Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

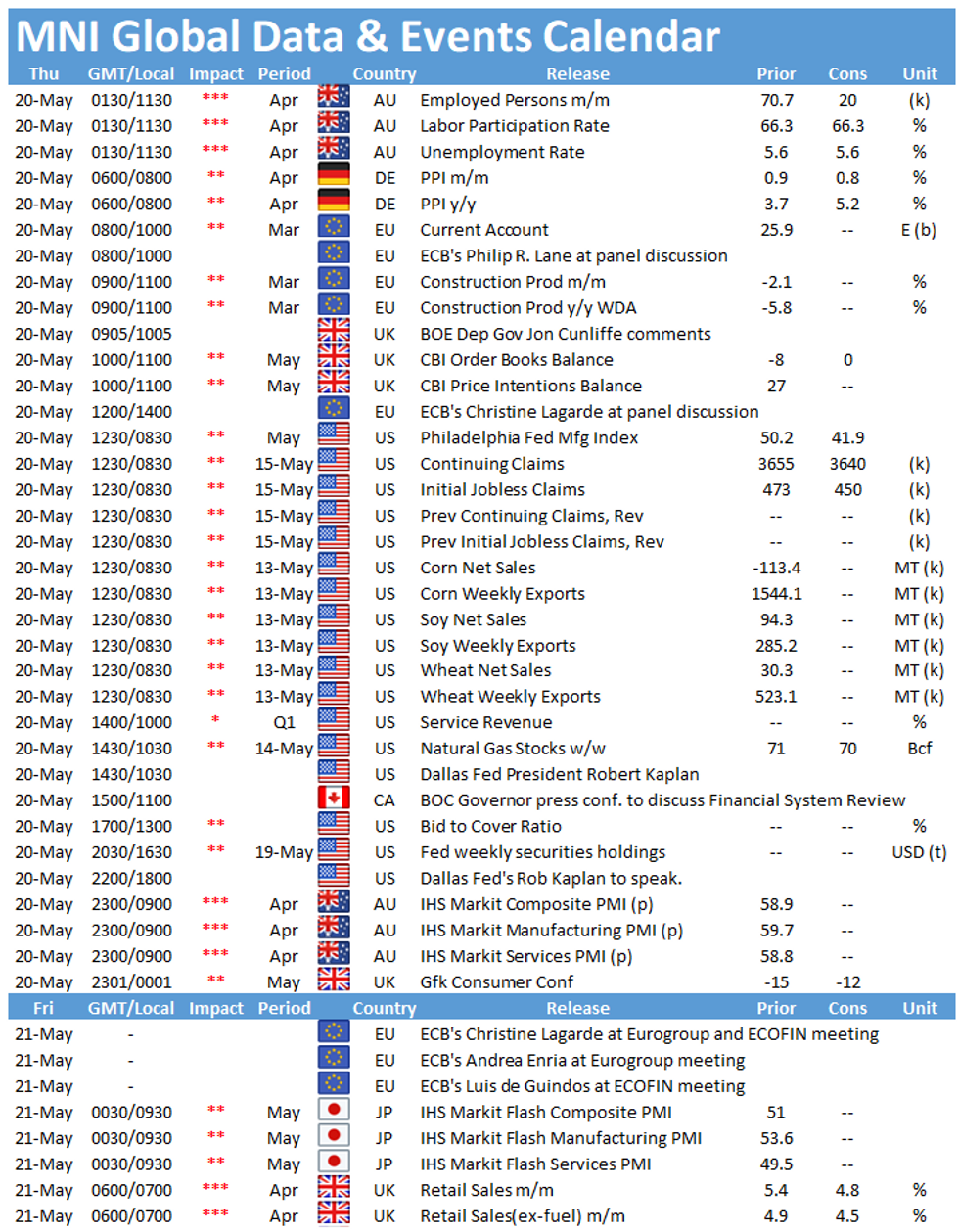

The main data in Europe Thursday include the release of German producer price inflation at 0700BST, followed by CBI industrial trends survey at 1100BST. In the US, the focus is again on the publication of initial jobless claims at 1330BST.

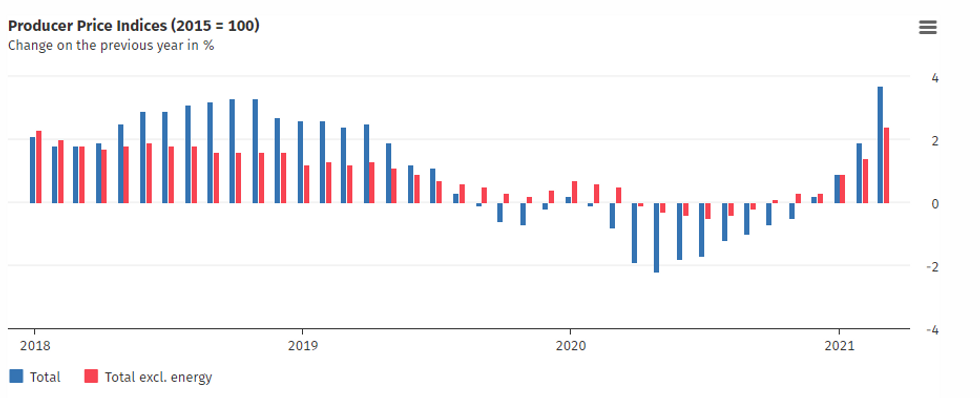

German PPI forecast to rise further

Producer price inflation increased markedly in March, rising by 3.7% on an annual basis. March's uptick was the sharpest increase since November 2011 (4.6%) and the fourth consecutive positive reading. The main drivers of March's gain were energy inflation and intermedia goods prices. Excluding energy, PPI increased by 2.4% in March. Destatis noted that energy inflation was led by higher electricity prices and CO2-pricing on several products. Moreover, raw material shortages led to higher prices for metallic secondary raw materials which rose 46.8% compared to March 2020.

In April, markets expect the annual PPI to rise further to 5.2%, which would be the highest level since August 2011 (5.2%). Survey evidence suggests that supply chain disruptions remain an issue and continue to drive up input as well as output prices. April's manufacturing PMI report again noted shortages of raw materials and components and difficulties regarding freight capacity as well as disruptions from the Suez Canal blockage.

Source: Destatis

CBI Trends total orders expected to improve

Monthly CBI order books deteriorated slightly in April to -8, down from -5 seen in March. Nevertheless, the indicator registered above the long-term average of -14. In May, markets look for an increase to 0, which would be the highest level since March 2019 (+1). Quarterly orders and output in Q1 improved markedly and manufacturing sentiment rose at the fastest pace since 1973, reflecting the growing optimism regarding the output.

US jobless claims seen slowing further

Claims filed through May 15 are set to dip to 450,000 from 473,000 through May 8, a pandemic low. Initial claims have been trending downward in recent weeks as the labor market gradually improves.

Continuing claims through May 8 should fall to 3.64 million, according to Bloomberg, following the previous week's 3.65 million.

The events calendar throws up several interesting speeches on Thursday. The main speakers to follow include ECB's Philip Lane and Christine Lagarde as well as BOE's Jon Cunliffe and Dallas Fed's Rob Kaplan.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.