Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

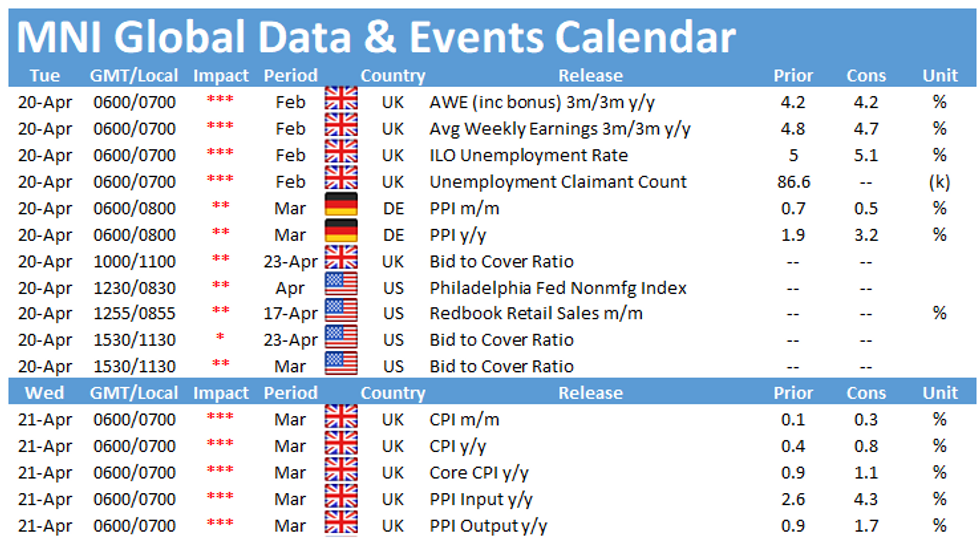

Tuesday kicks off with the release of German producer price inflation and the UK labour report, both released at 0700BST. The highlight of the day in the US is the release of the Philadelphia Fed nonmanufacturing business outlook survey at 1330BST.

German producer prices seen accelerating

Annual producer price inflation jumped to 1.9% in February, up from 0.9% seen in January and marking the highest level since May 2019. The annual PPI is forecast to rise further in March with markets looking for an increase to 3.2%, which would be the highest level since November 2018. A sharp uptick in intermediate goods prices, was the main driver for February's increase. Destatis noted that intermediate goods inflation was mainly led by a 46.6% y/y increase in prices for secondary raw materials. Survey evidence for March suggests ongoing supply chain issues, which led to higher prices for raw materials.

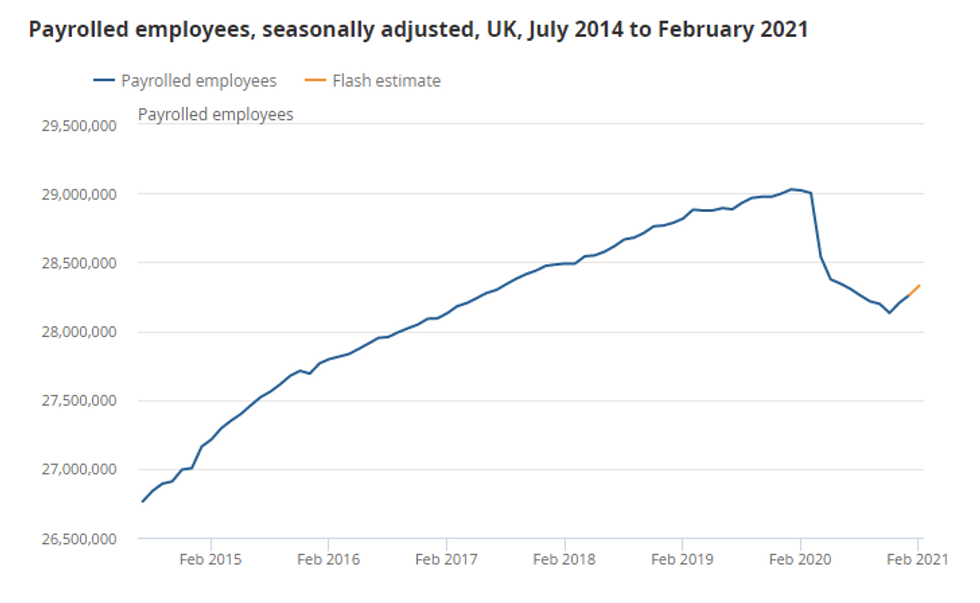

UK unemployment rate seen slightly higher

The UK's jobless rate edged slightly lower in January to 5.0% and markets look for a small uptick to 5.1% in February. More up-to-date PAYE data showed an increase in the number of payrolled employees in February, which bodes well with future gains of the employment rate. January's report saw the growth rate of vacancies slowing and actual hours worked declining slightly.

However, the KMPG/REC jobs report signals a strong increase of vacancies at the end of the first quarter, ahead of the planned reopening of non-essential businesses and hospitality. The services PMI saw an increase of employment for the first time since the start of the pandemic and the steepest rate of job creation since June 2019. The successful vaccination program and the continued easing of restrictions should provide a boost to the labour market going forward

Philadelphia Fed nonmanufacturing index surged in March

The general activity index of the Philadelphia Fed nonmanufacturing survey rose 26 points to 33.5 in March, which is the highest level since the start of the pandemic. March's increased was broad-based with both new orders and sales/revenues rising markedly. Moreover, the employment index improved, while the price index edged down. The future activity index of the survey continues to indicate growth over the next six months.

There are no speeches scheduled for Tuesday.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.