Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

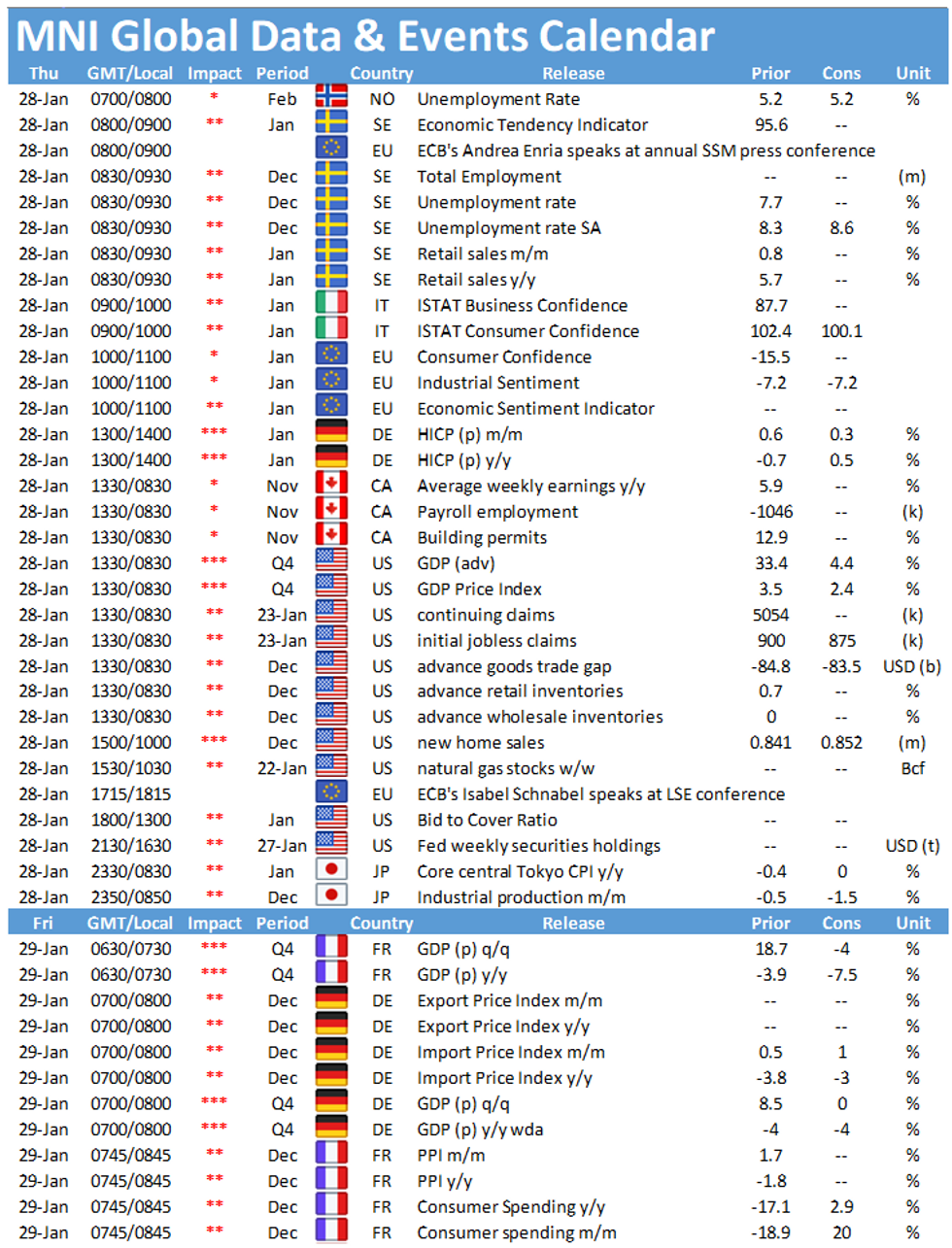

Thursday sees a full schedule of data releases, with the highlights in Europe including the publication of the European Commission's economic sentiment indicator at 1000GMT, followed by German flash inflation at 1300GMT. In the US the release of the flash estimate of GDP will be closely watched at 1330GMT.

EZ ESI expected to decline

The EZ economic sentiment indicator is forecast to ease to 89.4 in January, following a small uptick in December to 90.4. Last month's uptick was driven by an improvement of industrial and consumer sentiment. On the other hand, retail trade and service sector confidence deteriorated further. While industrial sentiment is projected to remain unchanged in January, service sector sentiment is expected to decline further amid high infection rates and renewed lockdowns. The tight restrictions which are in place in most European countries are weighing especially on the service and retail trade sector. Market forecasts are in line with the recently released flash PMI data, which saw services PMIs shift further into contraction territory.

German inflation seen rising

After recording negative rates for five consecutive months, German inflation is expected to rise by 0.5% in January. The annual HICP fell by -0.7% in December, g the same rate as in November. Destatis noted that the German VAT cut was the main driver for negative inflation, but the temporary cut ended in December; hence inflation is likely to tick up again in January.

US GDP forecast to grow in Q4

U.S. GDP likely grew by an annualized 4.3% in Q4 after rebounding a record 33.4% in Q3, according to the Bloomberg consensus. Although the economy began to lose its footing in the last quarter of 2020 as Covid-19 infection rates picked up again, momentum from earlier months should keep GDP growth positive.

The events calendar remains quiet on Thursday with the only scheduled speakers being ECB's Andrea Enria and Isabel Schnabel.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.