Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Long-end Treasuries selling off further post-Fed

- NOK outperforms as Norges Bank bring forward rate hike projections

- Bank of England decision takes focus

US TSYS SUMMARY: Long End Sell-Off Continues

Long-dated Tsy yields continued to shoot to fresh highs overnight, with the short-end / belly fading most post-FOMC gains as well.

- A trigger for the sell-off across the curve was a Nikkei report pointing to the potential for the Bank of Japan to widen the 10-Year JGB yield target band at tomorrow's BoJ decision (to -/+0.25% from -/+0.20% at present), although arguably the language in the article itself is a little less forceful than the headlines.

- Nevertheless, yields across the Tsy curve pushed up sharply, accelerating when European desks came in, led by 10s: 2-Yr yield is up 1.4bps at 0.1471%, 5-Yr is up 4.9bps at 0.8473%, 10-Yr is up 8bps at 1.7224%, and 30-Yr is up 6.8bps at 2.4862%.

- Jun 10-Yr futures (TY) down 24.5/32 at 131-10.5 (L: 131-05.5 / H: 132-03) on very heavy volumes, ~900+k traded so far.

- Equities have reversed course lower, and the USD higher.

- 0830ET brings the bulk of the day's data: jobless claims data and Philadelphia Fed biz outlook.

- We get $80B of 4-/8-week bill auctions at 1130ET, with $13B 10Y TIPS auction at 1300ET. NY Fed buys ~$1.750B of 20Y-30Y Tsys.

EGB/GILT SUMMARY: Further Vaccine Disruptions

European sovereign bonds have sold off and curves have bear steepened alongside gains for equities.

- Gilts are leading the correction with casy yields 2-7bp higher and the curve 5bp steeper. The Jun-21 gilt future is making fresh intraday day lows and last traded at 126.84.

- Following yesterday's initial headline that UK Covid vaccine supplies will be squeezed in the coming weeks, reports came out this morning that an increase in demand for the AstraZeneca vaccine in India have impacted planned exports of the jab to the UK.

- Yesterday's announcement from the European Commission President Ursula Von der Leyen on the possibility of emergency vaccine controls to prevent exports outside of the bloc, continues to weigh.

- Bunds have traded weaker with the long end of the curve underperforming. The 2s30s spread is 3bp wider.

- It is a similar story for OATs where cash yields are up to 3bp higher.

- Supply this morning came from France (OATs, EUR9.5bn), Spain (Bonos/Oblis, EUR6.171bn) and Ireland (Bills, EUr750mn).

EUROPE ISSUANCE: Spanish, French Auctions

France's AFT sells E9.5bln MT OATs vs E8.5-9.5bln target:

- E4.99bln 0% Feb-24 OAT, Avg yield -0.61%, Bid-to-cover 2.02x

- E3.10bln 0% Feb-26 OAT, Avg yield -0.48%, Bid-to-cover 2.09x

- E1.405bln 0.75% May-28 OAT, Avg yield -0.28%, Bid-to-cover 2.51x

France's AFT Sells E2.0bn In Linkers

- E1.028bln 0.10% Mar-26 OATei, Avg yield -1.700%, Bid-to-cover 2.42x

- E0.360bln 0.10% Mar-28 OATi, Avg yield -1.300%, Bid-to-cover 3.08x

- E0.609bln0.70% Jul-30 OATei Avg yield -1.410%, Bid-to-cover 2.79x

Spain sells E6.2bln Bonos/Oblis vs E5.5-6.5bln target

- E2.137bln 0% May-24 Bono Avg yield -0.396%, Bid-to-cover 1.83x

- E3.047bln 0% Jan-28 Bono Avg yield 0.000%, Bid-to-cover 1.70x

- E0.987bln 1.00% Oct-50 Obli Avg yield 1.297%, Bid-to-cover 1.55x

EUROPE OPTION FLOW

Eurozone:

RXK1 173c bought for 21, 22, 22.5 in ~24k - said to be part of a condor leg short cover

RXK1 170/171.5 RR, bought the put for 4 in 1.5k

DUK1 112.10^ sold at 10 in 1.25k (6k total between yesterday and today)

ERM1 100.37/100.62 combo, bought the put for 0.25 in 5k (ref 100.535)

0RU1 100.37p, sold at 2 in 3.5k total

FOREX: NOK Firms as Norges Bank Bring Forward First Hike

- The greenback remains lower relative to pre-Fed levels yesterday, which was read as dovish, but is clawing back some of the losses against the EUR , CNH and AUD. The move is mirroring the softer equity market this morning, with the e-mini S&P retreating off overnight highs of 3988.75.

- The NOK trades stronger following the release of their Q1 Monetary Policy Report. The Bank signalled that the first post-COVID rate hike would be brought forward by around a quarter to December 2021. Two further full rate hikes are now priced into 2022 and the terminal rate nudged higher toward 1.5%. This steepening of rate path projections underpinned NOK strength this morning, pressuring USD/NOK back toward the 2021 lows of 8.3151.

- SEK, EUR are among the worst performers so far Thursday, with AUD, CAD the strongest.

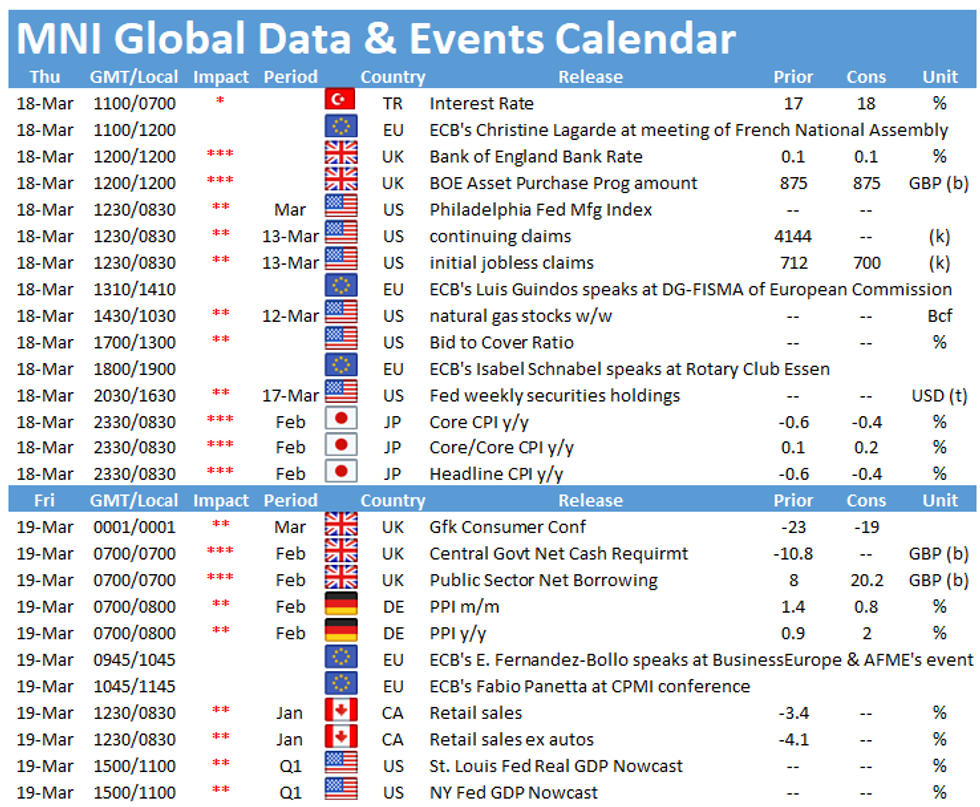

- Focus turns to rate decisions from the Bank of England and Turkish central bank later today. US weekly jobless claims are also due.

FX OPTIONS: Expiries for Mar18 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1900(E1.6bln-EUR puts), $1.1940-50(E798mln-EUR puts), $1.1995-1.2005(E1.7bln-EUR puts)

- USD/JPY: Y106.60($850mln), Y107.75($587mln), Y108.25-35($770mln)

- GBP/USD: $1.3611(Gbp602mln), $1.3900(Gbp410mln), $1.3950(Gbp620mln)

- EUR/GBP: Gbp0.8500(E720mln), Gbp0.8600(E1.7bln-EUR puts), Gbp0.8625(E1.15bln), Gbp0.8650(E581mln)

- EUR/CHF: Chf1.1200(E721mln)

- AUD/USD: $0.7700-15(A$1.6bln), $0.7750-55(A$2.2bln), $0.7850(A$1.3bln)

- AUD/NZD: N$1.0770-75(A$1.4bln-AUD puts)

- EUR/AUD: A$1.5500(E785mln)

- USD/CAD: C$1.2490-00($530mln), C$1.2685-90($1.6bln)

- USD/CNY: Cny6.3450($1.2bln), Cny6.43($1.1bln), Cny6.5650($582mln)

TECHS: Price Signal Summary - FI Bears Return

- In the equity space conditions are unchanged and E-mini S&P bulls remain in charge despite today's move away from the earlier high of 3978.50. The focus is on 4000. Support to watch is at 3886.03, the 20-day EMA.

- In the FX space:

- EURUSD resistance at 1.1990, Mar 11 high remains intact. This level represents the trigger for a stronger S/T recovery. Note, yesterday price action is a bullish engulfing candle and does highlight the potential for stronger gains. A break of 1.1990 would open 1.2067 Mar 4 high. Support is at 1.1883, Mar 16 low. A break would negate the pattern and expose key support at 1.1836, Mar 9 low.

- USDJPY remains in an uptrend. The focus is on 109.56, 61.8% of the Mar 2020 - Jan downleg and an important pivot resistance. Support is at 108.34 Mar 10 low.

- USDCAD extends the sell-off from Mar 5 with a fresh trend low earlier today. This confirms a resumption of the downtrend with attention on 1.2307, the lower band of a moving average envelope.

- On the commodity front, Gold is off the overnight highs. A bullish outlook remains intact though and scope is seen for a climb towards the 50-day EMA at $1786.7. Firm short-term support has been defined at $1699.3, Mar 12 low. Oil contracts remain below the Mar 8 high. The key directional triggers are unchanged at:

- Brent (K1) - $71.38, Mar 8 high and $66.50, Mar 10 low.

- WTI (J1) - $67.98, Mar 8 high and $63.13, Mar 10 low.

- In the FI space, Bunds (M1) are under pressure and have probed support at 170.72, Mar 5 low. With resistance at 172.20, Mar 11 high intact, further weakness is likely near-term. 170.37, 61.8% of the Feb 25 - Mar 11 rally marks the next objective. Gilts (M1) have registered a fresh trend low print confirming a resumption of the downtrend. The focus is on 126.85 May 3, 2019 low (cont). Treasuries are offered once again as the downtrend extends. The focus is on 131-00 next.

EQUITIES: Post-FOMC Gains Fade

- Asian stocks closed higher, with Japan's NIKKEI up 302.42 pts or +1.01% at 30216.75 and the TOPIX up 24.48 pts or +1.23% at 2008.51. China's SHANGHAI closed up 17.517 pts or +0.51% at 3463.068 and the HANG SENG ended 371.6 pts higher or +1.28% at 29405.72.

- European equities are mixed, with the German Dax up 108.76 pts or +0.75% at 14697.5, FTSE 100 down 21.51 pts or -0.32% at 6757.86, CAC 40 down 2.35 pts or -0.04% at 6060.17 and Euro Stoxx 50 up 11.74 pts or +0.31% at 3858.82.

- U.S. futures are lower, with the Dow Jones mini up 18 pts or +0.05% at 33035, S&P 500 mini down 18.75 pts or -0.47% at 3955.25, NASDAQ mini down 165.25 pts or -1.25% at 13036.25.

COMMODITIES: Oil Leads Lower

- WTI Crude down $0.68 or -1.05% at $63.97

- Natural Gas down $0.01 or -0.32% at $2.522

- Gold spot down $8.05 or -0.46% at $1736.26

- Copper down $2.25 or -0.55% at $410.55

- Silver down $0.07 or -0.25% at $26.2441

- Platinum down $3.01 or -0.25% at $1210.63

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.