Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

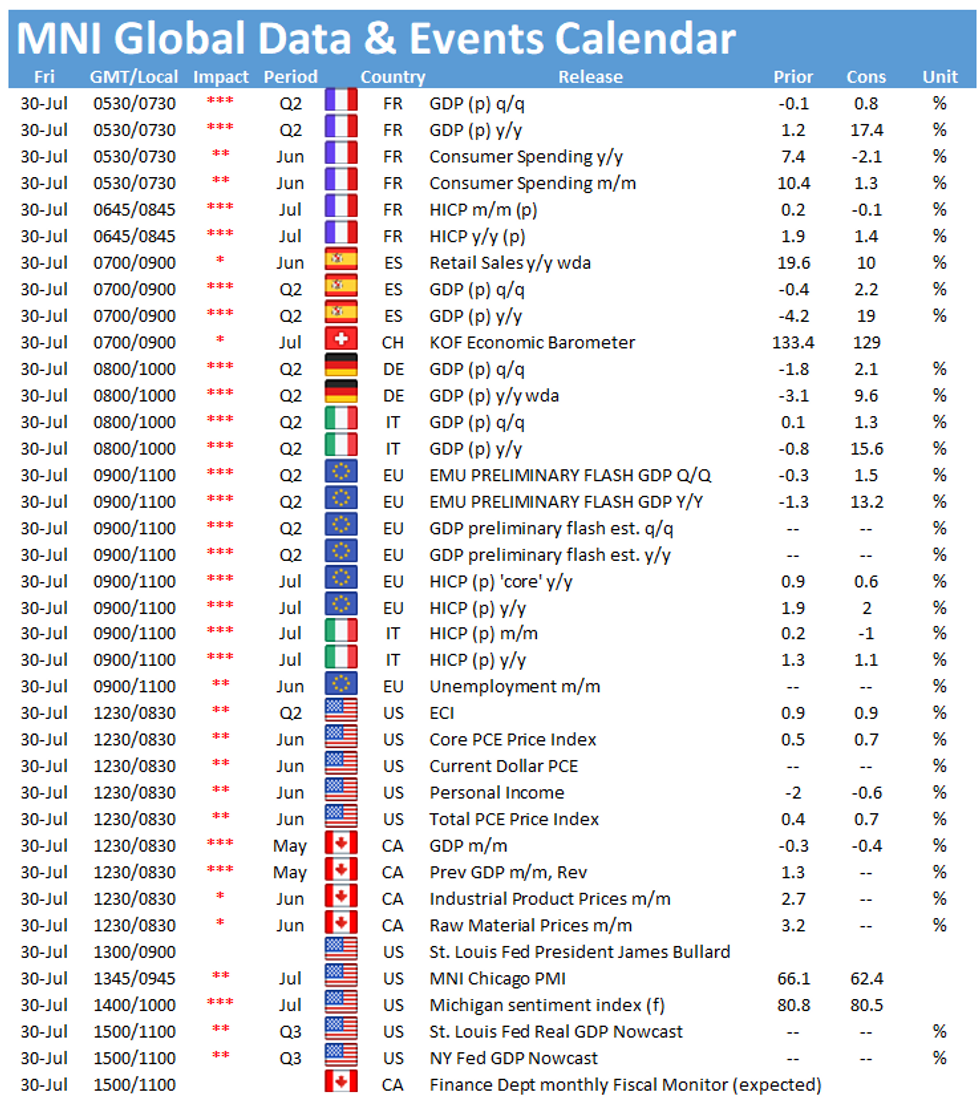

The main data releases in Europe Friday include flash GDP figures for France (0630BST), Spain (0800BST), Italy and Germany (both at 0900BST) as well as the EZ (1000BST). Additionally, the release of EZ flash inflation will be closely watched at 1000BST. The highlight in the US is the release of the employment cost index at 1330BST.

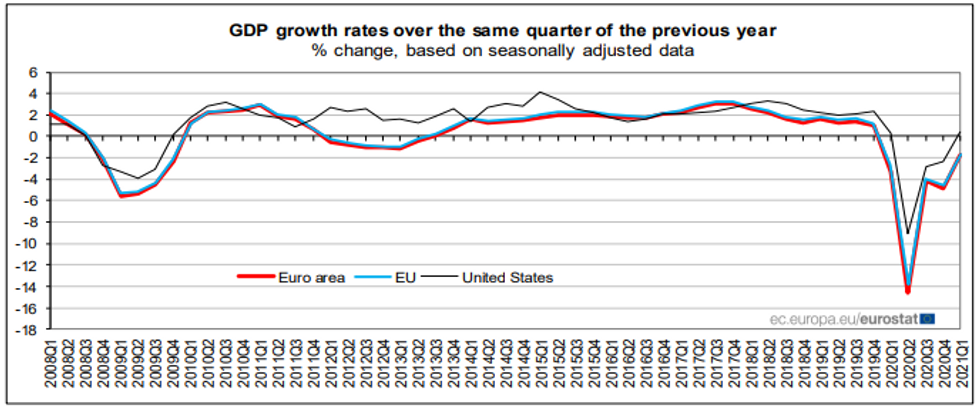

Economic growth forecast to rise in Q2 in Europe

The end of the second quarter was marked by the easing of covid-restrictions. While April was still difficult in many countries regarding infection rates and restrictions, May and June saw a rapid loosening of restrictions and a relaxation of the pandemic. As a result, economic growth in the second quarter should see a solid increase across the Eurozone. Markets expect French Q2 GDP to rise by 0.8%, while German growth is seen at 2.1%. The Italian economy is projected to expand by 1.3% and the Spanish by 2.2% in Q2. On aggregated eurozone level, economic growth is seen at 1.5% in the second quarter. Annual growth rates are likely to post very high levels as Q2 2020 saw historic declines due to the pandemic.

Source: Eurostat

EZ inflation projected to rise

Flash inflation in the EZ is expected to rise by 2.0% in July, after easing marginally to 1.9% in June. However, core inflation, once again a key focus for Frankfurt policymakers, is expected to slow to 0.7% y/y from 0.9% in June.

June's deceleration was led by a weaker growth rate of energy and service prices. Base effects due to the German VAT cut in 2020 are likely to push up EZ headline inflation in the coming months. Additionally, supply chain disruptions and bottlenecks put further pressure on consumer prices. The impact of temporary factors is expected to fade by the start of next year.

US employment cost index seen increasing

The employment cost index likely increased 0.9% in Q2, according to Bloomberg, following another 0.9% gain in Q1.

This quarter's release should be of particular interest to those following movements in U.S. wages, as things like hiring bonuses, which aren't included in monthly employment data from the BLS, will appear here, potentially pushing up compensation costs.

The only speech scheduled on Friday is St. Louis Fed's James Bullard speaking at the European Economics and Financial Centre.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.