Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

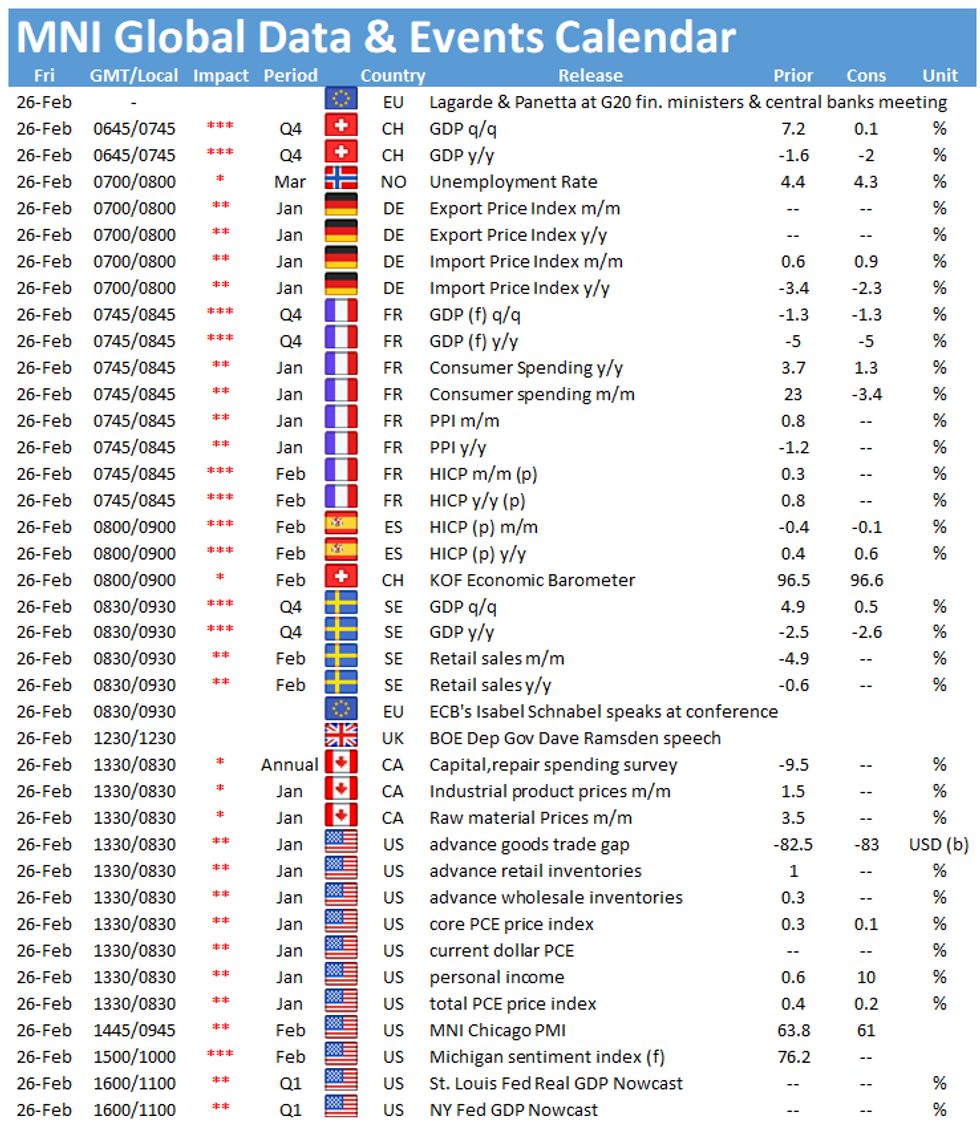

The main releases Friday morning include final French GDP and flash inflation, both released at 0745GMt. The highlight in the US is the release of the Chicago Business Barometer at 1445GMT.

Final French GDP expected to register at flash result

According to the flash estimate, the French economy contracted by 1.3% in the last quarter of 2020 as the second wave of Covid-19 led to renewed tight restrictions and hence to a decline in business activity. Annual growth was estimated at -5.0%. Markets are looking for the final print to confirm the flash result. Despite tight restrictions, the decline was not as severe as in Q2. Household consumption took the largest hit in Q4, falling by 5.4%, following Q3's strong rebound of 18.2%. Government consumption eased as well, down 0.4%, while net trade contributed positively to growth with exports rising by 4.8% and imports edged up 1.3%. The outlook for Q1 remains subdued as tight restrictions are still in place and infection rates remain elevated.

French inflation forecast to decelerate

Inflation rose markedly in January to 0.8%, up from a flat reading seen in December. January's uptick was broad-based with food inflation and tobacco prices rising at a faster pace, while prices for manufactured goods rebounded sharply. Energy prices fell at a slower pace. Annual inflation is forecast to slow to 0.5% in February, while the monthly rate is seen at -0.3% after having risen by 0.3% in January. The flash composite PMI noted that firms continued to cut output prices in February, despite a rise in input prices.

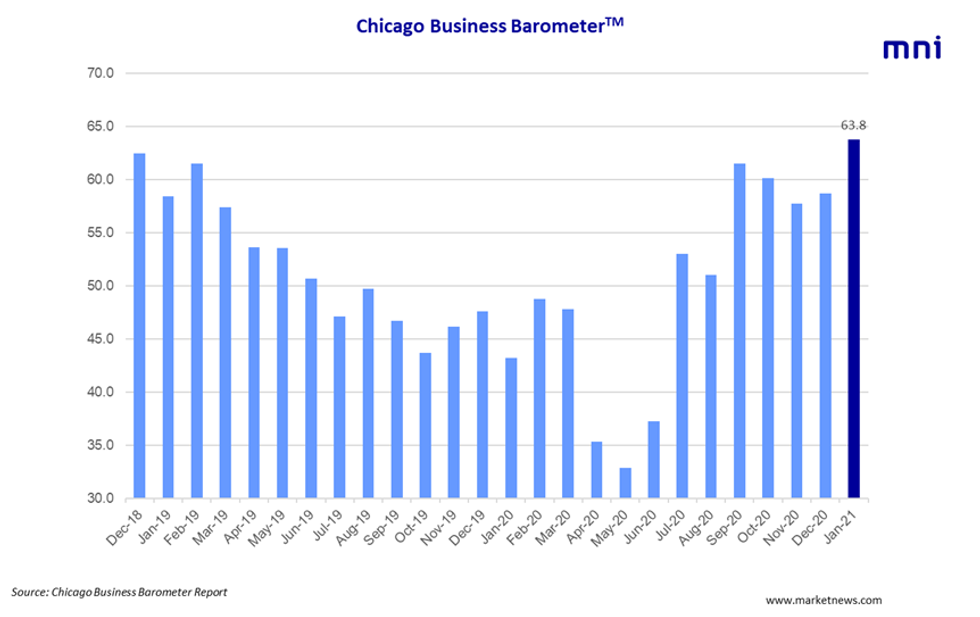

Chicago Business Barometer seen lower

The Chicago Business Barometer jumped to 63.8 in January, its highest level since June 2018. January's increase was boosted by a sharp rise of Production and New Orders as well as Order Backlogs. On the other hand, Employment and Supplier Deliveries declined. However, Supplier Deliveries remain elevated due to supply chain disruptions. In February, markets are looking for a dip to 61.0, after two consecutive months of gains. Similar survey evidence provides a mixed picture. While the Philadelphia Fed manufacturing index decreased in February, the Dallas Fed business activity index and the Empire State manufacturing index rose sharply.

The main events to follow on Friday include speeches by ECB's Isabel Schnabel and BOE's Dave Ramsden. Moreover, ECB's Christine Lagarde and Fabio Panetta are participating in G20 finance ministers and central banks governors meeting.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.