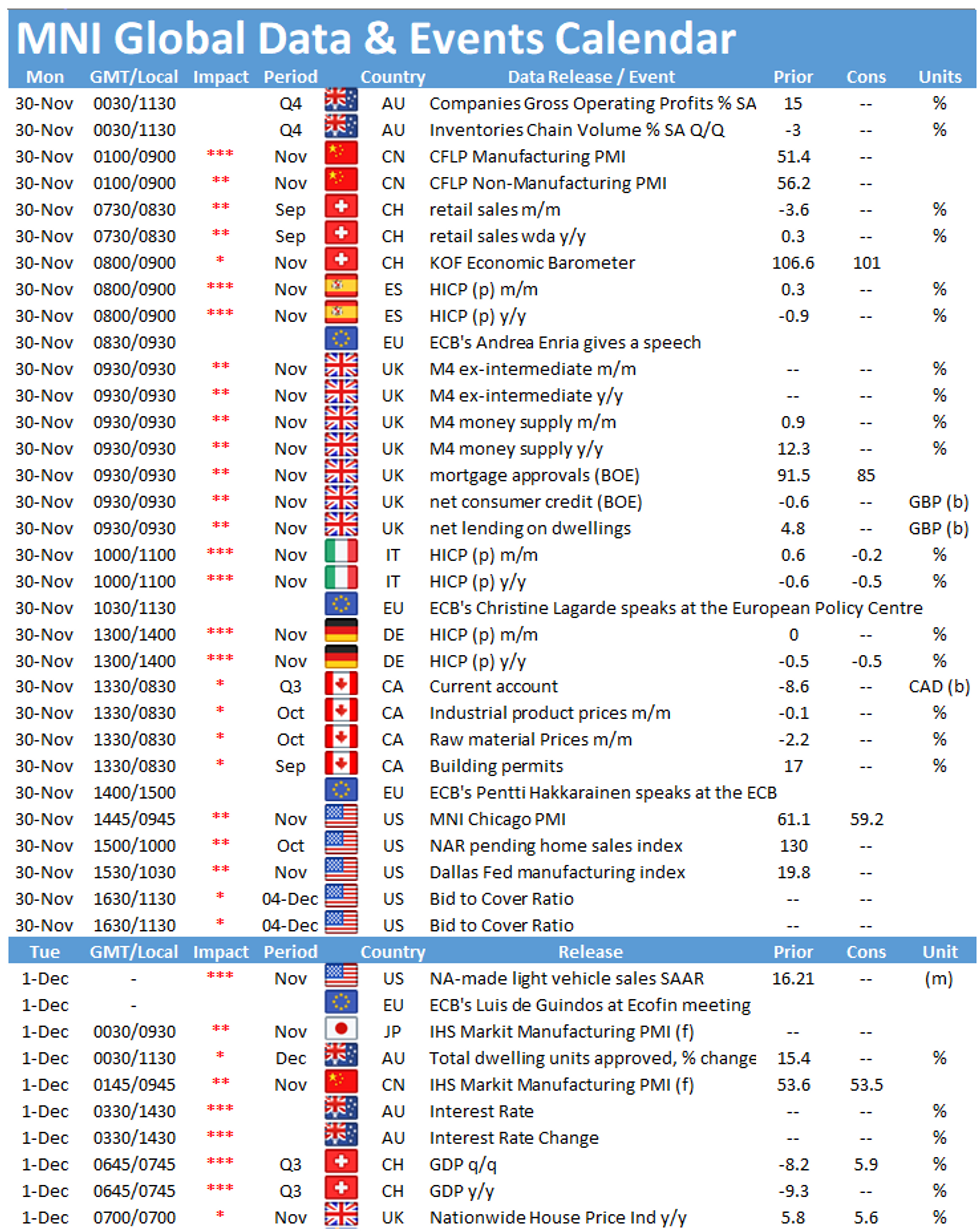

Monday throws up a busy schedule in terms of data releases with the highlights being the publication of flash inflation figures for Italy at 1000GMT followed by Germany at 1300GMT. In the US the publication of the Chicago Business Barometer will be closely watched at 1445GMT.

Italian inflation projected to edge slightly higher

Flash inflation is expected to tick up marginally to -0.5% in November after declining by 0.6% in the previous month. The national print for inflation registered at -0.3% in October, up from -0.6% seen in September. The difference between the HICP and the CPI mainly stems from effects of the end of summer sales which are not taken into account by the CPI. The flash composite PMI for the Eurozone noted a decline in prices in the service sector due to discounting which is in line with the negative inflation reading for Italy in November.

German inflation seen unchanged

German inflation recorded the third successive negative reading in October, declining by 0.5% after falling 0.4% in September. In November, markets are looking for annual inflation to register at October's reading. One reason for the negative inflation rate was the temporary VAT reduction which was introduced in July. Moreover, energy prices dragged down inflation. Excluding energy prices, HICP increased by 0.6% in October. The flash composite PMI for Germany showed an increase in prices charged for goods and services in November, suggesting an upward risk for inflation.

Chicago Business Barometer forecast to decline

The Chicago Business Barometer slipped to 61.1 in October following September's sharp increase. October's downtick was broad-based with every category except for New Orders showing a decline. In November, markets look for another fall to 59.2 amid the resurgence of Covid-19 cases. Similar survey evidence is in line with market forecasts. The Kansas City Fed's manufacturing index eased 2 points, while the Richmond Fed manufacturing index slumped 14 points in November.

The main events to look out for include speeches by ECB's Andrea Enria, Christine Lagarde and Pentti Hakkarainen.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.