Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

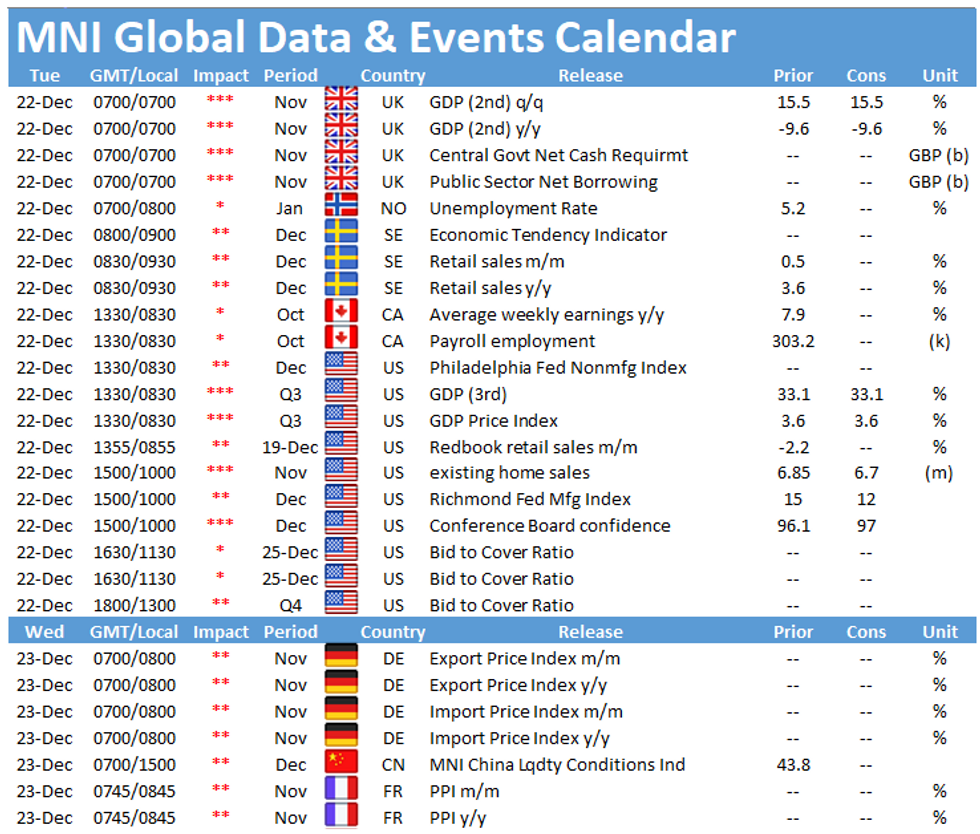

Tuesday morning kicks off with the publication of UK public sector finances and the UK's final print of GDP, both released at 0700GMT. In the US, the latest consumer confidence will be closely watched at 1500GMT.

UK borrowing seen higher

Public sector finances had been better than anticipated in recent months as government spending has been lower than expected. However, the ONS continuously noted that the dataset is likely to see sharp revisions as new data becomes available even after the release. Borrowing declined to GBP 22.3bn in October which was the second-lowest outturn since the beginning of the crisis. In November, markets look for borrowing excluding banking groups to increase to GBP 28bn, while total public sector net borrowing is seen higher at GBP 26.8bn. Government spending is likely to increase in the coming months as November saw a national lockdown and parts of the country moved into tier 4 ahead of Christmas.

UK final GDP expected to register at flash estimate

The final print of UK GDP is forecast to register in line with the flash result showing a quarterly rebound of GDP by 15.5% in Q3 after Q2's sharp decline. Annual GDP continues to decline in the third quarter, although at a slower pace of -9.6%. Private consumption was the main driver of the rebound in Q3, rising by 18.3%, while government spending was up 7.8% compared to the second quarter. Looking ahead, Q4 and most possibly Q1 are likely to post negative readings of quarterly GDP as the situation regarding Covid-19 intensified and the UK tightened the restrictions ahead of Christmas.

US consumer confidence forecast to tick up

The Conference Board consumer confidence index declined in November to 96.1, down from 101.4 seen in October. Both the present situations index as well as the expectations index decreased in November. The report noted that rising Covid-19 cases is increasing uncertainty and concerns regarding the outlook. Nevertheless, markets expect the indicator to edge slightly higher in December to 97.0.

The events calendar remains quiet ahead of Christmas with no speeches scheduled for the day.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.