Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI (Washington)

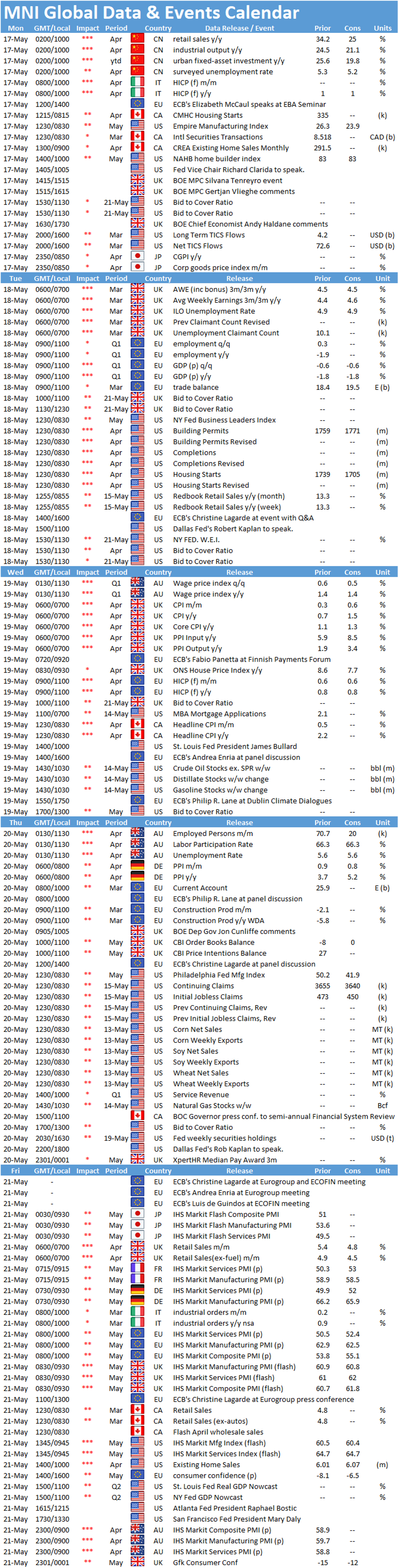

Key Things to Watch:

- Wednesday, May 19 – UK Inflation

- UK headline inflation likely jumped in April, pushed higher by a rise in domestic energy costs as price caps were raised along with strong upward pressure from base effects as year ago weak numbers drop out. The headline CPI is expected to rise sharply, hitting 1.4% y/y after 0.7% in March.

- Although a doubling in the headline number, CPI is set to remain below the Bank of England's 2% target for a 22nd consecutive month.

- Core inflation is also expected to edge higher, albeit at a slower pace without the energy price increase impact

- Wednesday, May 19 – Canada CPI

- It's Canada's turn to report breakaway inflation on comparisons to last year's plunge in gasoline prices. Companies in April also faced production bottlenecks and households went into a more severe third-wave lockdown than the U.S. or UK.

- The CPI accelerated to a 3.1% pace in April from a year earlier according to Montreal-based National Bank Financial. Inflation hasn't been 3% since July 2018 and hasn't exceeded that mark since 3.2% in September 2011.

- BOC Governor Tiff Macklem told reporters Thursday he's sticking with his forecast inflation will soon reach around 3% and later recede because some parts of the economy remain very weak. Inflation already jumped to 2.2% in March from 1.1% in February.

- Thursday, May 20 – U.S. Weekly Jobless Claims

- Claims filed through May 15 are set to dip to 450,000 from 473,000 through May 8, a pandemic low. Initial claims have been trending downward in recent weeks as the labor market gradually improves.

- Continuing claims through May 8 should fall to 3.64 million, according to Bloomberg, following the previous week's 3.65 million.

MNI Washington Bureau | +1 202-371-2121 | brooke.migdon@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok