Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

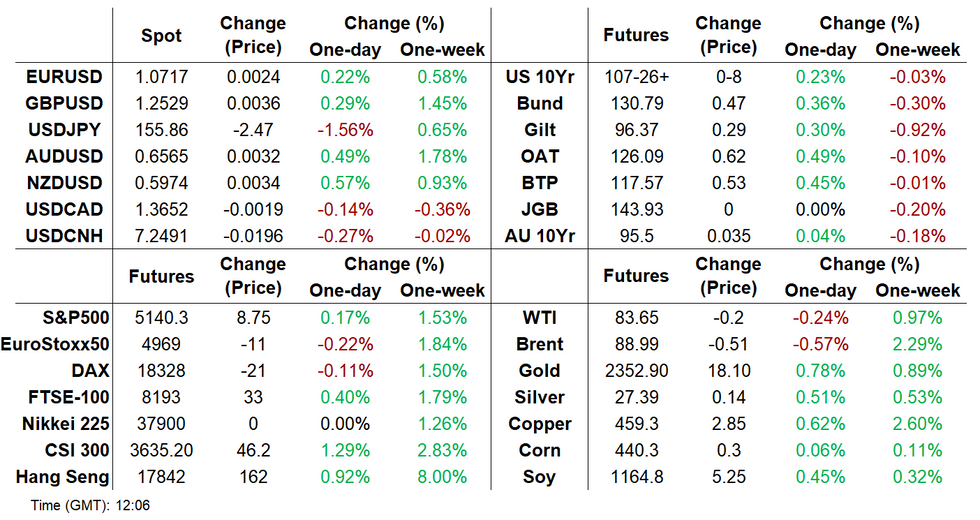

- JPY intervention speculation dominates, with USD/JPY range topping 500 pips.

- Iniital rounds of CPI data helps EGBs to outperform.

- ECB-speak and the U.S. quarterly refinancing estimates headline from here.

US TSYS: Underperforming EGBs, Treasury Refinancing Estimates Headline

- Treasuries underperform the rally seen in EGBs after softer than expected Spanish CPI before German regional inflation also indicated a national print on the softer side.

- Cash yields sit 2.5-4.5bp lower after the late open with Japan out, bull flattening with 2s10s at -34.9bps (-2.2bps) at levels more sustainably seen on Apr 23.

- TYM4 has touched a high of 107-28 (+ 09+) in a move closer to resistance at 108-15+ (20-day EMA), under slightly below average cumulative volumes of 260k.

- However, gains are considered corrective with support seen at 107-04 (Apr 25 low).

- Today’s focus is firmly on Treasury’s quarterly financing estimates at 1500ET – we’ll write more on what to expect a little nearer the time.

- Data: Dallas Fed mfg Apr (1030ET) – the last of the regional Fed mfg surveys for April.

- Bill issuance: 1130 US Tsy $70B 13W, $70B 26W Bill auctions (1130ET)

US TSY FUTURES: Notable Short Cover Seen Across Most Of Curve On Friday

Friday’s rally in Tsy futures and preliminary OI data point to aggressive net short cover across most of the curve, with the only exception coming via apparent modest net long setting in UXY futures.

- The apparent short cover in TY futures provided the most notable positioning swing.

- A reminder that we wrote the following during the rally “a quick reflection covering recent positioning when it comes to the post-Friday data rally in Tsys. More than $15mn DV01 equivalent of fresh net shorts was set across the Tsy futures curve over Wednesday and Thursday (as flagged in our daily OI updates). While some of that can likely be explained away by basis trade activity, today’s move may partly reflect a squeeze of some of the weaker short positions.”

- This looks to have played out, with over $11.5mn of net DV01 equivalent short covering seen.

- The move came as markets reacted to March’s PCE data, with revisions to the data set pointing to January as the key driver for the upward surprise in the core Q1 PCE reading the day prior, presenting a less hawkish outcome for markets.

| 26-Apr-24 | 25-Apr-24 | Daily OI Change | OI DV01 Equivalent Change ($) | |

| TU | 4,083,808 | 4,111,208 | -27,400 | -988,099 |

| FV | 6,006,160 | 6,054,061 | -47,901 | -1,961,776 |

| TY | 4,438,706 | 4,540,620 | -101,914 | -6,402,225 |

| UXY | 2,057,528 | 2,052,820 | +4,708 | +399,813 |

| US | 1,563,154 | 1,577,277 | -14,123 | -1,765,932 |

| WN | 1,630,700 | 1,635,485 | -4,785 | -915,434 |

| Total | -191,415 | -11,633,653 |

STIR: Fed Rate Path Dips Away From Post PCE Highs

- Fed Funds implied rates have drifted lower overnight, aided by softer than expected Spanish and German CPI inflation.

- The rate path still remains within Friday’s monthly PCE-inspired range though and holds the majority of the jump higher seen after Thursday’s Q1 GDP/PCE data.

- Cumulative cuts from 5.33% effective: 1bp May, 3bp Jun, 9bp Jul, 20bp Sep, 25.5bp Nov and 36bp Dec (vs 34bp Dec Fri close).

STIR: OI Points To Mix Of SOFR Long Setting & Short Cover Following Monthly PCE

The combination of open interest data and Friday's modest uptick across most SOFR futures points to a mix of net long setting and short cover, with the former more prominent in the reds and greens and latter more prominent in the whites and blues.

- The move came as markets reacted to March’s PCE data, with revisions to the data set pointing to January as the key driver for the upward surprise in the core Q1 PCE reading the day prior, presenting a less hawkish outcome for markets.

- This allowed the market implied path of Fed policy rates to edge away from the shallowest cutting path of the current market cycle as the data was digested.

| 26-Apr-24 | 25-Apr-24 | Daily OI Change | Daily OI Change In Packs | ||

| SFRH4 | 926,962 | 932,136 | -5,174 | Whites | -19,207 |

| SFRM4 | 1,121,561 | 1,136,315 | -14,754 | Reds | +15,035 |

| SFRU4 | 997,028 | 996,347 | +681 | Greens | +14,178 |

| SFRZ4 | 1,187,674 | 1,187,634 | +40 | Blues | -2,229 |

| SFRH5 | 735,594 | 732,945 | +2,649 | ||

| SFRM5 | 821,794 | 816,397 | +5,397 | ||

| SFRU5 | 710,885 | 713,567 | -2,682 | ||

| SFRZ5 | 799,922 | 790,251 | +9,671 | ||

| SFRH6 | 484,857 | 483,356 | +1,501 | ||

| SFRM6 | 514,855 | 503,294 | +11,561 | ||

| SFRU6 | 384,682 | 381,222 | +3,460 | ||

| SFRZ6 | 351,090 | 353,434 | -2,344 | ||

| SFRH7 | 228,693 | 230,369 | -1,676 | ||

| SFRM7 | 184,399 | 184,251 | +148 | ||

| SFRU7 | 167,486 | 168,180 | -694 | ||

| SFRZ7 | 142,725 | 142,732 | -7 |

BONDS: European CPIs Result In EGB Rally, OATs Tighten On Rating Relief

EGBs rallied on the back of the Spanish CPI data, with the move then extending as German regional CPI readings pointed to downside risk in this afternoon’s national flash reading (click for further details on the German data)

- Bund futures extended through Friday’s peak but haven't tested 131.00, last 130.80. The speed of this morning’s move may have acted as a limiting factor earlier in the day, in addition to the presence of this morning's EU supply.

- German cash yields are 3-5bp lower across the curve, light flattening seen.

- OATs have benefitted from ratings relief after France avoided negative action from both Fitch (current rating: AA-; Outlook Stable) & Moody’s (current rating: Aa2; Outlook Stable) after hours on Friday. OATs outperform EGBs and core global peers across the curve as a result. Click for further colour.

- Spanish PM Sanchez has decided to stay on after tabling a potential resignation on the back of a corruption scandal surrounding his wife. SPGBs are little changed on the news, with little widening pressure seen ahead of time. Click to see why.

- Gilts follow broader price moves in EGBs, albeit lagging German peers across the curve. Futures have moved through Friday's highs, last 96.36, while cash gilt yields are 3-4bp lower across the curve.

- ECB-speak from Lane, Muller & de Guindos is due during the remainder of the day.

EUROPEAN ISSUANCE UPDATE

BTP/CCTeu auction results

- E3.25bln of the 3.35% Jul-29 BTP. Avg yield 3.41% (bid-to-cover 1.33x).

- E3.5bln of the 3.85% Jul-34 BTP. Avg yield 3.86% (bid-to-cover 1.34x).

- E3.5bln of the 1.05% Apr-32 CCTeu. Avg yield 4.9% (bid-to-cover 1.39x).

EU-bond / Green EU-bond auction results

- Another relatively weak EU-bond auction with the lowest accepted price only just above the pre-auction mids and relatively weak bid-to-covers.

- E2.377bln of the 3.125% Dec-28 EU-bond. Avg yield 2.935% (bid-to-cover 1.15x).

- E2.293bln of the 2.75% Feb-33 Green EU-bond. Avg yield 2.952% (bid-to-cover 1.20x).

FOREX: USDJPY Substantially Lower Amid Strong Indications of MOF Intervention

The Bank of Japan’s decision to downplay the yen’s impact on inflation last Friday prompted a further sharp weakening of the currency. This culminated in USDJPY breaching the 160.00 overnight, amid thin liquidity due to the Japanese holiday. This took the rally from Friday’s lows to over 500 pips to reach a high of 160.17, closely matching the April 1990 peak.

- However, the subsequent aggressive move lower has somewhat justified that market’s cautious rhetoric, with strong indications that the MOF may have intervened to stabilise the JPY. There has been no official confirmation on intervention from Japanese authorities, with top currency official Kanda stating he has ‘no comment for now’. Subsequent Dow Jones source reports pointed to intervention, but were light on details.

- The bulk of the move lower came ahead of the European open, with USDJPY moving from around 159.50 to 155.60. A second wave of selling came just after 0800BST, where the pair traded down to a low of 154.54, just shy of initial key support at 154.01, the 20-day EMA.

- As a result, the USD index resides 0.28% lower, in fitting with modestly lower US yields. Stock markets trade marginally in the green, which assists the likes AUD (+0.47%) and NZD (+0.57%) which outperform in G10. Initial readings of Eurozone inflation have had little impact on EURUSD which hovers just above 1.07.

- With Aussie retail sales and China PMIs overnight, attention will be on a developing bullish phase for AUDUSD. Resistance at 0.6526, the 50-day EMA, has been breached and the clear break highlights a stronger reversal that signals scope for a climb towards 0.6644, the Apr 9 high.

- Key attention this week will rest on Wednesday’s Fed meeting and press conference, as well as Friday’s release of NFP.

FOREX OPTIONS: Expiries for Apr29 NY cut 1000ET (Source DTCC)

- EURUSD: 1.0695 (348mln), 1.0700 (223mln), 1.0710 (686mln), 1.0720 (499mln), 1.0725 (387mln), 1.0750 (1.38bn), 100775 (449mln), 1.0800 (261mln).

- GBPUSD: 1.2600 (490mln).

- USDCAD: 1.3700 (540mln).

- AUDNZD: 1.0900 (1.09bn), 1.1100 (866mln).

- USDCNY: 7.2500 (780mln).

EQUITIES: EUROSTOXX 50 Futures Bull Cycle Remains In Play

The short-term trend condition in S&P E-Minis remains bearish and the latest recovery appears to be a correction. The contract has recently cleared the 50-day EMA, signalling scope for a continuation lower. A resumption of the bear leg would open 4907.57, 50.0% of the Oct 27 ‘23 - Apr 1 bull leg. Firm resistance at 5138.19, the 20-day EMA, has been pierced, a clear break would instead signal a reversal and expose key resistance at 5333.50, the Apr 1 high.

- EUROSTOXX 50 futures are holding on to their recent gains from 4762.00, the Apr 19 low. The contract has breached the 20-day EMA and resistance at 4990.00, Apr 15 high. This highlights a potentially stronger reversal. A continuation higher would expose the bull trigger at 5079.00, the Apr 2 high. Key support lies at 4762.00. Initial support to watch is 4874.10, the 50-day EMA.

COMMODITIES: Bear Threat In Gold Remains Present

Gold remains in consolidation mode and is trading closer to its recent lows. The precious metal last week pierced the 20-day EMA and this highlights the start of a possible corrective cycle. A continuation lower would signal scope for an extension towards $2233.6, the 50-day EMA. Note that a short-term bear cycle would allow a significant overbought condition to unwind. Key resistance and the bull trigger is at $2431.5, the recent Apr 12 high.

- In the oil space, WTI futures continue to trade above key short-term support at $81.14, the 50-day EMA. The recent move down between Apr 12 - 22, highlights a corrective phase and a clear break of the 50-day average would signal scope for a deeper retracement towards $76.07, the Mar 11 low. On the upside, key resistance and the bull trigger has been defined at $86.97, the Apr 12 high.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 29/04/2024 | 1200/1400 | *** |  | DE | HICP (p) |

| 29/04/2024 | 1430/1030 | ** |  | US | Dallas Fed manufacturing survey |

| 29/04/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 29/04/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 29/04/2024 | 1920/2120 |  | EU | ECB's De Guindos remarks at Euro50Group Dinner | |

| 30/04/2024 | 2301/0001 | * |  | UK | BRC Monthly Shop Price Index |

| 30/04/2024 | 2330/0830 | * |  | JP | Labor Force Survey |

| 30/04/2024 | 2330/0830 | ** | | JP | Industrial Production |

| 30/04/2024 | 2330/0830 | * | | JP | Retail Sales (p) |

| 30/04/2024 | 0130/0930 | *** |  | CN | CFLP Manufacturing PMI |

| 30/04/2024 | 0130/0930 | ** | | CN | CFLP Non-Manufacturing PMI |

| 30/04/2024 | 0130/1130 | ** |  | AU | Retail Trade |

| 30/04/2024 | 0145/0945 | ** | | CN | IHS Markit Final China Manufacturing PMI |

| 30/04/2024 | 0530/0730 | *** |  | FR | GDP (p) |

| 30/04/2024 | 0530/0730 | ** | | FR | Consumer Spending |

| 30/04/2024 | 0600/0800 | ** | | DE | Retail Sales |

| 30/04/2024 | 0600/0800 | ** | | DE | Import/Export Prices |

| 30/04/2024 | 0645/0845 | *** | | FR | HICP (p) |

| 30/04/2024 | 0645/0845 | ** | | FR | PPI |

| 30/04/2024 | 0700/0900 | *** |  | ES | GDP (p) |

| 30/04/2024 | 0700/0900 | ** |  | CH | KOF Economic Barometer |

| 30/04/2024 | 0755/0955 | ** | | DE | Unemployment |

| 30/04/2024 | 0800/1000 | *** |  | IT | GDP (p) |

| 30/04/2024 | 0800/1000 | *** | | DE | GDP (p) |

| 30/04/2024 | 0830/0930 | ** | | UK | BOE M4 |

| 30/04/2024 | 0830/0930 | ** | | UK | BOE Lending to Individuals |

| 30/04/2024 | 0900/1100 | *** | | EU | HICP (p) |

| 30/04/2024 | 0900/1100 | *** | | EU | EMU Preliminary Flash GDP Q/Q |

| 30/04/2024 | 0900/1100 | *** | | EU | EMU Preliminary Flash GDP Y/Y |

| 30/04/2024 | 0900/1100 | *** | | IT | HICP (p) |

| 30/04/2024 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 30/04/2024 | 1100/1200 | | UK | Asset Purchase Facility Quarterly Report 2024 Q1 | |

| 30/04/2024 | 1230/0830 | *** | | US | Employment Cost Index |

| 30/04/2024 | 1230/0830 | *** |  | CA | Gross Domestic Product by Industry |

| 30/04/2024 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 30/04/2024 | 1300/0900 | ** | | US | S&P Case-Shiller Home Price Index |

| 30/04/2024 | 1300/0900 | ** | | US | FHFA Home Price Index |

| 30/04/2024 | 1300/0900 | ** | | US | FHFA Home Price Index |

| 30/04/2024 | 1345/0945 | *** | | US | MNI Chicago PMI |

| 30/04/2024 | 1400/1000 | *** | | US | Conference Board Consumer Confidence |

| 30/04/2024 | 1400/1000 | ** | | US | housing vacancies |

| 30/04/2024 | 1430/1030 | ** | | US | Dallas Fed Services Survey |

| 30/04/2024 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 01/05/2024 | 2245/1045 | *** |  | NZ | Quarterly Labor market data |

| 01/05/2024 | 2300/0900 | ** | | AU | IHS Markit Manufacturing PMI (f) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.