Highlights:

- Treasuries firm modestly in placeholder trade ahead of CPI

- AUD position improves markedly in latest CFTC report

- UK DMO to release quarterly consultation agenda as soon as today

US TSYS: Edging Richer On Low Volumes With Mid-Week CPI Eyed

- Treasuries have biased firmer overnight and at a slightly faster pace as US desks filter in, although they remain easily within Friday’s range having sold off on the strong Canadian jobs report and then higher US U.Mich consumer inflation expectations.

- Cash yields sit 1.5-2.5bp lower, led by the front end for a mild bull steepening with 2s10s at -36.0bps. The decline slightly lags EGBs.

- TYM4 at 108-27 (+ 04+) has lifted above particularly narrow ranges seen in Asia hours but remains well within Friday’s range, on low cumulative volumes of just 210k.

- Friday’s low of 108-21+ came close to support at 108-19 (20-day EMA) whilst channel resistance remains exposed with 109-06+ (channel top drawn from Feb 1 high) before other closely packed levels.

- Today’s NY Fed inflation expectations survey for April provides another look at surveyed expectations in what’s otherwise a thin docket ahead of PPI tomorrow and CPI on Wednesday.

- Data: NY Fed inflation expectations Apr (1100ET)

- Fedspeak: Mester & Jefferson on central bank communications (0900ET)

- Bill issuance: US Tsy $70B each 13W, 26W Bill auctions (1130ET)

STIR: Modest Paring Of Friday’s Lift For Fed Implied Rates

- Fed Funds implied rates have pared a small part of Friday’s increase on first spillover from Canadian jobs and then higher than expected U.Mich consumer inflation expectations.

- The rate path sits at a slightly higher level than shortly before Thursday's surprise push higher in initial jobless claims.

- Cumulative cuts from 5.33% effective: 2.5bp Jun, 7.5bp Jul, 20bp Sep, 29bp Nov and 43bp Dec.

- Today’s sole scheduled Fedspeak comes from Mester (’24 retiring next month) and VC Jefferson (voter) on central bank communications at 0900ET, with Jefferson providing prepared remarks.

- Jefferson said Apr 16 that he expects inflation to decline with rates held steady and will hold rates high for longer if inflation persists. The Fed’s job of restoring 2% inflation is not yet done and the labor market is to stay strong whilst it keeps rebalancing.

US TSY FUTURES: OI Data Points To Low Conviction Friday Session

The combination of Friday's weakness in Tsy futures and preliminary OI data points to a mix of net short setting (FV & WN) and long cover (TU, TY, UXY & US).

- There seemed to be a very modest bias towards net long cover in net curve OI DV01 equivalent terms, although the largest move in a single contract seemed to come via net short setting in FV futures.

- Still, the net OI swings were limited on the day, pointing to a low conviction session.

- The major input came from the downbeat UoM survey, which saw headline confidence readings fall and an uptick in inflation expectations, triggering further stagflation-related conversations.

- Note that an alteration in the survey collection method may have impacted the data.

- European holidays may have been a limiting factor for activity, with participants also looking ahead to this week's April CPI release.

- Net positioning remains short across the futures curve (albeit skewed by basis trade positions) as of the latest CFTC CoT report, which we covered in an earlier bullet.

| 10-May-24 | 09-May-24 | Daily OI Change | OI DV01 Equivalent Change ($) | |

| TU | 4,054,850 | 4,081,426 | -26,576 | -964,004 |

| FV | 6,155,441 | 6,125,560 | +29,881 | +1,222,969 |

| TY | 4,381,427 | 4,391,849 | -10,422 | -661,726 |

| UXY | 2,148,688 | 2,154,000 | -5,312 | -455,372 |

| US | 1,598,663 | 1,603,558 | -4,895 | -622,559 |

| WN | 1,642,730 | 1,637,993 | +4,737 | +927,351 |

| Total | -12,587 | -553,341 |

STIR: OI Points To Long Cover In SOFR Reds On Friday

The combination of Friday’s downtick in SOFR futures and OI data points to limited net pack positioning movement outside of the reds.

- Long cover seemed to dominate in all contracts in that pack.

- The major input came from the downbeat UoM survey, which saw headline confidence readings fall and an uptick in inflation expectations, triggering further stagflation-related conversations.

- FOMC-dated OIS pared pricing of ’24 cuts to ~40.5bp from ~44bp ahead of the release.

- Note that an alteration in the survey collection method may have impacted the data.

- European holidays may have been a limiting factor for activity, with participants also looking ahead to this week's April CPI release.

| 10-May-24 | 09-May-24 | Daily OI Change | Daily OI Change In Packs | ||

| SFIH4 | 249,375 | 250,796 | -1,421 | Whites | +2,307 |

| SFIM4 | 296,043 | 290,099 | +5,944 | Reds | -23,283 |

| SFIU4 | 239,803 | 240,392 | -589 | Greens | -315 |

| SFIZ4 | 297,651 | 299,278 | -1,627 | Blues | -253 |

| SFIH5 | 192,856 | 193,943 | -1,087 | ||

| SFIM5 | 183,655 | 188,764 | -5,109 | ||

| SFIU5 | 128,039 | 131,842 | -3,803 | ||

| SFIZ5 | 155,843 | 169,127 | -13,284 | ||

| SFIH6 | 104,688 | 102,761 | +1,927 | ||

| SFIM6 | 71,288 | 73,176 | -1,888 | ||

| SFIU6 | 55,647 | 55,984 | -337 | ||

| SFIZ6 | 62,259 | 62,276 | -17 | ||

| SFIH7 | 53,390 | 53,283 | +107 | ||

| SFIM7 | 42,354 | 40,915 | +1,439 | ||

| SFIU7 | 35,979 | 37,390 | -1,411 | ||

| SFIZ7 | 37,226 | 37,614 | -388 |

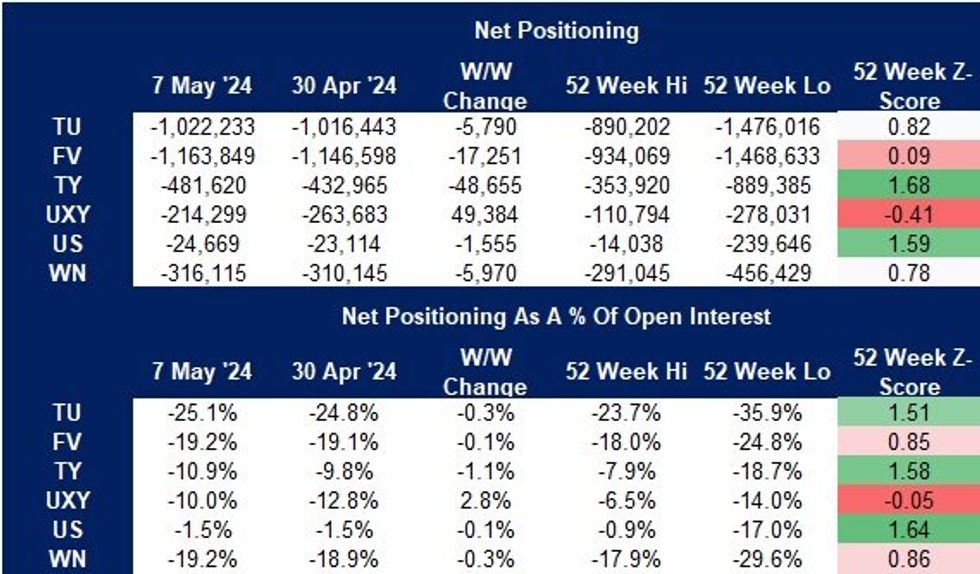

US TSY FUTURES: CFTC CoT Points To Hedge funds Driving Net Short Setting Across Much Of Curve

Friday’s CFTC CoT report pointed to non-commercial net short setting across most Tsy futures in the period up until 7 May.

- This was despite the softer-than-expected labor market report and generally softer-than-expected economic activity readings, as inflation components within the latest survey data continued to promote stagflation-related discussions, limiting receiver-side moves in FOMC-dated OIS.

- Only UXY futures saw their net short position trimmed, per the report.

- Closer inspection of the data reveals that hedge funds drove the deepening of the broader net short positioning, although they trimmed net shorts in both TU & UXY futures.

- Positioning remains net short across the curve (although some skew from basis trade positioning will be at play), with US futures the closest to net neutral positioning.

- All net shorts are comfortably off of the 52-week extremes, in both outright and net % of open interest terms.

Source: MNI - Market News/Bloomberg/CFTC

Source: MNI - Market News/Bloomberg/CFTC

GILTS: DMO likely to release quarterly consultation agenda today

- This afternoon will likely see the DMO release the agenda for next week’s quarterly consultation meetings to discuss issuance in FQ2 (the July to September period). We expect a release at 15:30BST.

- We will continue to see build up of the recently launched 3/5/7-year gilts, the new 10-year gilt that is due to be launched via syndication in June and the 30-year gilt that was tapped via syndication in June. In addition the 20/40-year gilts have yet to reach benchmark size.

- However, there is the possibility that we see a new 2035 linker issued or a new 15-year conventional gilt. The MNI Markets team currently pencil in a linker syndication in the W/C 8 July and a conventional long syndication in the W/C 2 September.

CFTC: AUD, NZD See Diverging Fortunes in CFTC Positioning

- Markets reversed a large part of the AUD net short by buying a net 19k contracts, putting the net position further off the 52w low to meet 31% of open interest. This tips the 52w Z-Score to 0.64 and potentially showing short-term momentum improvement since the nadir of mid-March.

- Conversely, the NZD position slipped, as markets sold a net of 2.6k contracts to deepen the net short. NZD shorts now account for a net 20% of open interest. The data, accurate as of the 7th May close, captured the poorer-than-expected Q1 labour market data, with employment change surprising lower (-0.2% vs. Exp. +0.3% Q/Q, unemployment rate at 4.3% vs. Exp. 4.2%).

- The JPY, GBP and EUR net positions gained, while CAD, CHF and MXN deteriorated. On a Z-score basis, CHF and EUR show the most negative readings, while MXN and now AUD are the most positive. Full update here:

FOREX: Placeholder Trade Ahead of US CPI Risks

- Early G10 trade this week has been largely a placeholder, with recent ranges being respected and price action lacking any meaningful conviction. The EUR is the firmest performing currency, helping EUR/GBP hold the recent bounce and keep prices anchored to the 200-dma of 0.8605.

- Pre-positioning and tactical trade is likely ahead of this Wednesday's CPI release, at which markets expect inflation to slow to 3.4% from 3.5%.

- EUR/CHF is trading on the front foot, helping the cross show above last week's highs and retrace the sell-off posted off 0.9837. Clearance here would open 0.9849 and levels last seen in May last year.

- Japanese intervention risks remain in the background, with the PM Kishida again commenting overnight that his staff watching FX moves "closely". USD/JPY is continuing to fade the late April intervention sell-off, with prices creeping to 155.96 early today. The pair has now printed higher lows for six consecutive sessions.

- The data and speaker schedule is typically light for a Monday, with no tier 1 releases on the docket. This leaves focus on Fed's Mester and Jefferson who appear at a Cleveland Fed event to discuss central bank communications strategy.

OPTIONS: Expiries for May13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0650(E2.5bln), $1.0750-55(E3.2bln), $1.0875-80(E893mln)

- GBP/USD: $1.2530(Gbp675mln), $1.2550-65(Gbp867mln)

- USD/JPY: Y155.00-15($2.4bln), Y157.45-50($1.4bln), Y157.65($901mln)

- USD/CNY: Cny7.3000($1.1bln)

EQUITIES: EuroStoxx Futures Top Bull Trigger

S&P E-Minis traded higher last week, extending the current bull cycle. Price has moved through resistance at the 20-day EMA - a bullish development. This highlights scope for a continuation higher that would expose the key resistance. Eurostoxx 50 futures build on the recent firm tone and the contract has traded higher to top the bull trigger. Recent gains have resulted in a breach of the 20-day EMA, resistance at 4990.00, as well as the bull trigger at 5079.00, Apr 2 high.

COMMODITIES: Bearish WTI Theme Remains Intact

A bearish theme in WTI futures remains intact and the contract traded to a fresh short-term cycle low last week. Gains off this mark are considered corrective for now. Price has recently breached the 50-day EMA, strengthening a short-term bearish theme that highlights potential for a deeper correction. Gold rallied well for two consecutive sessions as markets undergo a corrective bump higher. This breaks the consolidation phase and concludes the bearish short-term condition. The end of the corrective leg lower has unwound the overbought condition.

| Date | GMT/Local | Impact | Country | Event |

| 13/05/2024 | 1230/0830 | * | Building Permits | |

| 13/05/2024 | 1300/0900 | Cleveland Fed's Loretta Mester | ||

| 13/05/2024 | 1300/0900 | Fed Vice Chair Philip Jefferson | ||

| 13/05/2024 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 13/05/2024 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 14/05/2024 | 0600/0800 | *** | HICP (f) | |

| 14/05/2024 | 0600/0700 | *** | Labour Market Survey | |

| 14/05/2024 | 0700/0900 | *** | HICP (f) | |

| 14/05/2024 | 0700/0900 | ECB's De Guindos participates in ECOFIN meeting | ||

| 14/05/2024 | 0730/0830 | BOE's Pill Speech at Chartered Accountants Summit | ||

| 14/05/2024 | 0900/1100 | *** | ZEW Current Conditions Index | |

| 14/05/2024 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 14/05/2024 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 14/05/2024 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 14/05/2024 | 1230/0830 | *** | PPI | |

| 14/05/2024 | 1230/0830 | ** | Wholesale Trade | |

| 14/05/2024 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 14/05/2024 | 1310/0910 | Fed Governor Lisa Cook | ||

| 14/05/2024 | 1315/1515 | ECB's Schnabel speech at scientific conference | ||

| 14/05/2024 | 1400/1000 | Fed Chair Jerome Powell | ||

| 14/05/2024 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 14/05/2024 | 1530/1130 | * | US Treasury Auction Result for Cash Management Bill |