Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

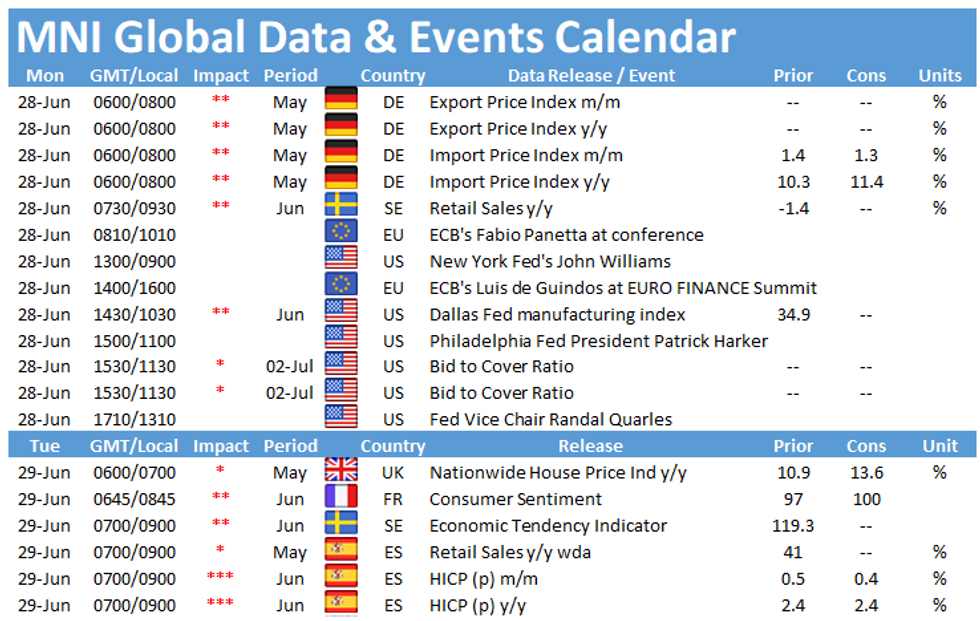

Its a quiet start to a busy data week, with Monday's only releases of note in Europe being the publications of German import and export prices at 0700BST and Swedish retail sales figures at 0830BST. In the US, the highlight of the day is the publication of the Dallas Fed manufacturing survey at 1530BST.

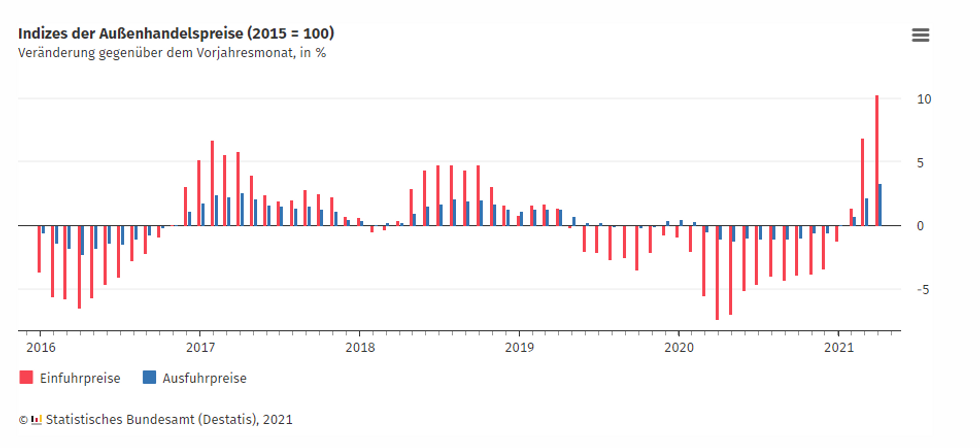

German import price index expected to tick up

The annual import price index rose sharply in April by 10.3%, hitting the highest level since December 2010. The import price index already jumped to 6.9% in March, after rising modestly by 1.4% in February. Monthly import prices increased by 1.4% in April. Destatis noted that energy prices are the source of the increase of the import price index. Prices for energy imports soared by 101.3% in April due to base effects. Markets are looking for another increase in May to 11.4% for annual import prices, while monthly prices are seen at 1.3%.

The flash composite PMI reported another increase in input price inflation in June, after showing a record high in May and suggesting an upside risk to the import price index.

Source: Destatis

Swedish retail sales fell in April

Retail sales dropped by 1.4% in April, as both durables (-2.6%) and consumables (-1.3%) posted monthly declines. Annual sales rose by 7.2% in April, reflecting strong declines seen at the beginning of the crisis. After rebounding sharply at the beginning of the year, the growth rate of monthly sales slowed in February and ticked up slightly in March, before April's drop.

May's Economic Tendency survey showed a decline in retail trade confidence in May and sales are expected to fall further over the next three months, which bodes ill with retail sales.

Dallas manufacturing index edged lower in May

The general business activity index eased slightly in May to 34.9, but remains well above the long-term average of 2.6. May's survey noted business activity continued to expand, although at a slower pace than in the previous month. Supply chain disruptions are likely to persist in June, as indicated by the recent release of the IHS flash manufacturing PMI. The PMI report noted that delivery times lengthened to a new record high and input prices soared once again.

The main events to follow on Monday include speeches by ECB's Fabio Panetta and Luis de Guindos as well as New York Fed's John Williams, Philadelphia Fed's Patrick Harker and Fed's Randal Quarles.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.