Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

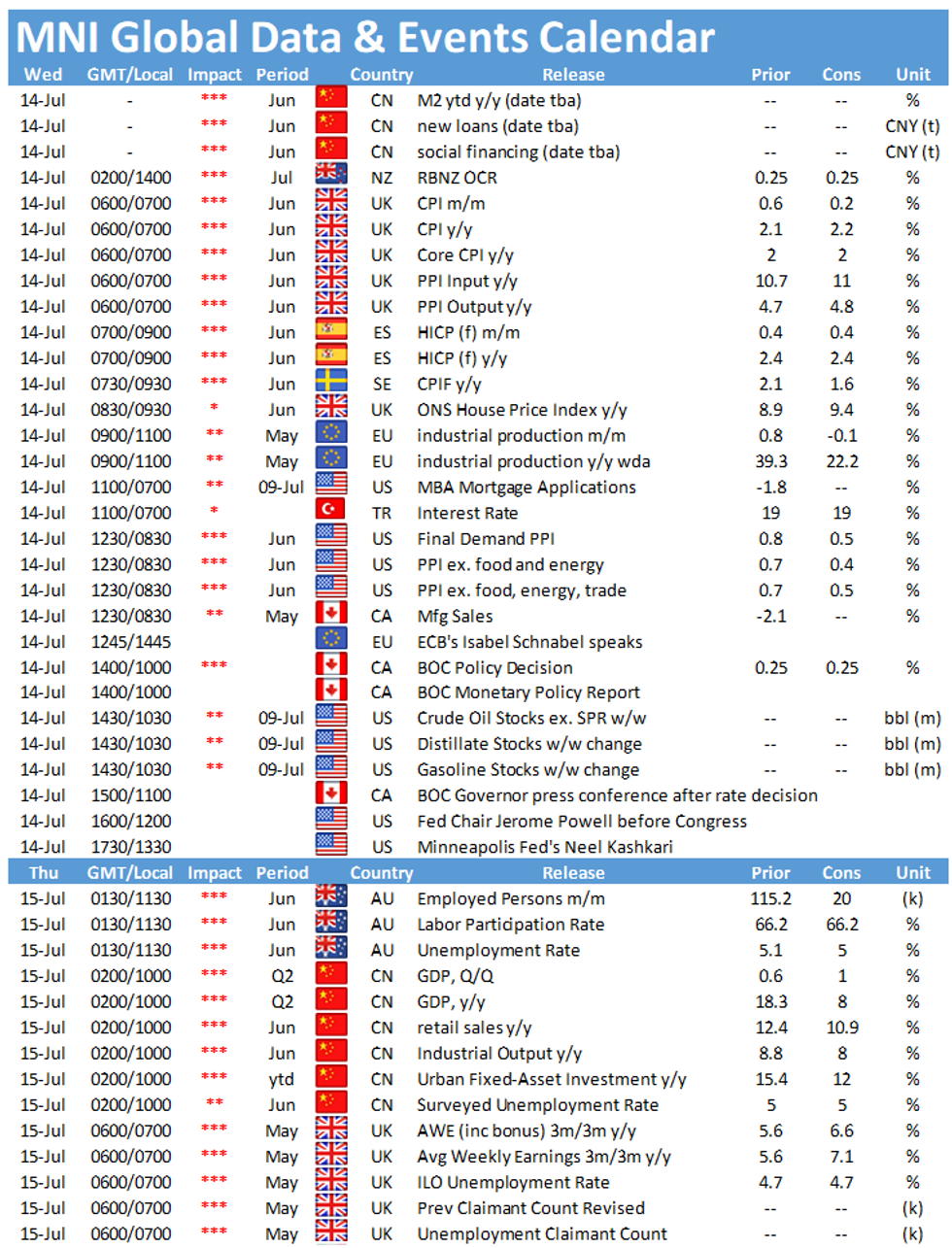

Wednesday morning starts with the release of UK inflation figures at 0700BST, followed by EZ industrial production at 1000BST. The main data event in the US is the publication of the producer price inflation at 1330BST.

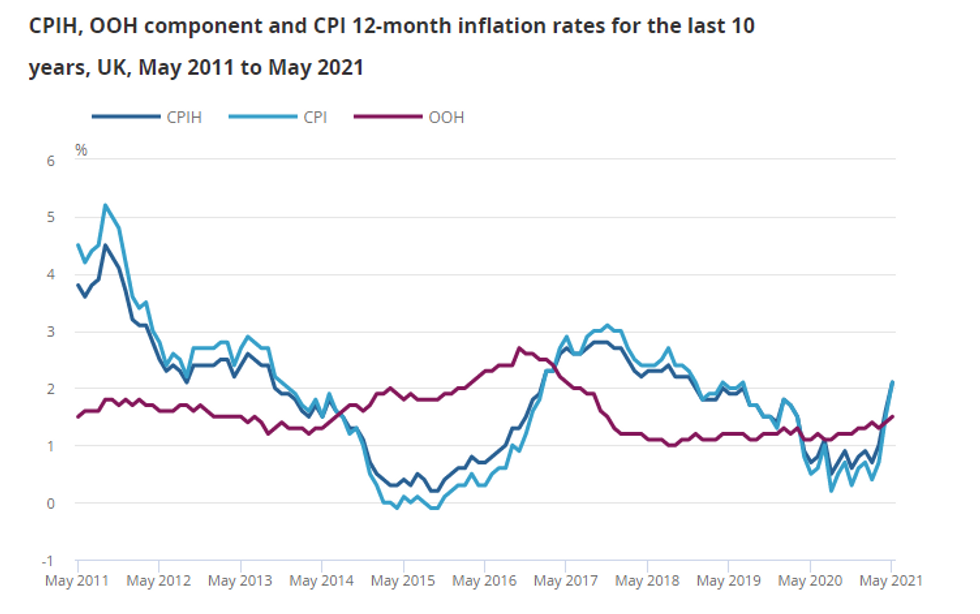

UK consumer prices expected to rise

Inflation is expected to edge slightly higher in June to 2.2%, up from 2.1% seen in May, while monthly inflation is seen slowing to 0.2%. In May, the CPI rose above the BOE's target for the first time since July 2019 and June's increase would mark the highest level since November 2018. The move will see prices move further away from the Bank of England's 2% target, but the Monetary Policy Committee has already said it will look through what it sees as transitory inflation.

The largest upward contribution in May came from transport prices, which are likely to remain elevated again in June. Prices for services are likely to pick up as well as the economy is reopening further and pent-up demand is released. The BRC shop price index saw a small dip of prices in June, however the report noted that costs for retailers are mounting and that these higher costs may be passed on to consumers in the month ahead.

Input price inflation is released as well Wednesday and markets forecast another increase to 11.0%, as supply bottlenecks and disruptions persist. The manufacturing PMI noted that input costs rose at a record pace as demand continues to outstrip supply and logistical issues as well as material shortages remained a problem. The survey saw an increase in selling prices as well as higher input costs were passed on.

Source: Office for National Statistics

EZ industrial production seen rising

Industrial production rose by 0.8% in April, marking the second successive gain. In May, markets are looking for a small downtick by 0.1%. Consumer durable goods and energy output saw the largest gains in April, while non-durable consumer goods production was the only category to post a decline.

Already available state-level data suggests a small downside risk in May as the three largest economies reported a monthly decline. German and French industrial production each decreased by 0.3% in May, while the Italian index was down 1.5%. On the other hand, Spanish monthly production rose by 4.3% in May.

Annual US PPI forecast to increase further

The annual US producer price index jumped to a record high of 6.6% and markets expect the index to rise further to 6.7%. May's increase was mainly driven by a sharp increase in final demand for goods, while final demand for services rose modestly. Monthly producer prices are projected to decelerate to 0.5% in June, after rising by 0.7% in May.

Survey evidence is in line with market forecasts. As global material shortages, logistical problems and supply chain disruptions persist, input costs for producers rise markedly again in June, according to the IHS manufacturing PMI. The ISM manufacturing PMI saw the price index surge to the highest level since 1979 in June.

The main events to look out for on Wednesday include speeches by ECB's Isabel Schnabel, Fed's Jerome Powell and Minneapolis Fed's Neel Kashkari. Additionally, the press conference following the BOC's interest rate decision will be closely watched.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.