Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

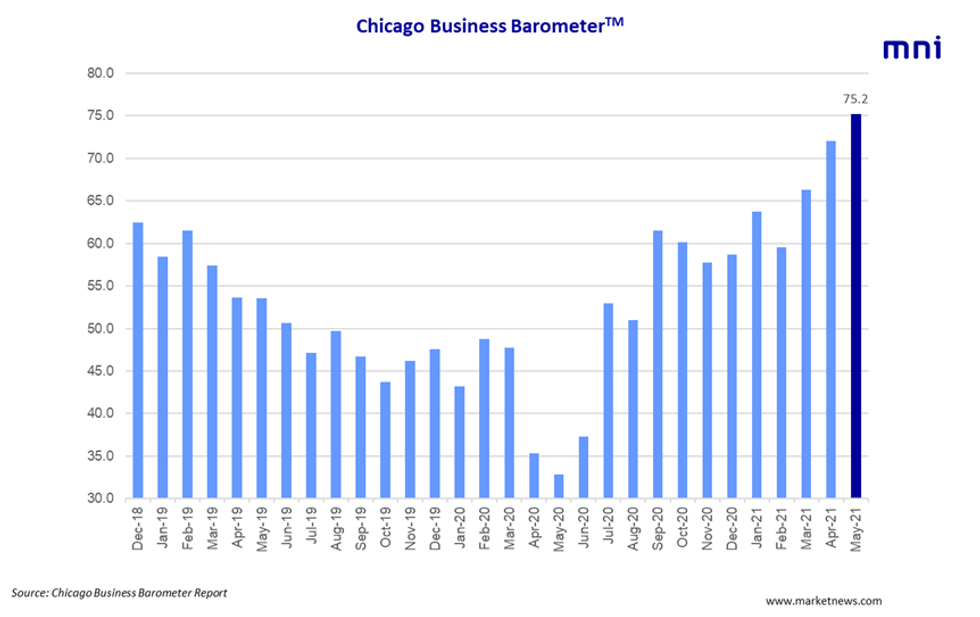

The Chicago Business Barometer rose sharply in May, with the headline index rising to 75.2 from 72.1 in April, driven by a solid gain in new business and order backlogs. May's reading marks the highest level since November 1973, beating market expectations for a downtick.

Among the main five indicators, New Orders and Order Backlogs saw the largest gains, while Employment recorded the only decline.

Demand remained strong in May with New Orders jumping to the highest level since December 1983. The index now stands at 80.0, up from 72.9 in April. Production slowed 2.3pt to 70.6. Anecdotal evidence signals strong consumer demand, partly due to the fear of raw material unavailability.

Order Backlogs jumped 7.5 points to 80.7, hitting a 70year high. Firms noted logistical issues and personnel shortages which are driving backlogs. Meanwhile, Inventories dropped to a 9-month low of 41.8, the second successive reading below the 50-mark.

EMPLOYMENT

May saw employment slip back into contraction territory, following two months of readings above 50. The indicator declined from 56.4 to 49.8 and firms indicated difficulties finding new staff.

Supplier Deliveries rose 5.9 points to a 47-year high of 82.3 in May with supply chain constraints remaining a serious problem. Companies continuously noted delivery delays due to transportation issues and material shortages. Prices paid at the factory gate fell to 88.4 in May, down from April's 41-year high of 91.5. However, several respondents said prices for commodities, such as steel, plastics, copper, or electronic components rose further.

This month's special question asked, "Considering the global shortage of computer chips, do you have contingency plans?" While the majority of 46.2% do not use the product, 28.2% have no plans in place. The second question asked about tensions due to the increase in global logistics and component shortages, with the majority looking to mitigate the risks.

This month's survey ran from May 3 to 18.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.