Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI US MARKETS ANALYSIS - Risk-On Underpins Bear Steepening

HIGHLIGHTS:

- Sovereign curves have bear steepened alongside gains for equities.

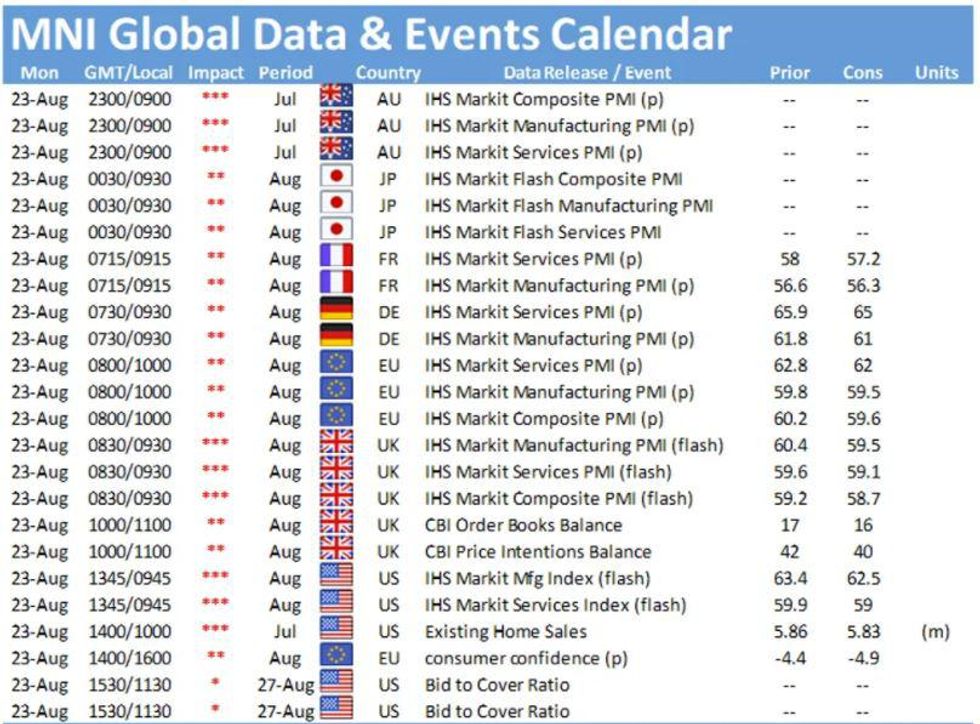

- Preliminary European PMIs for August Point To Sustained Economic Recovery

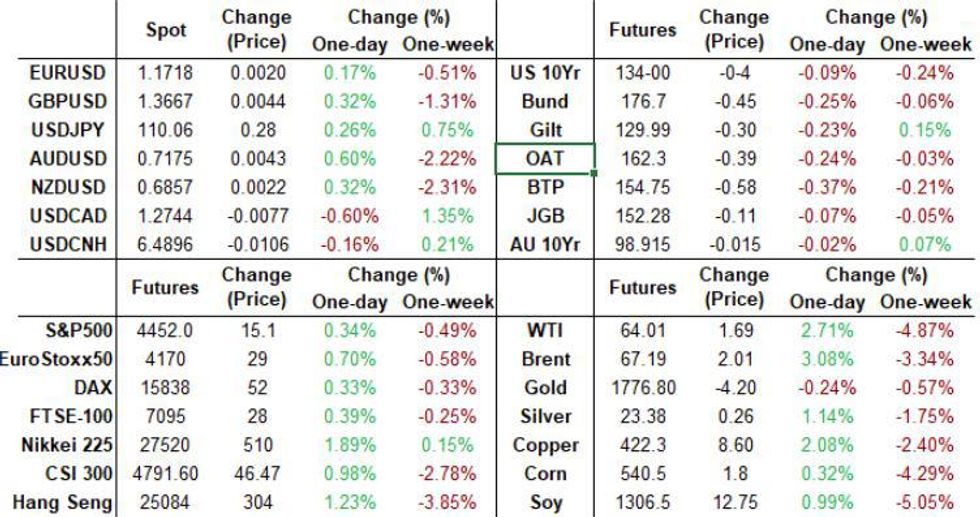

US TSYS SUMMARY: Bear Steepening Amid Risk On Move

The Treasury curve has bear steepened to open the week, with futures a little softer.

- A fairly risk-on Asia-Pac and European session, with equities rising and the dollar continuing to retrace from Friday's 2021 highs.

- The 2-Yr yield is up 0.6bps at 0.2303%, 5-Yr is up 1.6bps at 0.7981%, 10-Yr is up 2.2bps at 1.2768%, and 30-Yr is up 2.3bps at 1.8917%.

- Sep 10-Yr futures (TY) down 4/32 at 134-00 (L: 133-30 / H: 134-06). 133-29 is the Aug 18 low and support.

- Chicago Fed Nat Activity Index at 0830ET is followed by flash August PMIs at 0945ET, then existing home sales at 1000ET. Supply consists of $99B 13-/26-week bill auctions at 1130ET. NY Fed buys ~$3.225B of 7-10Y Tsys.

- No Fed speakers scheduled until Chair Powell at Jackson Hole on Friday (1000ET - the conference is now virtual vs in-person, as announced late Fri). BBG sources piece out over the weekend saying Treas Sec Yellen supports Powell's re-appointment.

- Some attention on the $3.5T budget resolution, with Democrats sparring internally about how to proceed. House Democratic leaders meet this afternoon, with Democratic Caucus meeting Tuesday 0900ET.

EGB/GILT SUMMARY: Risk-On Driving Govies Lower

European sovereign curves and have bear steepened and equities are broadly higher in a characteristically risk-on move.

- Preliminary PMI data point to a sustained expansion in economic activity in August. Even in the UK, where the services PMI missed by a significant margin (55.5 vs 59.1 survey), the data nonetheless indicates that the economic recovery is still underway.

- Gilts have traded weaker from the open cash yields 2-3bp higher on the day and the curve 1bp steeper.

- Bunds have marginally underperformed gilts with yields at the very long end up 4bp.

- It is a similar story for OATs where the 2s30s spread has widened by 3bp.

- BTPs have underperformed core EGBs with yields pushing up 2-5bp across the curve.

- Supply this morning came from Germany (Bubills, EUR3.045bn allotted). Later today France will offer EUR3.9-5.5bn of BTFs.

EUROPEAN SOVEREIGN ISSUANCE UPDATE

GERMANY AUCTION RESULTS: Germany Allots E3.045bn of 12m Bubills

- Average yield -0.6619%, Buba cover 3.2x, bid-to-cover 2.46x

EUROPEAN OPTIONS FLOW SUMMARY

RXU1 176/175/174 put fly, sold at 7 in 2k

RXU1 175.5/173.5ps, bought for 5 in 1.25k

RXV1 176/176.5/177/178 broken c condor, sold at 2 in 1.25k

RXV1 176c, bought for 12.5 in ~2.8k

RXX1 173/172ps 1x1.5, bought for 6 in 1.5k

RXX1 173p, bought for 68 and 69 in 5k

DUV1 112.30/20ps 1X4, sold at -1 in 1k

DUV1 112.20 put, bought for 1.25 in 5.6k

0LZ1 99.50/37/25 put fly, bought for 2.25 in 3k

FOREX: USD Underperforms Against the Majors

- USD has broadly been better offered, but crosses have mainly stayed within ranges, as investors focus on the European, UK PMI releases.

- The data were mixed across countries, whilst we are still printing into expansion, some of the release saw numbers above survey, but down versus last.

- The USD trades in the red against all majors, besides the Yen, on the back of underpinned Equity market, albeit off their best levels for the session.

- GBP saw some offers hitting the currency, after the UK PMI service missed expectation, but downside for the British Pound have been limited, with the currency taking its cue from the better offered Dollar.

- The EUR is mixed, down 0.62% against the NOK, and up 0.5% versus the Yen.

- EURGBP tested 0.8593 100-dma, printed a 0.85936 high)

- Above the latter opens to 0.8618 76.4% retracement of the Jul 20 - Aug 10 sell-off.

- Looking ahead, US PMIs will be the main focus, ahead of the awaited Jackson Hole on Friday.

- We have no speakers scheduled for today.

FX OPTION EXPIRY

FX OPTION EXPIRY:

Of note: EURUSD, light for today, but we have 1.23bn at 1.1700 (Thurs), and 1.3bn at 1.1700 (Friday)- EURUSD: 1.1750 (210mln)

- USDJPY: 110 (211mln), 110.10 (220mln), 110.25 (400mln)

- USDCNY: 6.45 (331mln)

Price Signal Summary - S&P E-Minis Holds Onto Gains

- On the equity front, S&P E-minis have recovered from recent lows of 4347.75, Aug 19 low. Importantly, last week's low and rebound, means the 50-day EMA remains intact. This average intersects at 4347.46 and represents a key support area. Attention is on the bull trigger at 4476.50, the Aug 16 high. EUROSTOXX 50 last week probed its 50-day EMA. Key support has been defined at 4078.00, Aug 19 low.

- In the FX space, the USD remains in an uptrend and current weakness is considered corrective. EURUSD last week cleared 1.1704, Mar 31 low. This signals scope for a move to 1.1621 next, 1.00 projection of the Jan 6 - Mar 31 - May 25 price swing. Firm resistance is at 1.1805, Aug 13 high. GBPUSD remains vulnerable and the focus is on key support and the bear trigger at 1.3572, Jul 20 low. USDCAD resumed its uptrend last week but did stall at 1.2949, the Aug 20 high. The trend remains bullish with the focus on 1.2976, 1.00 projection of the Jun 23 - Jul 19 - 30 price swing. Note, Friday's price pattern is a bearish shooting star candle and a concern for bulls - watch support at 1.2649, Aug 19 low.

- On the commodity front, Gold remains firm with the focus on the next important resistance at $1796.5, the 50-day EMA. A break would strengthen bullish conditions. WTI futures support at $64.49, Jul 20 low was cleared last week. This strengthens the bearish theme and opens $60.81, 1.236 projection of the Jul 6 - 20 - 30 swing. Resistance is seen at $65.00, Aug 9 low.

- In FI, Bunds are lower this morning. The support to watch is unchanged at 176.21, the Aug 11 low. Trend conditions remain bullish. The bull trigger is 177.61, Aug 05 high. The Gilt futures outlook is bullish too and attention is on 130.72, Aug 4 high and the bull trigger. Support to watch is at 129.16, the 50-day EMA.

EQUITIES: Europe Gains Ground On Energy And Consumer Discretionary Stocks

- European equities are gaining, led by energy (Stoxx600 energy sector +1.8%) amid the oil price rally, and consumer discretionary (+1.4%), with the German Dax up 38.12 pts or +0.24% at 15808.04, FTSE 100 up 32.81 pts or +0.46% at 7087.9, CAC 40 up 59.79 pts or +0.9% at 6626.11 and Euro Stoxx 50 up 24.85 pts or +0.6% at 4147.5.

- U.S. futures are gaining, though the Nasdaq has underperformed a little in the European morning, with the Dow Jones mini up 153 pts or +0.44% at 35211, S&P 500 mini up 14.5 pts or +0.33% at 4451.5, NASDAQ mini up 38.5 pts or +0.26% at 15125.25.

- Overnight, Asian stocks closed higher, following Wall Street's lead Friday: Japan's NIKKEI up 480.99 pts or +1.78% at 27494.24 and the TOPIX up 34.46 pts or +1.83% at 1915.14. China's SHANGHAI closed up 49.798 pts or +1.45% at 3477.132 and the HANG SENG ended 259.87 pts higher or +1.05% at 25109.59

COMMODITIES: Oil Leads Gains

Crude oil is at the top of the commodities performance list, up over 3% at one point as the front WTI contract bounces from 4-month lows set Friday. More broadly, commodities are gaining across the board on a combination of improved risk appetite and a weaker UDS.

- WTI Crude up $1.84 or +2.96% at $63.99

- Natural Gas up $0.05 or +1.4% at $3.911

- Gold spot up $8.12 or +0.46% at $1786.11

- Copper up $7.85 or +1.9% at $419.95

- Silver up $0.37 or +1.62% at $23.3807

- Platinum up $23.51 or +2.36% at $1020.36

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.