Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

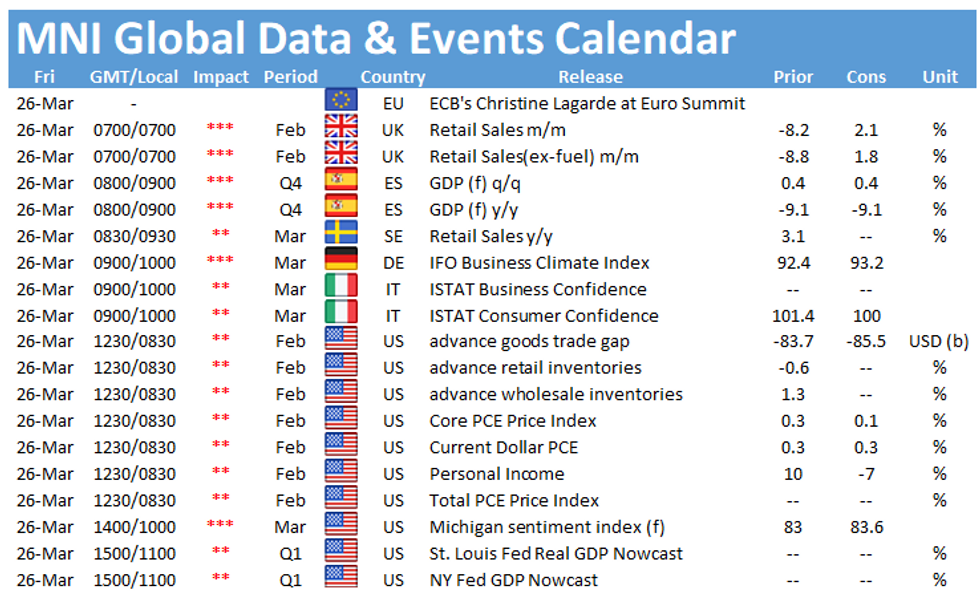

The week ends with several data events of note including the publication of UK retail sales at 0700GMT, followed by the Ifo business climate indicator at 0900GMT. In the US, the release of the final Michigan Sentiment index at 1400GMT will be closed watched.

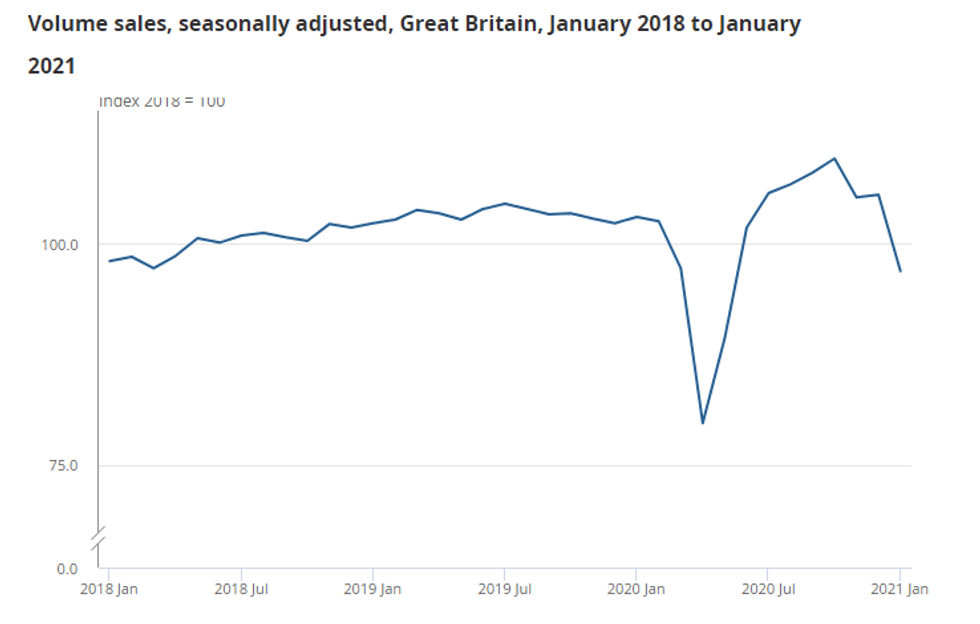

UK retail sales forecast to rebound

Following January's sharp decline in retail sales due to the national lockdown, markets expect the indicator to rebound to 2.1% in February, with the latest MNI Reality Check pointing to a possible outperformance. Annual sales are projected to improve to -3.6% in February, up from -5.9% in the previous month. January sales were 5.5% lower than before the pandemic, but the third lockdown had a significantly smaller effect on sales than the first the lockdown. All sectors saw a monthly decline in January, except for non-store retailers and food stores. Looking ahead, sales are likely to rise significantly in the coming months due to the reopening of non-essential shops and hospitality. The CBI distributive trades survey signalled optimism as well for April, while the BRC retail sales monitor already recorded rising sales in February.

Source: Office for National Statistics

Ifo business climate seen higher

The headline Ifo business climate indicator is forecast to rise further in March to 93.2, which would be the highest level since September, only slightly below the pre-pandemic level. Both the current situations index as well as expectations are expected to improve in March as covid-restrictions have been slightly eased at the beginning of the month. However, since then troubling news have increased. Infection rates are rising, and the lockdown has been prolonged to April, which bodes ill with a further recovery in the near-term.

Final Michigan Sentiment Index expected to rise

The final print of the Michigan consumer sentiment index is projected to come in slightly better than the preliminary estimate suggested. Markets look for a 0.6pt uptick to 83.6 in March compared to the first estimate. According to the preliminary estimate, consumer sentiment rose to a one-year high in March, which was mainly driven by the increasing number of vaccines and the relief measures. Survey evidence suggests an upbeat outlook as well. The IHS flash services PMI rose to a 80-month high and the report noted that looser restrictions led to stronger client demand.

The main events to look out for on Friday include the following speakers: ECB's Christine Lagarde as well as BOE's Michael Saunders and Silvana Tenreyro.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.