Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

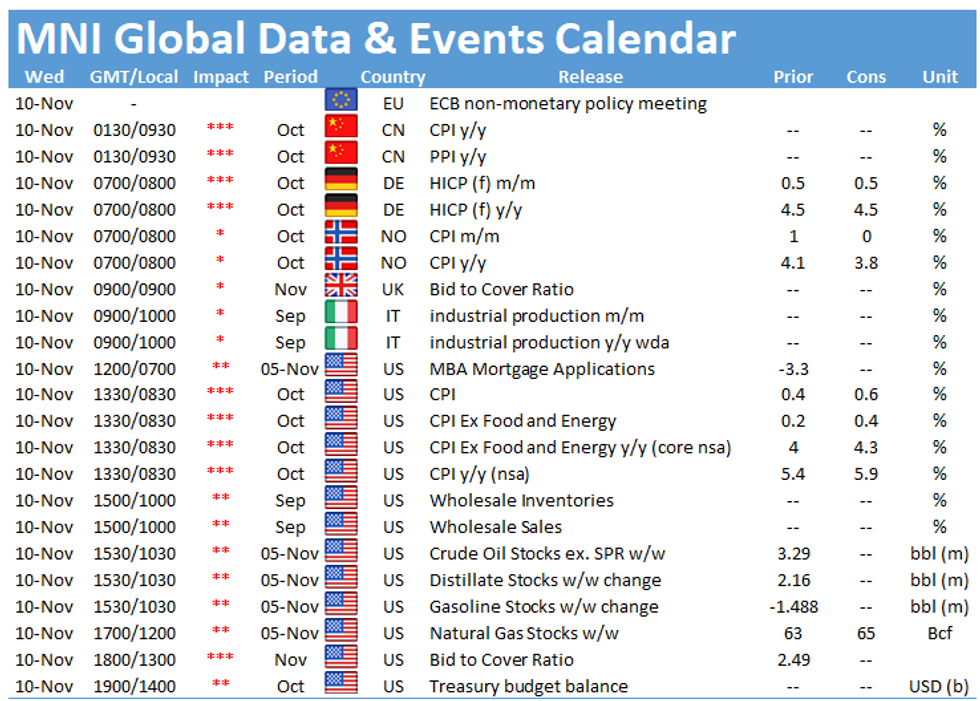

Inflation data is the headline news Wednesday, with US. data following on from stronger-than-expected numbers overnight in China.

No Respite For Fed As US Consumer Prices Set For Further Rise (1330 GMT)

Forecasters see further upward pressure on US consumer inflation in October and highlight the potential market threat of accelerated tapering by the Fed and even an eventual move to pull forward rate hikes.

With energy prices continuing to accelerate, headline CPI inflation is geared towards an increase on all fronts, with the monthly CPI expected to rise from 0.4% in September to 0.6% for October. Similarly, core CPI is set to accelerate from 0.2% to 0.4% previously, particularly influenced by the expansion of COVID-19-sensitive key demand products including automobiles and apparel, according to some analysts.

As such, market forecasts point to another solid rise in the annual CPI, reaching 5.9% in October up from 5.4%. It the headline rate comes in at that level, it will be the highest level since inflation peaked just above 6% in the early 1990's. Following suit, the core annual CPI is set to increase to 4.3% compared to 4.0% y/y in September.

US Annual CPI (%) over last 40 years

Source: Bloomberg

US Initial Claims set to fall to post-Covid low (1330 GMT)

US initial claims, being published a day early due to the Veterans' Day holiday Thursday, are likely to show a further decline to a fresh post-Covd low according to analysts. Weekly claims are expected to dip to 260,000, down from 269,000 last week and well below the levels above 6.1 million seen in the early days of the pandemic back in early spring 2020.

Continuing claims are also expected to decline, falling to 2.05 million from 2.105 million previously.

There are few speakers slated for Wednesday, but BOE MPC member Silvana Tenreyro is set for a 'fireside chat' with former US Treasury Secretary Larry Summers, discussing 'secular stagnation' post-Covid.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.