Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Executive Summary:

- The NBH is likely to accelerate the pace of its tightening cycle and hike its policy rate by 100bps on June 28 as HUF weakness keeps supporting inflation expectations.

- The central bank is also likely to proceed with a 30bps in the 1W depo rate, which would increase the ‘effective’ policy rate to 7.55%.

- Geopolitical uncertainty (Russia 'default') has been weighing on the Hungarian forint, which fell to a new all-time low (vs. EUR) on Monday following the Russia headlines.

Link to full publication:

The National Bank of Hungary (NBH) is likely to accelerate the pace of its tightening cycle and hike its policy rate by 100bps on June 28, which would levitate the benchmark rate to 6.9% (highest since July 2012), as HUF weakness keeps supporting inflation expectations. The central bank is also likely to proceed with a 30bps in the 1W depo rate, which would increase the ‘effective’ policy rate to 7.55%.

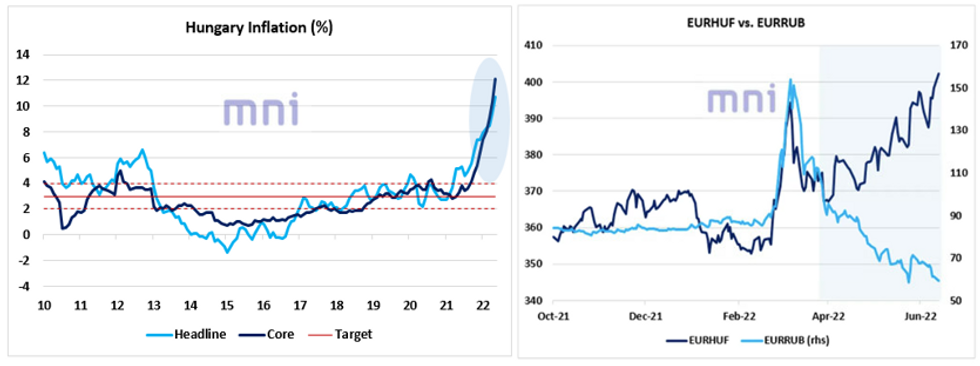

Inflationary pressures continue to rise in Hungary, with CPI accelerating to 10.7% in May (vs. 10.4% exp.), up from 9.5% the previous month, diverging significantly from the NBH 4-percent upper tolerance band (figure 1, left frame). Hungary officials reiterated on several occasions that inflation would be running a few ppt higher in the absence of price caps. For instance, PM Orban mentioned earlier this month that CPI inflation would be currently running at 15% / 16% in the absence of caps. As a result, the government has extended the caps on some basic food and fuel prices until October 1, and a cap on retail mortgage interest rates will remain in place until the end of the year. Sell-side analysts continue to revise their year-end inflation forecasts higher, currently estimated at 9.4% (vs. 7.7% in the beginning of May).

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.