Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

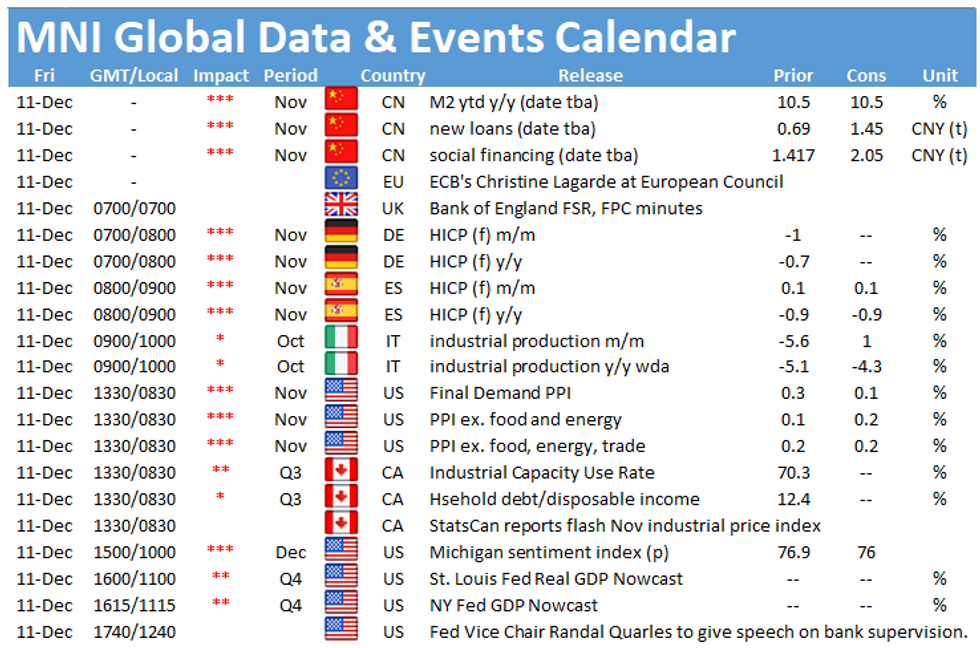

It is a quiet end to the week in terms of data releases. In Europe the only publications worth noting are the releases of German final inflation figures at 0700GMT and Italian industrial production at 0900GMT. In the US the main event to look out for is the release of producer price inflation at 1330GMT.

German final inflation seen at flash result

The final print of HCIP is expected to register in line with the flash estimate showing a decline of 0.7% in November. This would mark the fourth consecutive negative reading for annual inflation which is the longest deflationary period since 2009. Destatis noted that one of the main drivers of negative inflation is the German VAT cut which was introduced in July. Moreover, energy prices continue to drag down inflation. Looking ahead, another negative reading is likely in December as the VAT cut continues until January and the extended lockdown is likely keep energy prices low.

Italian industrial production projected to rise

Industrial production in Italy is forecast to rise by 1.0% in October after falling by 5.6% in September on a monthly basis. Annual output is set to show another negative reading with markets looking for a 4.3% drop. Survey evidence provides mixed signals. The Italian manufacturing PMI suggests continued improvement in the industrial sector although at a slower pace, while Istat's manufacturing sentiment eased in November and business confidence fell markedly.

US producer price inflation to remain subdued

The US PPI for final demand is forecast to slow to 0.1% m/m in November after it decelerated to 0.3% m/m in October. Final demand goods were the main driver of October's increase with prices rising by 0.5%, while the final demand services index edged up 0.2%. Excluding food, energy and trade services producer prices rose for final demand rose 0.2% on a monthly basis in October and markets look for an unchanged in November. Annual PPI is expected to accelerate to 0.7% in November, up from 0.5% seen in the previous month. While the ISM manufacturing PMI saw an unchanged reading for prices in November, both the IHS services and manufacturing PMI signalled an increase in input prices and prices charged.

The main events to look out for on Friday include appearances by ECB's Christine Lagarde, Kansas City Fed's Esther George and Fed's Randal Quarles.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.