Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Modest risk-off as markets see little new in Biden stimulus plans

- Earnings take focus, with JPMorgan, Citigroup and Wells Fargo all due

- US retail sales, PPI and Michigan sentiment all due

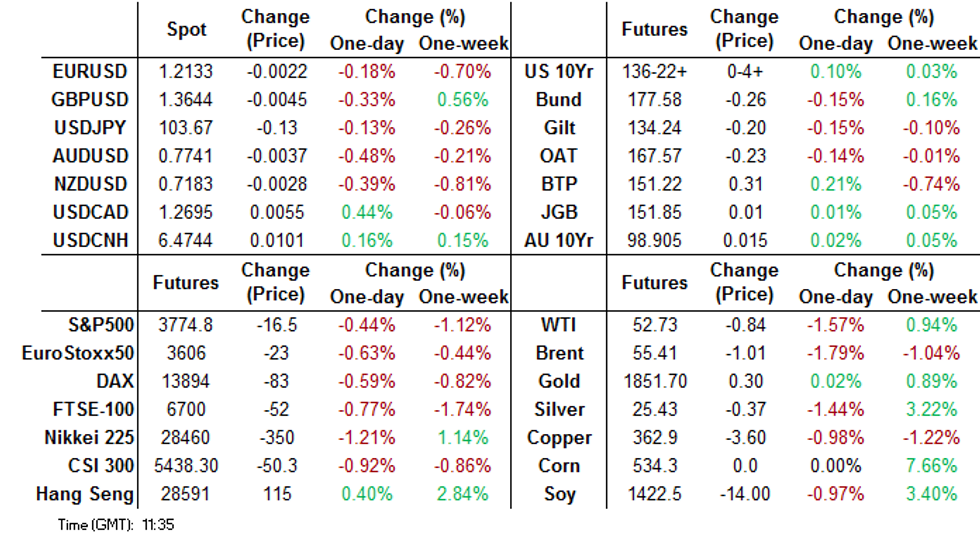

US TSYS SUMMARY: Shrugging Off Stimulus News, With Retail Sales/IP Data Eyed

A fairly underwhelming response to the Biden $1.9trn stimulus unveiling has seen Treasuries claw back late Thurs losses and equities on the back foot. Busy data slate ahead of the long weekend.

- Mar 10-Yr futures (TY) up 4.5/32 at 136-22.5 (L: 136-16.5 / H: 136-25.5), trading sideways after an initial jump in early Asia-Pac trade. All told, though, light volumes (~230k).

- The pre-Biden sell-off reversed overnight partly on the "sell the rumor, buy the fact" effect, but also on speculation of potential changes to/watering down of the proposal as it goes through Congress.

- Curve bull flattening; the 2-Yr yield is flat at 0.1391%, 5-Yr is down 1.4bps at 0.4694%, 10-Yr is down 2bps at 1.109%, and 30-Yr is down 2.1bps at 1.8514%.

- Dec retail sales highlights the data docket at 0830ET (same time sees Jan Empire Manufacturing and Dec PPI). At 0915ET we get the Dec industrial production release, with prelim UMich sentiment rounding off the calendar at 1000ET.

- Minn's Kashkari (1130ET) is the final scheduled Fed speaker before pre-FOMC blackout period.

- No supply. NY Fed buys ~$12.825B of 0-2.25Y Tsys.

- Reminder that Monday is a US market holiday (MLK Day).

EGB/GILT SUMMARY: Mixed Morning Amid Weaker Equities

Core European govies have traded mixed this morning alongside weaker trading in equities.

- The gilt curve has steepened on the back of the longer end selling off and the short-end firming. The 2s30s spread is 2bp wider on the day.

- Bunds have weakened with cash yields broadly 1-2bp higher.

- It is a similar story for OATs. Last yields: 2-year -0.6367%, 5-year -0.6509%, 10-year -0.3195%, 30-year 0.3851%.

- The BTP curve has bull steepened. Yields are 2-4bp lower with the short-end outperforming.

- SPGBs now trade close to unch on the day.

- Supply this morning came from the UK (Bills, GBP4.0bn).

- Data published today confirm that UK economic activity contracted in November with the monthly GDP for November coming in at -2.6% M/M vs -4.6% survey.

- There are signs that coronavirus infection rates are starting to stabilise in parts of England.

EUROPE OPTIONS SUMMARY

Eurozone:

DUG1 112.20/112.30/112.40 call fly sold at 5.5 in 1.1k

DUG1 112.30/112.40/112.50 call fly sold at 2.5 in 1.25k

DUH1 112.20/112.10 put spread bought for 1 in 2k

DUH1 112.20/112.30/112.40 call fly bought for 3.5 in 1.5k

UK:

LH1 100.00 call (v 99.995) sold at 2.5 in 6k

LZ1 99.875/100.00/100.125 call fly bought for 3.75 in 2.5k

0LH1 100.00/100.125 call spread sold at 2.25 in 16k

0LH1 100.00/100.125 1x2 call spread bought for 1.25 in 5.5k

0LH1 100.125/100.00/99.875 1x3x2 put fly (v 99.975), sold at 0.75 in 10.5k

0LJ1 100.00/100.125/100.25 call ladder bought for 2 in 3k

0LM1 100.00/99.875 1x2 put spread + 0LU1 99.875/99.75 1x2 put spread, strip bought for 3 in 8k

0LM1 100.00/99.75 put spread (v 99.955) bought for 9.25 in 10.5k

0LU1 99.875/99.75 1x2 put spread bought for 0.5 in 2k

FOREX: Markets Sluggish Post-Biden Stimulus Plan

Early trade in FX favouring USD, JPY and haven currencies more generally - growth proxies suffering a little, with CNH, AUD, CAD all hitting the day's lows just ahead of the NY crossover.

The outlining of Biden's plans for a $1.9trl stimulus package has raised concerns of swift, sharp opposition from Republican lawmakers over spending on Democratic priorities including aid to state and local governments. More details are expected at a joint session of Congress in February.

CAD, AUD and NZD are among the poorest performers early Friday as WTI and Brent roll off their respective cycle highs printed earlier n the week. Both benchmark oil contracts are off close to 1.5% apiece ahead of the final COMEX open of the week.

Earnings season gets underway in earnest Friday, with reports due from Wells Fargo, Citigroup and JPMorgan later today. US PPI and retail sales and industrial production for December also cross as well as the prelim Uni. of Michigan sentiment numbers.

FX OPTIONS: Expiries for Jan15 NY cut 1000ET (Source DTCC)

EUR/USD: $1.2000(E750mln), $1.2100(E777mln), $1.2135-50(E1.4bln), $1.2175-90(E1.1bln), $1.2195-1.2200(E670mln)

USD/JPY: Y101.00($610mln), Y103.00-10($694mln), Y103.50-60($1.2bln), Y104.00($1.0bln), Y104.80-00($1.5bln)

GBP/USD: $1.3400(Gbp677mln), $1.3585-1.3600(Gbp572mln), $1.3700(Gbp453mln)

EUR/GBP: Gbp0.8650(E1.5bln), Gbp0.8845-60(E2.7bln), Gbp0.8900(E750mln)

AUD/USD: $0.7695-00(A$705mln)

USD/MXN: Mxn19.50($1.2bln)

Tech Focus: Price Signal Summary - Attention Remains On The USDJPY Channel Top

- EURUSD bearish theme remains intact. Support levels to watch are:

- 1.2095, the 50-day EMA where a break would open 1.2059, Dec 9 low.

- USDJPY attention remains on key resistance at 104.23, the bear channel top drawn off the Mar 24 high. A break would highlight a stronger reversal. Monday's high of 104.40 is the bull trigger.

- Watch support though too at 103.53, Jan 13 low. A break would represent a bearish development.

- Sterling remains constructive and in Cable, scope is seen for a climb towards 1.3750, 0.764 projection of May 18 - Sep 1 rally from Sep 23 low

- EURGBP, this week cleared key support at 08933. The focus is on:

- 0.8867, Nov 23 low and a key support - tested this morning. A clear break would open 08800 and below.

- On the commodity front, Gold still appears vulnerable following recent weakness. Watch support at $1810.7 - 76.4% of the Nov 30 - Jan 6 rally. Oil contracts are off recent highs but remain bullish. Brent (H1) targets $58.59 - 76.4% of the Jan - Apr 2020 sell-off (cont). WTI (G1) focus is on $54.50 - high Feb 20, 2020 (cont).

- In the FI space:

- Bunds (H1) traded higher again yesterday and has breached all relevant near-term retracements. An extension higher would open the 178.37 high from Apr 4.

- Gilts (H1) resistance is seen at 134.64/69 20- and 50-day EMAs. A bearish outlook dominates while activity remains below these EMA levels.

EQUITIES: European Markets Soft Early Friday

Continental stock markets are softer Friday morning, with UK names underperforming (FTSE-100 lower by ~0.7%) while Italian stocks rebound and are one of the sole indices in the green so far.

A pullback in commodities this morning is leading the materials sector lower in the Stoxx 600, with real estate and industrials also weak. Healthcare and financials are sources of strength, with both sectors holding above water.

In the US, futures are off, with the e-mini S&P down around 10 points pre-open. Focus turns to looming earnings reports from Wells Fargo, Citigroup and JPMorgan later today.

COMMODITIES: Oil Opens Gap With Cycle Highs

Both WTI and Brent crude futures trade lower in early Friday trade, with losses of around 1.5% apiece. A stronger dollar is partially responsible, but a more general sense of risk-off and profit-taking is driving markets so far.

Given the pullback in equities this morning, gold is benefiting - spot gold remains pinched between the 200- and 50-dma directional parameters, today crossing at $1843.56 and $1863.61 respectively.

US data takes focus going forward, with retail sales, PPI and Uni. of Michigan numbers the highlights.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.