Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

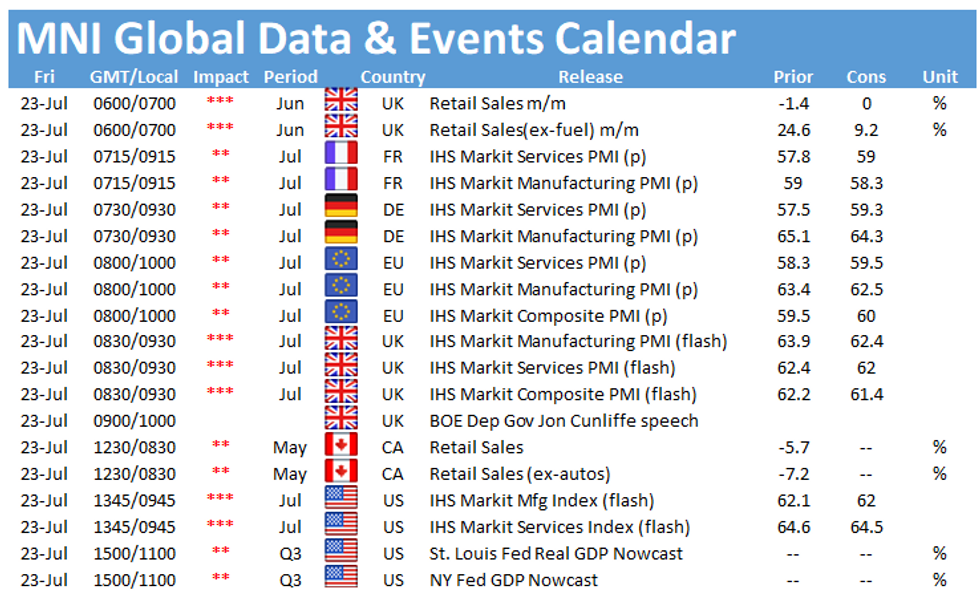

Friday kicks off with the release of UK retail sales at 0700BST, followed by the flash PMIs for France (0815BST), Germany (0830BST), the EZ (0900BST), the UK (0930BST) and the US (1445BST).

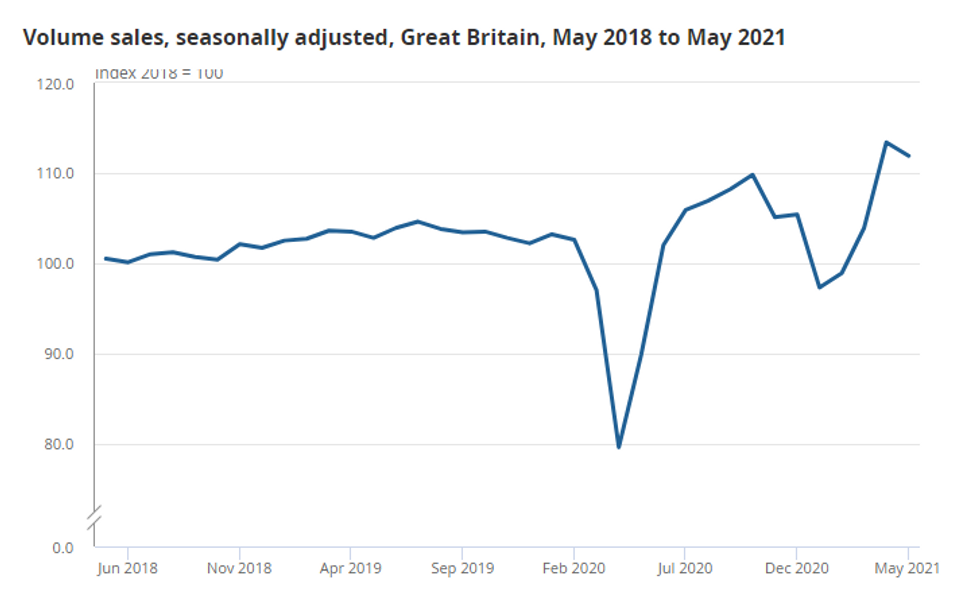

UK retail sales seen flat

UK retail sales are forecast to come in flat in June after dropping by 1.4% in May. However, May's retail sales were 9.1% higher than before the pandemic. Food sales showed the largest downward contribution in May as people returned to restaurants and bars.

MNI's reality check is in line with market forecasts, showing that retail sales remain subdued in June, as supply bottlenecks weigh on sales. On the other hand, the BRC shop sales monitor saw a solid increase of sales in June, linking it to pent-up demand.

Europe's flash manufacturing PMIs seen lower

The flash manufacturing PMIs for France, Germany, the EZ and the UK are all expected to tick down slightly in July. Although all four indicators are currently at very high levels and a small decline still leaves them comfortably above the 50-mark. Last month's surveys noted that supply chain issues persisted, and raw materials remained scarce, which drove up prices. There are no signs of a significant relaxation of these issues. As a result, business activity is forecast to ease slightly in July.

The French index is seen 0.7pt lower at 58.3, while the German manufacturing PMI is expected to drop to 64.3. The EZ index is seen at 62.5 and the UK's manufacturing PMI is expected to fall 0.9pt to 62.5 in July.

Europe's flash services remain in expansion

The flash services PMIs for France, Germany and the EZ are all expected to edge higher in July, while the UK's index is seen slightly lower. Service sector activity remains in expansion territory as the countries continue to ease restrictions and also allow for intra EU travel, which provides a boost to the tourism and hospitality sector. However, June's UK's report noted that staff shortages and capacity constraints led to a higher backlog.

In July, the French index is forecast to rise to 59.0, while the German PMI is seen at 59.3. The EZ services PMI is projected to increase to 59.5, while the UK's index is projected to edge slightly lower in July to 62.0.

US flash PMIs forecast to ease

Both the flash services and manufacturing PMI are expected to edge slightly in lower in July. While the manufacturing PMI is seen 0.1pt lower at 62.0, the services PMI is projected to fall to 64.5. Both indicators remain well above the 50-mark, signalling expansion. June's manufacturing PMI report noted that output and new orders rose markedly, but supply chain disruptions worsened and weighed on production capacity. Meanwhile, June's services PMI noted the difficulty in finding suitable staff and a sharp increase in the backlog of work. However, business confidence improved further.

The events calendar remains quiet with no speeches scheduled on Friday.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.