Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI (Washington)

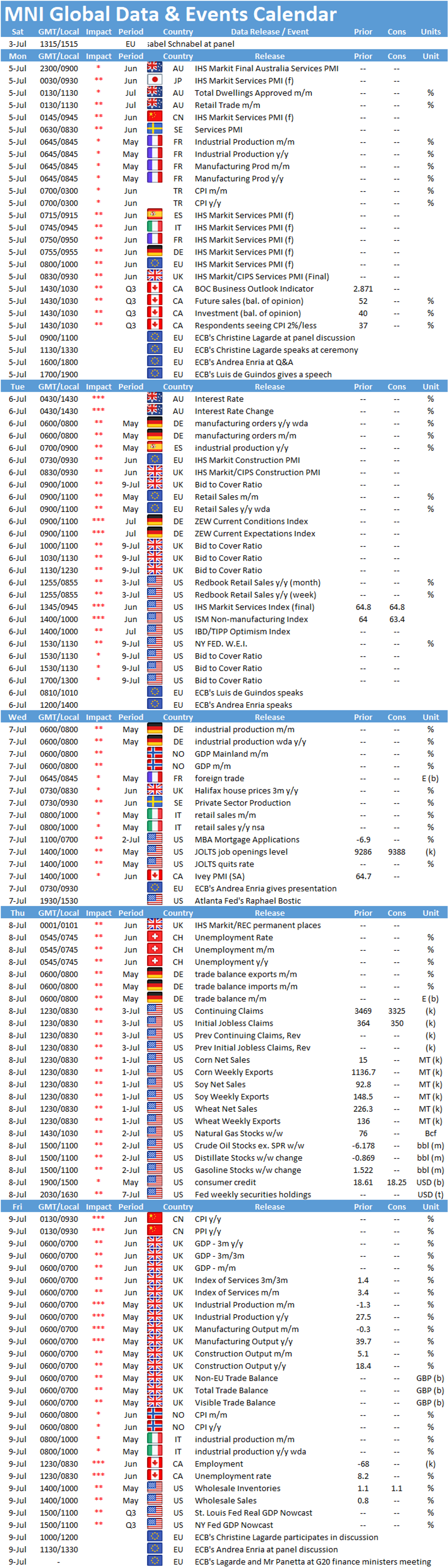

Key Things to Watch:

- Monday, July 5 – UK Services PMI

- According to the flash services PMI business activity growth is slowing in June. The flash services ticked down to 61.7 in June, down from 62.9 recorded in May. Nevertheless, the index still signals strong expansion of the service sector, driven by the easing of restrictions and higher demand. Markets expect the final reading to register in line with the flash estimate.

- Employment improved further in June, with the rate of job creation being only slightly below the record registered 7 years ago. Similar to the manufacturing sector, input prices are rising further in June, which also led to a new record high of selling prices.

- Tuesday, July 6 – Reserve Bank of Australia Policy Decision

- The Reserve Bank of Australia meets Tuesday with policymakers set to decide whether to extend the duration of its forward guidance, with deliberations clouded by fresh lockdowns in major cities after a resurgence of the pandemic and the spread of the Delta Variant of the Coronavirus.

- The key decision for the RBA is whether to extend its yield target on three-year Australian government bonds to the November 2024 series, a call that will based on the central bank's assessment of when that year it expects to raise interest rates from the current record low of 0.10%.

- The RBA has already said that it will continue with its program of buying longer dated Government bonds beyond the current AUD100 billion program ending in September, and will decide on what form that takes, with some speculation that policymakers could look to upscale QE from the anticipated AUD50 billion to AUD75 billion.

- Tuesday, July 6 – ISM Services PMI

- Service sector activity likely held steady through June, with the ISM Services Index forecast to dip just slightly to 63.5 from a record-high 64 in May, according to Bloomberg.

- Analysts say the index is likely to fall further in coming months as the effects of fiscal stimulus and reopenings fade but should still remain well above the 50 benchmark that signals expansion

MNI Washington Bureau | +1 202-371-2121 | brooke.migdon@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok