Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

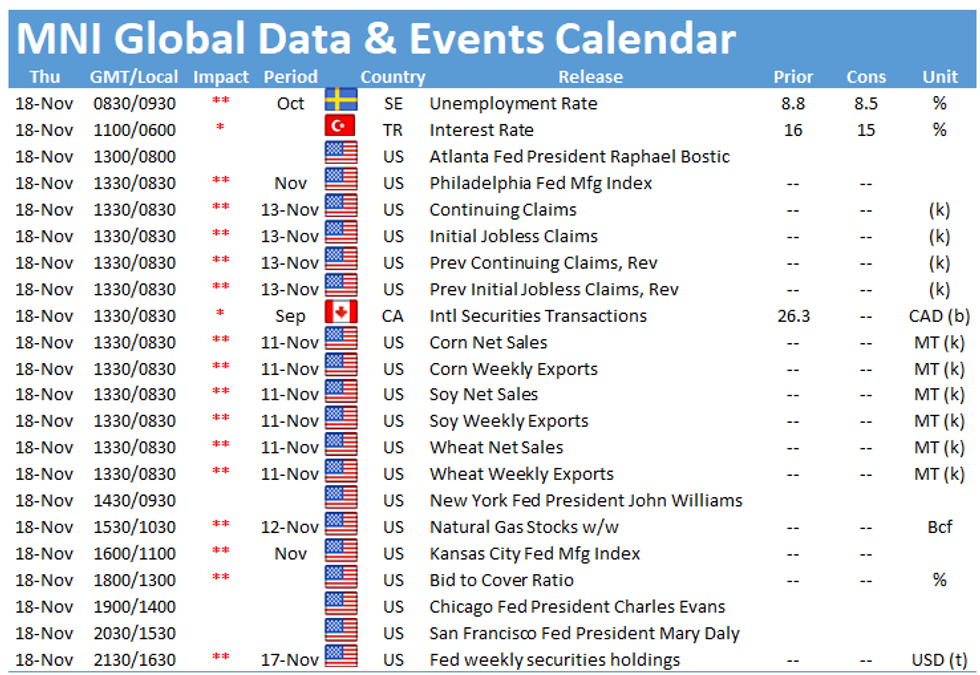

Thursday sees largely second tier economic data, with monetary policy decisions expected from Turkey and South Africa.

Turkey Central Bank set for 100 bps cut (1100GMT)

The CBRT is broadly expected to reduce its one-week repo rate by at least 100bps to 15.00% as the bank resumes its easing cycle against the EM trend. Here we see the majority of analysts taking Kavcioglu's guidance on limited room to cut rates at face value, justifying the relatively smaller cut relative to the 200bps shed last month, our emerging markets desk write.

However, with the bank's reaction function being less dictated by market conditions than political vectors, risks are unequivocally skewed towards a potentially larger cut.

US initial jobless claims continue to fall (1330GMT)

US initial jobless claims are expected to come in at a new pandemic low of 260k, down from 267k in the prior week, accord.

The reduction in jobless claims will be another step closer to the pre-pandemic March 2020 reading of 212k claims. Continuing claims are also set to fall, with the consensus forecasting 2.120 million for the week ending November 6, implying a reduction of 40k claims from the previous reading.

Prevailing labour shortages in the US are largely attributable to repercussions of career switches, increased unpaid care work and resistance to return to work. Nonetheless, the US labour market recovery provides a silver lining for the economy against a background of surging inflation as the Fed begins to taper purchases this month.

SARB on hold, upside risk on rates (1410GMT)

The SARB is at a key inflection point this week with market pricing diverging from a marginal consensus in favour of a hold at 3.50%. In light of the still-muted aggregate demand impulse, elevated unemployment and relatively benign medium-term inflation outlook, we retain our call for rates unchanged out to 1Q22 with Governor Kganyago cautious not to curtail SA's fragile recovery with CPI still within the 3-6% target range.

Policymaker speeches Thursday include NY Fed President John Williams, Chicago Fed's Charles Evans and SF Fed President Mary Daly.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.