Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Data deluge ahead of the long weekend

- China FX strengthens further, new multi-year highs vs. USD

- WTI nears new post-pandemic highs

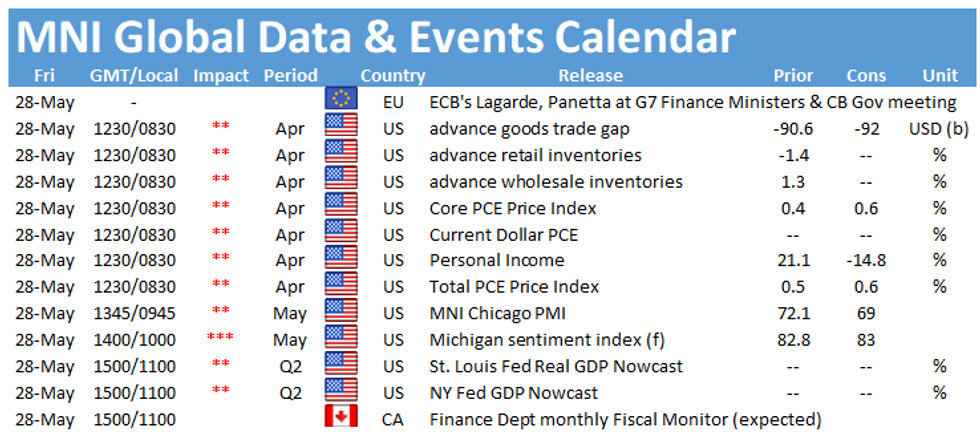

US TSYS SUMMARY: Data Provides Pre-Holiday Weekend Focus

Treasuries are pretty flat having bounced from overnight lows (again, in pretty modest ranges in Asia-Pac and European trade). Data is set to be the main focus of the shortened pre-holiday weekend session.

- The 2-Yr yield is unchanged at 0.1446%, 5-Yr is up 0.3bps at 0.8187%, 10-Yr is up 0.3bps at 1.6096%, and 30-Yr is up 0.8bps at 2.2903%.

- Sep 10-Yr futures (TY) down 2/32 at 131-23, briefly touching worst levels since Monday (L: 131-20 / H: 131-25).

- Equities are on the front foot, with S&P eminis at the highest since May 10. Dollar's a little stronger too.

- Another 0830ET data dump: personal income / spending are the focus, including PCE deflator; we also get advance goods trade balance and wholesale/retail inventories.

- Then at 0945ET, May MNI Chicago PMI, followed by final UMIch Sentiment at 1000ET.

- No scheduled Fed speakers, and no supply. NY Fed buys ~$12.425B of 0-2.25Y Tsys.

- Reminder of early closure today ahead of the holiday weekend.

EGB/GILT SUMMARY - Mixed So Far

Following a weak start, European government bonds now trade mixed on the day. Equity performance has similarly been uneven, while the dollar has been on the front foot against G10 FX.

- Gilts have traded weaker with cash yields 1-2bp higher and the very long of the curve slightly steeper.

- Germany bonds similarly had a weak start but soon recovered losses to trade flat on the day.

- OATs have also recovered following the earlier sell off, with the belly of the curve now trading marginally above yesterday's close.

- The BTP curve has bull steepened with the 2s30s spread 2bp wider.

- The final estimate of French Q1 GDP was revised lower (-0.1% Q/Q vs an initial estimate of 0.4$),

- Supply this morning came from the UK (Treasury Bills, GBP3bn) and Italy (BTPs/CCTeu, EUR8.5bn)

EUROPE ISSUANCE SUMMARY

Italy sells:

- E3.000bln 0% Apr-26 BTP, Avg yield 0.170% (Prev. 0.170%), Bid-to-cover 1.36x (Prev. 1.43x)

- E3.500bln 0.60% Aug-31 BTP, Avg yield 0.940% (Prev. 0.880%), Bid-to-cover 1.32x (Prev. 1.44x)

- E2.000bln 0.50% Apr-26 CCTeu , Avg yield -0.070% (Prev. -0.060%), Bid-to-cover 1.51x (Prev. 1.92x)

OPTION FLOW SUMMARY

Eurozone:

RXN1/RXU1 170/169.5/169/168.5p condor spread, sold July and receive half a tick in 2k

3RU1/3RN1 100.25 call calendar, bought for 2.5 in 3k

UK:

0LZ1 99.625/99.375/99.125p fly vs 99.875c, bought the fly for 3 in 15k

0LZ1 99.25/99.00ps, bought for 1.5 in 1k

Equities:

SX7E Aug 92.5p bought for 2.85 in 40.5k and 2.75 in 4.5k (45k total)

Recall this was bought for 3.05 in 40k yesterday and also traded 3.35 in 32k and 3.40 in 8k (40k total) on Wednesday

FOREX: Month-End Flow a Focus

- The greenback is moderately higher Friday morning, helping bump the USD Index back above the 90.00 handle. Similarly, the EUR trades more favourably, with month-end flow a focus into the early US close. Despite the final May fix falling on Monday, the US and UK market holidays may prompt participants to bring forward month-end flow into today's close. Most sell-side models point to a weak requirement to buy USD.

- Antipodean FX trades weaker, with AUD and NZD the poorest performers so far Friday. AUD/USD sits just above 50-dma support at 0.7714 while NZD/USD is edging off the multi-month highs posted this week at 0.7316.

- China FX remains a focal point, with CNH & CNY again stronger and hitting the highest level against the USD since 2018.

- Today's MNI Chicago PMI will be a highlight, with markets expecting the pace of expansion to slow to 68.0 from 72.1. April PCE data also crosses alongside the latest personal income/spending update. There are no central bank speakers of note.

FX OPTIONS: Expiries for May28 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1985-1.2000(E1.0bln), $1.2100-15(E552mln), $1.2185-1.2200(E1.8bln-EUR puts), $1.2210-20(E1.2bln-EUR puts), $1.2250-65(E1.2bln-EUR puts), $1.2275(E722mln-EUR puts), $1.2300(E672mln-EUR puts)

- USD/JPY: Y108.50-60($895mln-USD puts), Y110.00($2.0bln-USD puts), Y110.50($976mln)

- GBP/USD: $1.4200(Gbp817mln-GBP puts)

- EUR/JPY: Y132.80-00(E723mln)

- EUR/CHF: Chf1.1000(E960mln-EUR puts)

- AUD/USD: $0.7750(A$553mln)

- USD/CAD: C$1.2000($640mln-USD puts), C$1.2050($C420mln), $1.2100($1.3bln), C$1.2150($612mln-USD puts)

- USD/MXN: Mxn19.75($1.3bln-USD puts), Mxn20.25($689mln)

Price Signal Summary - EUROSTOXX 50 Is Through Resistance

- In the equity space, S&P E-minis are firmer and approaching the key resistance at 4238.25 May 10. Key trend support is unchanged at 4029.25, May 13 low. The 20-day EMA marks initial support at 4158.91. EUROSTOXX 50 futures trend conditions remain bullish with the focus on 4099.00,1.00 projection of the Mar - Jul - Oct 2020 price swing.

- In the FX space, EURUSD continues to trade within its recent range. The pair this week cleared 1.2245 and sights set on 1.2285 next, Jan 8 high. Watch support at 1.2160, May 19 low. GBPUSD traded higher yesterday and remains bullish. The focus is on 1.4237, Feb 24 high and this year's high print. A break would confirm a resumption of the broader uptrend. USDJPY has resumed its uptrend breaking above 109.79, May 13 high and the bull trigger. This opens 110.15 next, 76.4% retracement of the Mar 31 - Apr 23 sell-off.

- On the commodity front, Gold remains bullish. The yellow metal has topped $1,900 this week and this opens the Jan 8 high of $1917.6. Trend conditions remain overbought, however this is not impacting the trend. $1872.8, May 25 low is first support. Oil contracts are trading near recent highs. Brent (N1) key resistance is at $70.24, May 18 high and this marks the bull trigger. WTI (N1) has confirmed a fresh trend high print of $67.45 today. This marks a resumption of the underlying uptrend. The focus is on $67.95, Oct 29 2018 high (cont)

- Within FI, Bunds (M1) has stalled ahead of the 50-day EMA at 1470.48. This signals the end of the recent correction. A clear breach of the average is required to signal scope for further gains. Gilts (U1) faced selling pressure yesterday. A firm resistance exists at 127.74/82, high between Apr 20 and May 26.

EQUITIES: Continental Markets Solid, VG1 Tops Resistance

- Continental stock markets are higher early Friday, with the core EuroStoxx 50 higher by 0.5% while the UK's FTSE-100 lags slightly with gains of 0.2%. In futures, EUROSTOXX 50 trend conditions remain bullish with the focus on 4099.00,1.00 projection of the Mar - Jul - Oct 2020 price swing.

- Europe's financials sector extends recent outperformance, and is top of the pile again Friday. Technology and industrials names also trade well, while the energy sector is the sole decliner so far.

- UK homebuilders are among the best performers in the Stoxx 600, with Taylor Wimpey and Barratt Developments among the largest climbers this morning.

COMMODITIES: Oil Sustains Bounce, Gold & Silver Lag

- Both Brent and WTI crude futures are sustaining the modest bounce posted since late Thursday, with WTI nearing next resistance at $67.50. A break north of here opens the Oct 29, 2018 high at $67.95 and the next key upside level at $68.39.

- Gold and silver are lagging under the weight of a firmer greenback, with the USD Index's bounce back above 90.00 keeping spot gold south of the $1900/oz mark. First support undercuts at the May 25 / May 19 low at $1872.8/52.3.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.