Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

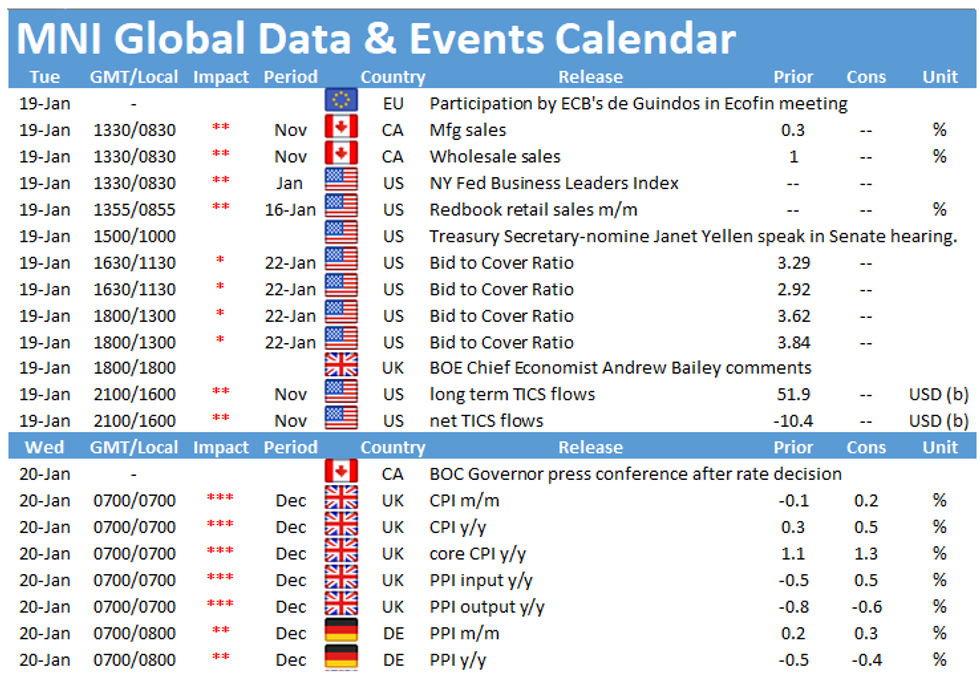

The main data events to follow on Tuesday include final German inflation figures at 0700GMT as well as the release of the ZEW survey at 1000GMT. In the North Americas the release of the Canadian survey of manufacturing at 1330GMT is the highlight.

Final German inflation seen at flash estimate

Source: Bloomberg

The final read of German inflation is expected to confirm December's flash estimate at -0.7%. This would mark the fifth consecutive negative reading. Destatis noted that the negative rates were mainly driven by the German VAT cut introduced in July and ends in December. Monthly prices increased 0.6% in December according to the flash estimate and markets look for an unchanged reading for the final results. Inflation decelerated to 0.4% in 2020 compared to 2019 if the flash estimates are confirmed.

ZEW Expectations forecast to rise

Survey: Bloomberg

The ZEW economic sentiment index is expected to increase to 57.8 in January from 55.0 seen in December, while the current conditions index is projected to deteriorate to -68.5, down from -66.5 seen in the previous month. Last month's survey noted that there is no clear upward trend yet of sentiment as uncertainty regarding the outlook remains high and economic growth in in the first quarter is likely to see a contraction. Moreover, infection rates in Germany remain high and restrictions got tightened in January which weighs especially on the current conditions index. However, the start of the vaccination program should provide a boost to economic sentiment in the coming months. The recently released Sentix index suggests an upside risk with current conditions rising to the highest level since March and expectations recording an all-time high.

Canadian manufacturing sales expected to decline

Manufacturing sales are expected to decrease by 0.3% in November after rising by 0.3% in the previous month. October's uptick was driven almost entirely by non-durable industries, especially by the paper, and petroleum and coal industries. Paper manufacturing sales rose 5.4%, while petroleum and coal product sales were up 3.1%. Manufacturing sales fell by 5.2% on an annual basis in October. Survey evidence suggests an upside risk with the IHS PMI rising to the highest level on record in December. The survey noted a sharp increase in new orders and new export orders which bodes well with manufacturing sales going forward.

The main events to follow on Tuesday include comments by U.S. Treasury Secretary-nominee Janet Yellen and BOE's Andrew Haldane.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.