Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Europe sentiment mixed, France seen re-entering lockdown

- Month-end flow works against early USD strength

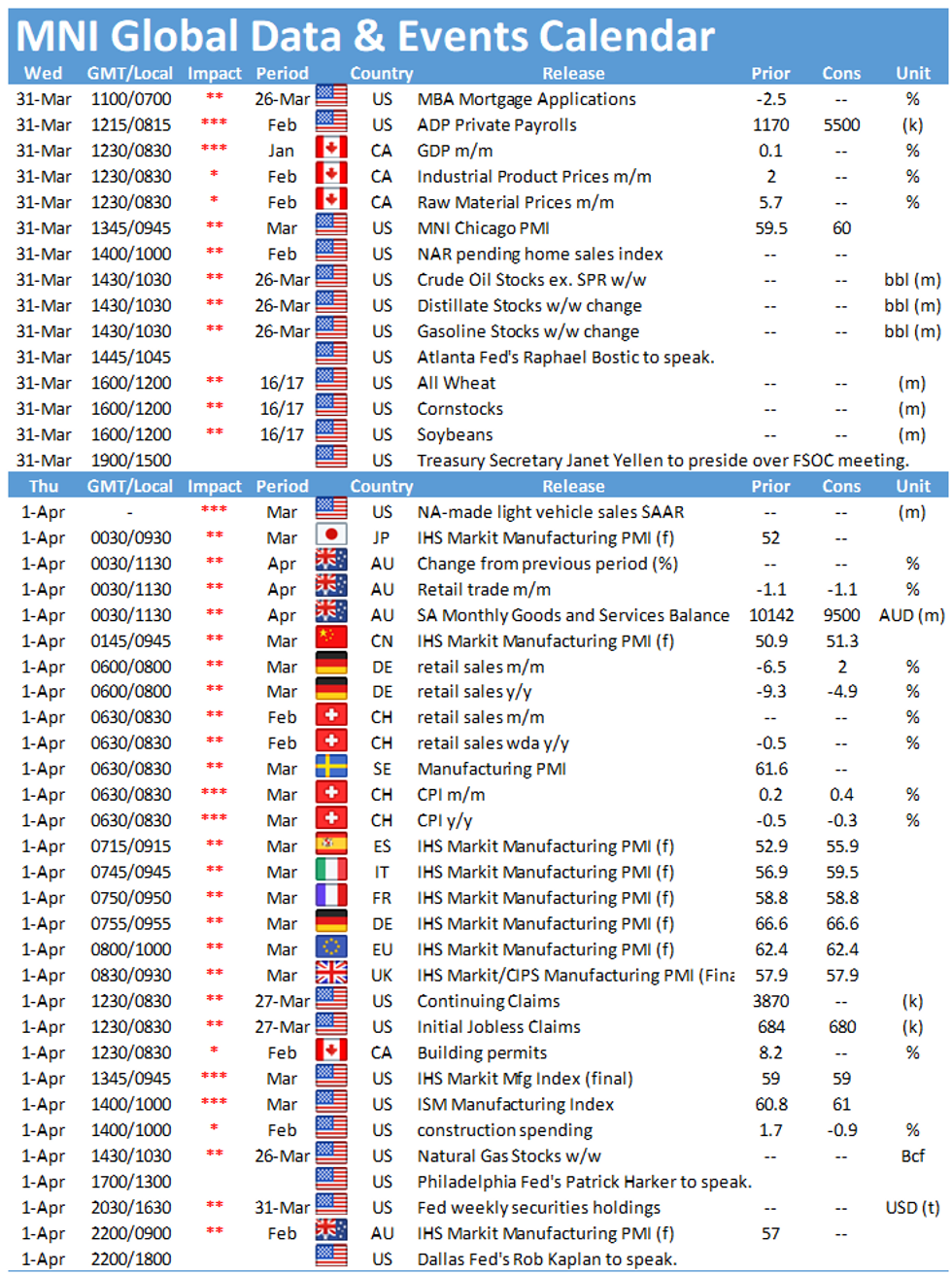

- Focus turns to Biden's stimulus plans, MNI Chicago PMI

US TSYS SUMMARY: Yields Firm Ahead Of ADP, MNI Chicago PMI, Biden Speech

Yields have firmed after Tuesday's late-session dip but remain well off the highs, ahead of data and quarter-end.

- Long-end takes a breather after Tuesday's rally: the 2-Yr yield is up 0.2bps at 0.1485%, 5-Yr is up 1.9bps at 0.9151%, 10-Yr is up 2.3bps at 1.7262%, and 30-Yr is up 2.1bps at 2.3892%.

- Jun 10-Yr futures (TY) down 1.5/32 at 131-04.5 (L: 131-01 / H: 131-09.5).

- Dollar and equities a little weaker.

- The highlight of the day is Pres Biden's speech at 1620ET laying out his "American Jobs Plan" - incorporating $2.25trn in spending on infrastructure and other measures, with accompanying tax hikes to fund it. But given that the plan has already been published, unlikely to be a market mover.

- In data, ADP private payrolls feature at 0815ET, with MNI Chicago PMI at 0945ET and pending home sales at 1000ET.

- Atlanta Fed's Bostic speaks at 1045ET, while Treas Sec Yellen presides over the FSOC meeting at 1500ET.

- In supply, $35B 119-day bill auction at 1130ET. NY Fed buys ~$1.75B of 20-30Y Tsys.

EGB/GILT SUMMARY: Mixed Trading

It has been a relatively mixed session so far with core European sovereign bond markets trading weaker, albeit with price action relatively contained, while periphery EGBs have firmed and alongside uneven trading in European equities.

- The gilt curve has flattened slightly on the back of softer trading at the short end and incremental gains the long end.

- Bunds now trade close to unch on the day with the curve flat. Last yields: 2-year -0.6961%, 5-year -0.6246%, 10-year -0.2863%, 30-year 0.2645%.

- It is a similar story OATs which trade in line with yesterday's close.

- BTPs have firmed slightly with yields up to 1bp lower on the day and the curve bull flattening.

- Data published this morning showed that the UK economy expanded faster than initially expected in the fourth quarter 1.3% vs an initial estimate of 1.0%). Elsewhere, French and Italian preliminary CPI data for March was a touch weaker than expected.

- After the German government announced on Tuesday that the AstraZeneca vaccine should only be used on people aged over 60, the UK government today reiterated its support for the Jab with Communities Secretary Robert Jenrick stating that the government is "100 percent" confident in the efficacy of the vaccine.

- Germany and France are reportedly in discussion with Russia bout the potential supply of the Sputnik Covid vaccine.

- Supply this morning came from Germany (Bund, EUR2.070bn allotted) and Greece (Bills, EUR812.5mn)

EUROPE ISSUANCE: German Auction

Germany allots E2.070bln 0% May-36 Bund, Avg yield 0.02% (Prev. -0.06%), Bid-to-cover 1.10x (Prev. 0.99x)

EUROPE OPTION FLOW SUMMARY

Eurozone:

DUK1 112.20c, bought for 1.25 in 5k

DUK1 112.10/112.20/112.30c fly, bought for 2 in 5k

UK:

0LU1 99.62/99.75/99.87c fly 1x3x2, bought for flat in 3.2k

3LM1 99.62/99.50/99.37p fly, sold at 1.25 in 3k

FOREX: Month-end Flow Reverses Stronger Start for USD

- EUR/USD hit new cycle lows of $1.1704 early Wednesday before price action reversed and USD weakness is seen across the G10 board. Month-end flows likely picking up, with continue to point toward general USD sales into the month-end fix against most others except for JPY. The JPY selling signal is playing out this morning, with USD/JPY touching new 2021 highs and narrowing the gap with Y111.00.

- NOK and GBP are moderately stronger so far. The price action has helped press EUR/NOK to the lowest levels of the year, touching 10.0030. A break below the 10.00 handle would be the first since early last year.

- Focus turns to US ADP Employment Change numbers, the MNI Chicago Business Barometer, pending home sales numbers and Canadian GDP for January. US President Biden also speaks on his economic plans for the US. Reports this morning see Biden announcing plans for a $2.25 trillion economic plan, with the spending offset by a hike in the corporate tax rate to 28%.

Expiries for Mar31 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1650(E714mln), $1.1725-30(E648mln-EUR puts), $1.1750(E1.2bln), $1.1770-75(E1.2bln), $1.1785-90(E818mln), $1.1800(E1.2bln), $1.1850(E1.36bln-EUR puts), $1.1880(E606mln), $1.1900(E1.8bln), $1.1920-25(E1.7bln), $1.1945-56(E1.3bln), $1.2000(E1.0bln)

- USD/JPY: Y108.50($725mln), Y109.50($630mln), Y110.00($2.6bln-$2.48bln of USD puts), Y110.15-20($1.25mln-USD puts), Y110.50($685mln-USD puts), Y110.80($475mln-USD puts)

- GBP/USD: $1.3650-70(Gbp686mln), $1.3800(Gbp921mln-GBP puts), $1.3825(Gbp432mln-GBP puts), $1.3945-50(Gbp537mln), $1.3960-75(Gbp720mln), $1.4000(Gbp751mln)

- EUR/GBP: Gbp0.8515-25(E1.2bln-EUR puts), Gbp0.8540-50(E1.3bln-EUR puts), Gbp0.8600(E1.3bln-E1.2bln of EUR puts), Gbp0.8645-50(E664mln)

- USD/CHF: Chf0.9250($660mln)

- AUD/USD: $0.7450(A$864mln), $0.7500(A$1.3bln), $0.7600-05(A$732mln), $0.7650(A$774mln), $0.7675-90(A$917mln), $0.7700(A$1.0bln), $0.7750-60(A$1.8bln), $0.7770-80(A$1.3bln), $0.7790-0.7800(A$1.1bln), $0.7825-30(A$615mln)

- AUD/JPY: Y84.45(A$782mln)

- EUR/AUD: A$1.5450-60(E696mln-EUR puts)

- USD/CAD: C$1.2500($837mln), C$1.2600-05($690mln), C$1.2645-50($1.1bln-USD puts)

EQUITIES: Mixed Start To Last Day Of Quarter

- Asian stocks closed lower, with Japan's NIKKEI down 253.9 pts or -0.86% at 29178.8 and the TOPIX down 23.86 pts or -1.21% at 1954. China's SHANGHAI closed down 14.765 pts or -0.43% at 3441.912 and the HANG SENG ended 199.15 pts lower or -0.7% at 28378.35.

- European equities are flat/lower, with the German Dax up 0.8 pts or +0.01% at 15000.32, FTSE 100 down 17.85 pts or -0.26% at 6769.89, CAC 40 down 6.51 pts or -0.11% at 6091.2 and Euro Stoxx 50 down 3.9 pts or -0.1% at 3918.49.

- U.S. futures are mixed, with the Dow Jones mini down 14 pts or -0.04% at 32911, S&P 500 mini down 0.25 pts or -0.01% at 3947.5, NASDAQ mini up 23.75 pts or +0.18% at 12902.

COMMODITIES: Metals Gain As Dollar Softens Slightly

- WTI Crude down $0.02 or -0.03% at $60.91

- Natural Gas up $0.01 or +0.19% at $2.627

- Gold spot up $0.8 or +0.05% at $1685.85

- Copper up $2.7 or +0.68% at $399.9

- Silver up $0.1 or +0.42% at $24.1318

- Platinum up $19.5 or +1.68% at $1176.6

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok