MNI (LONDON) - Highlights:

- Harris narrows in on nomination, but betting odds still favour Trump

- JPY strength persists, AUD/JPY extends losses

- Chinese markets slip with commodities as outlook for policy support sours

US TSYS: Support From Softer Industrial Prices, 2Y Supply And Existing Home Sales Ahead

- Treasuries have seen some support overnight from a softer global growth outlook with industrial commodity prices including iron ore and copper falling further after what’s perceived by some as a lack of major new stimulus from the China Communist Party’s Third Plenum (for example, here).

- Moves are relatively limited though and leave benchmark tenors across the curve firmly within yesterday’s range after a flow-driven sell-off on a lighter session for headlines.

- Cash yields are 1.5-2.5bp lower with the front end lagging, but with curves also within ranges including 2s10s at -27.3bps (-0.3bps).

- TYU4 at 110-28+ (+ 05+) is close to session highs on somewhat subdued cumulative volumes of 260k.

- Yesterday’s low of 110-18+ cleared support at 110-21+ (20-day EMA) to open 110-07+ (50-day EMA). The latest pullback tests a bullish backdrop which includes resistance at 111-13+ (Jul 16 high).

- Today sees data focus on existing home sales before 2Y supply is possibly of more note. Last month’s 2Y auction came in almost in-line but with the bid-to-cover of 2.75x the highest since Aug 2023. A heavy docket for earnings is also in focus, with some large names including Alphabet, Tesla and Visa.

- Data: Philly Fed non-mfg Jul (0830ET), Existing home sales Jun (1000ET), Richmond Fed mfg Jul (1000ET)

- Note/bond issuance: US Tsy $69B 2Y Note auction -91282CLB5 (1300ET)

- Bill issuance: US Tsy $70B 42D CMB Auction (1130ET)

STIR: Fed Rates Hold Yesterday’s Climb, Awaiting Stronger Trigger Late In The Week

- Fed Funds implied rates hold yesterday’s second half climb that came about with little new drivers, showing little impact from further declines in industrial commodity prices overnight.

- It leaves implied rates close to highs seen since surprisingly soft US CPI on Jul 11, although still fully prices three cuts with the January meeting.

- Cumulative cuts from 5.33% effective: 0.5bp Jul, 24.5bp Sep, 39bp Nov, 61bp Dec and 78bp Jan.

- A reminder that the FOMC is in media blackout for the Jul 31 decision whilst today sees a pick-up in data with existing home sales and some regional Fed manufacturing surveys but with greater data focus on GDP and PCE data on Thu/Fri.

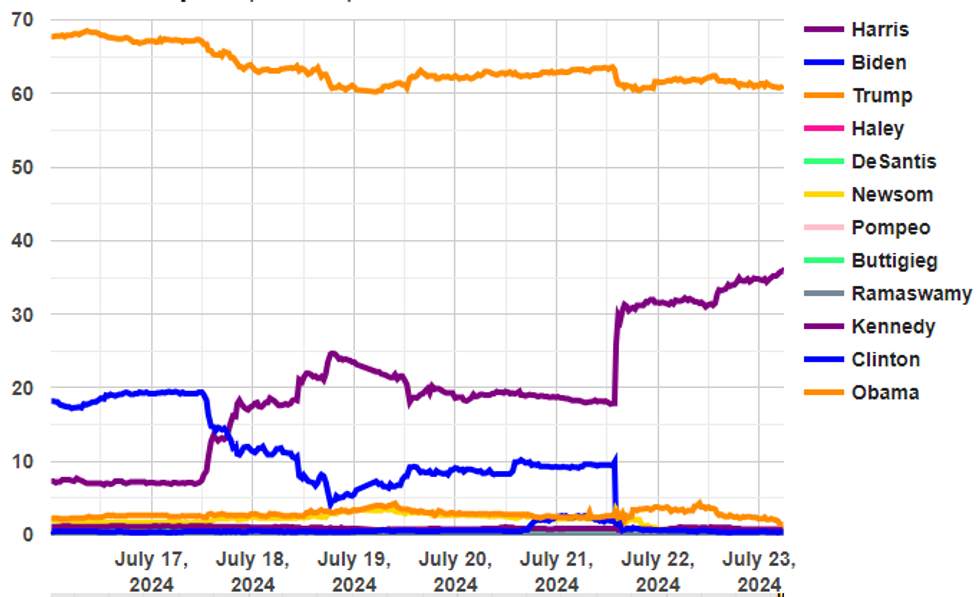

US: Harris Effectively Securing Dem Nom Does Little To Shift Betting Markets

An AP report claiming that Vice President Kamala Harris has won over enough Democratic National Convention delegates to effectively secure the party's presidential nomination, combined with news that the Harris For President campaign has seen a major influx of donations in the past 24hrs, has done little to move political betting markets regarding the outcome of November's election.

- AP has said it is not yet calling Harris the 'presumptive nominee' as delegates are free to vote for the candidate of their choosing at the 19-22 Aug DNC. However, AP reports that according to its unofficial survey Harris has gained the support of 2,668 delegates - well over the 1,976 majority threshold.

- The Harris For President campaign's securing ofUSD81mn in new funding from 880,000 donors over the past 24 hours is the largest in a day in presidential election history. Such

- In spite of these seemingly positive headlines for the Democrats, there has only been a small shift towards Harris in betting market implied probabilities for the election outcome.

- Data from electionbettingodds.com (which compiles Betfair, PredictIt, Polymarket, and Smarkets data) gives Harris a 35.8% implied probability of winning, up from 31.3% on 21 July in the immediate aftermath of President Joe Biden's withdrawal from the race.

- Former President Donald Trump is the favourite to win the White House, with a 61.1% implied probability. This is down from 63.3% immediately before Biden's withdrawal and a recent peak of 68.5% on 16 July.

- There will be significant focus on the first opinion polls with fieldwork done after Biden's withdrawal and as Harris looks set to become the Democratic nominee.

Chart 1. Betting Market Implied Probability of Presidential Election Winner (by Candidate), %

Source: electionbettingodds.com

Source: electionbettingodds.com

EUROPE ISSUANCE UPDATE:

UK auction results

A mixed linker auction, with a decent bid-to-cover in excess of 3x (albeit the lowest on a non-linker auction since September).

The price of 87.425 but below the secondary market low of the day at 87.448.

In spite of this, the 0.125% Mar-39 linker price is now higher than it was immediately on the release of the auction results (albeit it did have a very marginal dip at the time).

No wider impact on non-linker pricing.

GBP1bln of the 0.125% Mar-39 linker. Avg yield 1.053% (bid-to-cover 3.08x).

German auction results

E5bln (E4.096bln allotted) of the 2.70% Sep-26 Schatz. Avg yield 2.73% (bid-to-offer 1.61x; bid-to-cover 1.97x).

CHINA: Risk-off Moves Across China Work Against Local Markets

A particular focus on Chinese markets overnight, where risk-off moves worked against both headline equity indices as well as relevant industrial commodities:

- CHINA (BBG): Chinese Stocks Slump Amid Signs National Team Is Pulling Back

Chinese stocks suffered their biggest decline in six months as a lack of major policy support following the Third Plenum reinforced bearish sentiment. The onshore benchmark CSI 300 Index closed 2.1% lower, following a 0.7% drop in the previous session. - CHINA (Yicai): PBOC Could Phase Out MLF

The PBOC could eventually phase out its medium term lending facility and use the DR series of overnight rates as the main policy tool, according to Wen Bin, chief economist at China Minsheng Bank. - CHINA (BBG): China’s Deadly Rains to Intensify as Tropical Storms Arrive

Heavy rains lashing China have left at least 26 people dead in the past week, flooding city streets and threatening farming and industrial activity, as two more tropical storms barrel toward the nation. - COMMODITIES (BBG): Iron Ore Buckles Below $100 as China’s Plenum Fails to Inspire

Iron ore crumbled below $100 a ton as a policy meeting in China failed to deliver major stimulus, while supplies stayed strong. The outcome of the Third Plenum, a twice-a-decade conclave of Communist Party officials held last week, underwhelmed investors, with few steps to boost metals demand or fix the property crisis. - COMMODITIES (BBG): Copper Falls to Lowest Since Early April on China Pessimism

Copper fell to lowest level in almost four months on concern that Chinese demand for industrial metals is weakening. A twice-a-decade conclave of China’s top leadership held last week has so far failed to deliver any meaningful stimulus.

FOREX: Soft Iron Ore Undermines AUD/JPY as Sell-Off Accelerates

- The USD Index is rangebound, with early strength through the European open wholly reversed to keep most major pairs flat headed into the NY crossover. JPY remains the currency in focus, and a poor showing from Chinese equities in Tuesday trade helped JPY print a new recovery high, pressuring USD/JPY back below Y156.00.

- AUD/JPY remains the cross in focus on the break of the uptrendline last week, and now the close below the 50-dma. Clustered support at the Y102.65 100-dma and the early June low at 102.61 will be closely watched - particularly on any extension of the weakness in iron ore prices after Dalian-listed contracts fell close to 1.7% in Asia-Pac.

- NOK remains weaker after a poor start to the week. USD/NOK is narrowing the gap with 11.1385, the early May high. It's EUR/NOK that could trigger a further break here, as the cross tests 12.0062 - the cycle high posted in November last year.

- Richmond Fed and existing home sales data are top of the schedule for the US today, but markets are likely to be more sensitive to the prelim PMI print tomorrow. There are no central bank speakers of note, with both the BoE and Federal Reserve inside their pre-meeting media blackout periods.

FX OPTIONS: Sizeable Strikes, Quiet Calendar Keeping Spot G10 Contained

- EUR/USD's fade through early European hours puts spot within close proximity of the most sizeable strike rolling off in the pair today: E1.0bln at 1.0875-85, while USD/JPY is also narrowing in on $787mln at Y155.85.

- Lastly, AUD/NZD trade is of note - the contained price action so far Tuesday keeps the cross within range of N$1.1075, at which A$660mln is set to expire today.

- The pipeline is busier for the rest of the week, with the highlights including:

EUR/USD: Jul24 $1.0990(E3.2bln), $1.1000(E1.0bln)

USD/JPY: Jul24 Y156.00-05($2.3bln); Jul25 Y158.00($1.5bln)

AUD/USD: Jul24 $0.6600(A$1.6bln)

USD/CNY: Jul24 Cny7.3000($1.2bln)

EQUITIES: E-Mini S&P Continues to Trade Above Last Week's Lows

- A bull cycle in Eurostoxx 50 futures remains intact, despite the pullback in prices into the Friday close. The move lower last week undermines the bullish theme somewhat, with price having traded through the 50-day EMA, and the bear trigger has been tested at 4860.00, the Jun 14 low. Clearance of this level would expose 4846.00, the Apr 19 low and a key reversal point. For bulls, a move higher and a break of 5087.00, the Jul 12 high, would again highlight a bullish theme.

- The broader trend condition in S&P E-Minis is bullish and the slip lower into last week’s close appears to be a correction. The recent rally to cycle highs confirms a resumption of the uptrend and maintains the bullish sequence of higher highs and higher lows. MA studies are in a clear bull-mode set-up too, highlighting positive market sentiment. Sights are on 5741.34, a Fibonacci projection. Firm support is at 5486.11 the 50-day EMA.

COMMODITIES: WTI Futures Remain Below 50-Day EMA, Potential for Further Weakness

- Weakness into the Friday close keeps the focus pointed lower for WTI futures. The 50-day EMA gave way during the sell-off late last week, opening the potential for further losses toward 76.95 - the Jun 13th low on the continuation contract. Initial key resistance to watch is $83.58, the Jul 5 high, and a break and close above this level is needed ahead of any test on the 84.36 bull trigger.

- Gold prices faded across the second half of last week, resulting in new pullback lows of $2383.99 on Monday. Nonetheless, the broader gains last week reinforce current conditions, and keep the M/T trend pointed higher. The yellow metal has breached key resistance and the bull trigger at $2450.1, the May 20 high. This confirms a resumption of the medium-term uptrend and opens the $2500.00 handle next. Moving average studies are in a clear bull-mode set-up, highlighting a rising trend. Initial support is at $2390.6, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 23/07/2024 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 23/07/2024 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 23/07/2024 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 23/07/2024 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 23/07/2024 | 1400/1000 | *** | NAR existing home sales | |

| 23/07/2024 | 1400/1000 | ** | Richmond Fed Survey | |

| 23/07/2024 | 1530/1130 | * | US Treasury Auction Result for Cash Management Bill | |

| 23/07/2024 | 1700/1300 | * | US Treasury Auction Result for 2 Year Note | |

| 24/07/2024 | 2300/0900 | *** | Judo Bank Flash Australia PMI | |

| 24/07/2024 | 2301/0001 | * | Brightmine pay deals for whole economy | |

| 24/07/2024 | 0030/0930 | ** | Jibun Bank Flash Japan PMI | |

| 24/07/2024 | 0600/0800 | * | GFK Consumer Climate | |

| 24/07/2024 | 0645/0845 | ECB's de Guindos at ECB/IMF conference | ||

| 24/07/2024 | 0700/0900 | ** | PPI | |

| 24/07/2024 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 24/07/2024 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 24/07/2024 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 24/07/2024 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 24/07/2024 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 24/07/2024 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 24/07/2024 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 24/07/2024 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 24/07/2024 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 24/07/2024 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 24/07/2024 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 24/07/2024 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 24/07/2024 | 1200/1400 | ECB's Lane at ECB/IMF conference | ||

| 24/07/2024 | 1345/0945 | BOC Monetary Policy Report | ||

| 24/07/2024 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 24/07/2024 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 24/07/2024 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 24/07/2024 | 1400/1000 | *** | New Home Sales | |

| 24/07/2024 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 24/07/2024 | 1430/1030 | BOC Governor Press Conference | ||

| 24/07/2024 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 24/07/2024 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note |